|

市場調査レポート

商品コード

1683917

英国の家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)United Kingdom Poultry Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 208 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

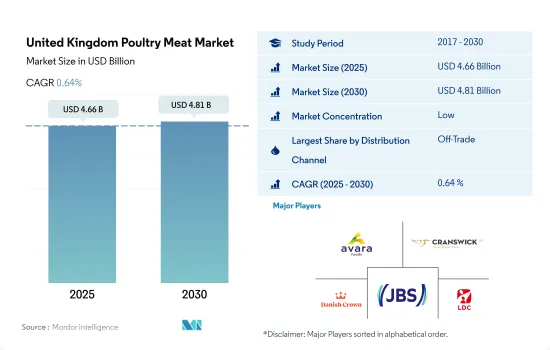

英国の家禽肉市場規模は2025年に46億6,000万米ドルと推定・予測され、2030年には48億1,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは0.64%で成長すると予測されます。

大手小売チェーンの拡大が市場を牽引

- 英国では、家禽肉製品が最も消費される主なチャネルは非商業流通チャネルです。商業外流通チャネルのサブタイプの中では、スーパーマーケットとハイパーマーケットが主要チャネルです。スーパーマーケットは、2022年には金額ベースで64.2%の最大市場シェアを占めました。こうした小売業態の成長は、事業拡大やスーパーマーケットやハイパーマーケットの増加といった要因とともに、英国の家禽製品市場にプラスの影響を与えました。ディスカウント店の人気に伴い、食料品小売市場はテスコ、セインズベリー、アスダ、モリソンズの各スーパーマーケットによって支配されていました。2022年の市場シェアは、テスコが27.5%、セインズベリーが15.2%で、英国最大の小売業者でした。

- 英国のレストランでは、チキンウィング、チキンナゲット、チキンロリポップなどの家禽肉料理が人気です。同国では肉の消費量が多いため、2018年から2022年にかけて、オン・トレード・チャネルを通じて家禽肉消費は金額ベースで16.85%の売上成長を記録しました。マクドナルド、KFC、サブウェイなどの人気ファーストフードチェーンの特別なレシピと味が消費者に好まれ、売上にプラスの影響を与えています。2022年現在、英国のサブウェイ店舗数は2,209で、欧州で最も多いです。

- オフ・トレード・チャネルでは、オンライン・チャネルが市場で最も急成長しているセグメントです。予測期間中のCAGRは金額ベースで6.39%と予測されています。このように、インターネットユーザーの増加に対応してオンライン食料品店の数が増加しており、予測期間中に乳製品のオンライン販売を促進すると予想されます。2022年現在、英国では食料品のオンラインショッピングは13%に過ぎないです。

英国の家禽肉市場動向

労働力不足が業界に大きな影響

- 英国の家禽生産量は2022年には2021年から1.88%減少。英国の国内家禽は様々な種で構成されており、主に家禽とターキーだが、アヒルやガチョウもいます。ホロホロチョウやウズラはあまり使われていません。しかし、2022年の英国の家禽個体数は1.0%減少し、1億8,800万羽に達しました。繁殖家禽と産卵家禽は2021年に比べ0.5%減少し、5,300万羽に達しました。同様に、ブロイラー(食卓用鶏)も2022年には2021年比で0.5%減少し、1億2,600万羽に達し、家禽総数の3分の2強を占める。

- 現在、世界で認められている家禽品種は1,132種で、その58%が欧州にあります。欧州では、204の家禽品種がすでに危機的状況にあり、34の家禽品種が絶滅しています。英国では、280種以上の家禽(アヒル33種、ガチョウ23種、鶏124種、ミニチュア63種、バンタム20種、ターキー18種)が存在し、最近輸入された外来種を除けば、そのすべてが英国家禽クラブによって正式に品種として認定され、標準化されています。英国の家禽肉業界は、農業部門と加工部門の労働力不足に悩まされています。

- 生産者はBrexitが主食用製品に与える影響を懸念しています。人手不足の結果、英国の生産者は英国の顧客向けに限られた種類の製品を生産しています。2021年の平均欠員率は全労働力の16%を超えており、欠員数は増加傾向にあります。ブレグジットは業界に打撃を与え、多くの生産者は週当たりの鶏肉生産量を5~10%削減せざるを得なくなりました。通年のターキー生産量は、2020年と比較して2021年には10%減少しました。クリスマス用ターキーの生産量は2021年に20%減少したと推定されます。

ブレグジットとロシア・ウクライナ紛争が英国の価格を高騰させた

- 英国における家禽の価格は2017年から2022年にかけて10.18%上昇しました。鶏肉は英国で最も広く消費されている肉であり、牛肉、羊肉、豚肉よりも多く食べられています。鶏肉は安価であるため、国中で選ばれる肉となっています。しかし、2022年5月の鶏肉の平均小売価格は31p/kg上昇し、1年前より12%近く高くなり、3.2米ドル/kgに達しました。ウクライナ戦争、エネルギー価格の上昇、ブレグジットは、英国で鶏肉価格が上昇した理由の一部です。

- 2022年のファームゲート価格は前年比で50%近く上昇しました。電力、燃料、ワクチン、パッケージング、その他のコストの上昇により、同国の生産コストはますます高くなっています。2022年、小規模施設の場合、電気代は月200米ドルから600米ドル以上に、鶏を保管するための段ボール箱は1,000羽あたり800米ドルから1,000羽あたり1,000米ドル以上に増加しました。鶏に必要なワクチンも同年に8%増加しました。さらに、前年は飼料代も上昇しました。これは、不作とロシア・ウクライナ戦争により、飼料によく使われる小麦と大豆の価格が高騰したためです。

- ここ数ヶ月、Nando'sやKFCといったファーストフード店の価格が上昇しています。冷蔵オーブン用鶏肉の平均小売価格は、過去2年間で最低の2.69米ドル/kgから4.2米ドル/kgに上昇しました。例えば、2021年12月の手羽先1箱の価格は22米ドルだったが、2022年5月には27~28米ドルに上昇しました。

英国の家禽肉産業の概要

英国の家禽肉市場は断片化されており、上位5社で18.65%を占めています。この市場の主要企業は以下の通り。 Avara Foods Ltd, Cranswick plc, Danish Crown AmbA, JBS SA and Lambert Dodard Chancereul(LDC)Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 鶏肉

- 生産動向

- 家禽

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮/冷蔵

- 冷凍

- 加工品

- 加工タイプ別

- デリミート

- マリネ/テンダー

- ミートボール

- ナゲット

- ソーセージ

- その他加工家禽

- 流通チャネル

- 非売品

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- 非売品

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向の分析を含む)

- 2 Sisters Food Group

- Avara Foods Ltd

- Blackwells Farm

- Copas Traditional Turkeys

- Cranswick plc

- Danish Crown AmbA

- Donald Russell Ltd

- Gressingham Foods

- JBS SA

- Lambert Dodard Chancereul(LDC)Group

- Salisbury Poultry(Midlands)Ltd.

- Wild Meat Company

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001607

The United Kingdom Poultry Meat Market size is estimated at 4.66 billion USD in 2025, and is expected to reach 4.81 billion USD by 2030, growing at a CAGR of 0.64% during the forecast period (2025-2030).

Expansion of leading retail chains is driving the market

- In the United Kingdom, the off-trade distribution channel is the primary channel through which poultry meat products are consumed most in the country. Of all the sub-types of the off-trade channel, supermarkets and hypermarkets are the major channels. Supermarkets held the largest market share of 64.2% by value in 2022. The growth of these retail formats, along with factors like business expansion and the increase in supermarkets and hypermarkets, positively impacted the poultry products market in the United Kingdom. With the popularity of the discounters, the grocery retail market was dominated by Tesco, Sainsbury's, Asda, and Morrisons supermarkets. Tesco was the largest retailer in Great Britain, with a market share of 27.5%, and Sainsbury's with 15.2% in 2022.

- Poultry meat dishes in restaurants in the UK, including chicken wings, chicken nuggets, and chicken lollipops, are popular in the country. Poultry meat consumption registered a sales growth of 16.85% by value from 2018 to 2022 through the on-trade channel, owing to the high meat consumption in the country. The special recipes and tastes of popular fast-food chains like McDonald's, KFC, and Subway are preferred by consumers, affecting sales positively. As of 2022, the United Kingdom had the highest number of Subway restaurants in Europe, at 2,209 locations.

- In the off-trade channel, online channels comprise the fastest-growing segment in the market. It is projected to register a CAGR of 6.39% by value during the forecast period. Thus, there has been an increase in the number of online grocery shops in response to the rising number of internet users, which is anticipated to drive online sales of dairy products during the forecast period. As of 2022, only 13% of grocery shopping was conducted online in the UK.

United Kingdom Poultry Meat Market Trends

Labor shortage is highly affecting the industry

- The UK poultry production decreased by 1.88% in 2022 from 2021. The UK's domestic poultry population is made up of a variety of species, predominantly fowls and turkeys, but also ducks and geese. Guinea fowls and quail are used less often. However, in 2022, the poultry population in the United Kingdom declined by 1.0%, reaching 188 million birds; breeding and laying fowl declined by 0.5%, reaching 53 million birds compared to 2021. Similarly, broilers (table chickens) experienced a 0.5% decrease in 2022 compared to 2021, reaching 126 million birds, representing just over two-thirds of the total poultry population.

- Currently, there are 1,132 poultry breeds recognized around the world, 58% of which are in Europe. In Europe, 204 poultry breeds are already critical, and 34 are extinct. In the UK, there are over 280 poultry breeds (33 ducks, 23 geese, 124 fowls, 63 miniatures, 20 bantams, and 18 turkeys), all of which, apart from a few recent imported exotics, are officially recognized as a breed and standardized by the Poultry Club of Great Britain. The UK poultry meat industry is struggling with labor shortages across the farming and processing sectors.

- The producers are concerned about the impact of Brexit on staple products. As a result of labor shortages, UK producers are producing a limited range of products for UK customers. The average vacancy rate was over 16% of the total workforce in 2021, and the number of gaps is on the rise. Brexit has had a knock-on effect on the industry, with many producers having to reduce weekly chicken output by 5-10%; all-year-round turkey output dropped by 10% in 2021 compared to 2020. Christmas turkey production was estimated to have dropped by 20% in 2021.

Brexit and the Russia-Ukraine conflict inflated the prices in the United Kingdom

- The prices of poultry in the UK rose by 10.18% from 2017 to 2022. Chicken is the most widely consumed meat in the UK, with people eating it more than beef, lamb, or pork. Chicken's low cost has made it the meat of choice across the country. However, the average retail cost of chicken rose by 31 p/kg in May 2022, nearly 12% more expensive than it was a year ago, reaching USD 3.2/kg. War in Ukraine, increased energy prices, and Brexit are a few of the reasons why poultry prices increased in the UK.

- The farm gate prices increased by nearly 50% in 2022 compared to the previous year. The cost of production in the country has become increasingly expensive due to rising electricity, fuel, vaccines, packaging, and other costs. In 2022, for a small facility, the electricity bill increased from USD 200 per month to more than USD 600 per month, and the cardboard boxes used to store chickens increased from USD 800 per 1,000 to more than USD 1,000 per 1,000. The vaccines needed for the chickens also increased by 8% in the same year. Furthermore, the cost of feed increased in the previous year. This was due to a surge in the prices of wheat and soy, which are often used in the feed production process, due to the unsuccessful harvests and the Russia-Ukraine War; the countries together account for approximately 30% of the world's wheat supply.

- In recent months, fast food outlets such as Nando's and KFC have seen their prices rise. The average retail price of refrigerated oven-ready chicken increased from a low of USD 2.69/kg to USD 4.2/kg in the past two years. For example, in December 2021, a box of chicken wings was priced at USD 22, which increased to USD 27 to 28 per box in May 2022.

United Kingdom Poultry Meat Industry Overview

The United Kingdom Poultry Meat Market is fragmented, with the top five companies occupying 18.65%. The major players in this market are Avara Foods Ltd, Cranswick plc, Danish Crown AmbA, JBS SA and Lambert Dodard Chancereul (LDC) Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Poultry

- 3.2 Production Trends

- 3.2.1 Poultry

- 3.3 Regulatory Framework

- 3.3.1 United Kingdom

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.1.4.1 By Processed Types

- 4.1.4.1.1 Deli Meats

- 4.1.4.1.2 Marinated/ Tenders

- 4.1.4.1.3 Meatballs

- 4.1.4.1.4 Nuggets

- 4.1.4.1.5 Sausages

- 4.1.4.1.6 Other Processed Poultry

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 2 Sisters Food Group

- 5.4.2 Avara Foods Ltd

- 5.4.3 Blackwells Farm

- 5.4.4 Copas Traditional Turkeys

- 5.4.5 Cranswick plc

- 5.4.6 Danish Crown AmbA

- 5.4.7 Donald Russell Ltd

- 5.4.8 Gressingham Foods

- 5.4.9 JBS SA

- 5.4.10 Lambert Dodard Chancereul (LDC) Group

- 5.4.11 Salisbury Poultry (Midlands) Ltd.

- 5.4.12 Wild Meat Company

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms