|

市場調査レポート

商品コード

1692026

アフリカの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Africa Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 217 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

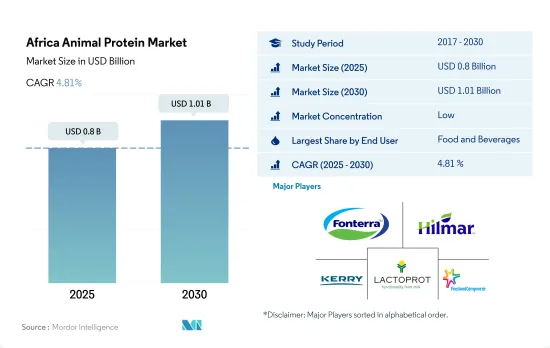

アフリカの動物性たんぱく質市場規模は2025年に8億米ドルと推定・予測され、2030年には10億1,000万米ドルに達し、予測期間(2025-2030年)のCAGRは4.81%で成長すると予測されます。

手頃な価格で高品質な製品の流入が、飲食品とパーソナルケア・化粧品市場を牽引します。

- 用途別では、飲食品部門が2022年の動物性たんぱく質のエンドユーザー部門としてこの地域をリードしています。2022年の飲食品セグメントでは、ベーカリーおよびスナックのサブセグメントがそれぞれ27.14%および23.58%と、主要な数量シェアを占めています。健康的な間食、冷凍スナック需要の増加、手頃な価格で高品質なプライベートブランド製品の流入増加がスナックサブセグメントの成長に寄与しています。南アフリカでは、ゼラチンや乳清たんぱく質は栄養価が高く消化器系の健康増進に役立つと考えられているため、健康志向がヨーグルトやその他の冷凍スナック製品の成長を支え続けています。このため、スナックのサブセグメントは予測期間中に金額ベースで3.55%のCAGRで推移すると予測されます。

- しかし、パーソナルケア分野は予測期間中、金額ベースで最も速いCAGR 5.95%を記録すると見られています。美容クリニックの増加、身だしなみに対する一人当たり支出の増加、強固な規制枠組み、美容・化粧品市場の拡大が、この地域のコラーゲン原料需要を促進しています。

- サプリメントは同市場の第2位を占めています。最も急速に成長しているスポーツ・パフォーマンス栄養サブセグメントは、サプリメントの成長を支援しています。予測期間中のCAGRは金額ベースで4.05%を記録すると予測されています。アフリカの消費者は、その他の活動の中でもランニングやサッカーなどのスポーツに積極的です。同地域では、スポーツジムの会員になっている消費者がかなりの割合を占めています。例えば、2020年には南アフリカには約2,450のヘルスクラブがありました。ヘルスセンターやフィットネスセンターの増加は、このサブセグメントの成長にプラスの影響を与えています。

ナイジェリアやその他のアフリカ諸国のような国々におけるたんぱく質強化食品に対する需要の高まりが、このセグメントの需要を引き寄せています。

- その他のアフリカ(エチオピア、ケニア、ガーナ、ギニア、コートジボワールを含む)は2022年の動物性たんぱく質市場をリードしました。たんぱく質の種類別では、乳清たんぱく質が2022年の数量シェア32.30%で市場を独占しました。市場の需要が最も高かったのは、乳清たんぱく質をベースにした機能性スナックでした。これらの国の消費者は健康的な食事への関心が高まっており、ホエイたんぱく質ベースの食事を好むようになっています。消費者は栄養要求を満たすために、スナックバー、たんぱく質強化クッキーなどの製品を選び、サブセグメントの成長を後押ししています。

- しかし、ナイジェリアは動物性たんぱく質で最も急成長している国であり、予測期間中のCAGRは6.94%を記録すると予測されています。同国で2022年に最も消費されたたんぱく質はゼラチンで、金額シェアは27%でした。ゼラチンは消化しやすいたんぱく質で、体重管理に対応し、健康な免疫システムを維持します。こうした利点がナイジェリアの動物性たんぱく質市場での需要を促進しています。動物性ゼラチン、特に牧草飼育牛のゼラチンは、遺伝子組み換え作物、農薬、ホルモン、抗生物質、化学添加物などの危険な汚染物質を含まないため、市場を独占しています。

- 南アフリカは、アフリカの動物性たんぱく質市場においてわずかなシェアを占めています。予測期間中のCAGRは3.20%と予測されています。ホエイ蛋白質は、他の動物性蛋白質の中で同国の主要な蛋白質のひとつに浮上しました。ホエイたんぱく質は、筋肉のリハビリテーションや運動前のエクササイズに理想的であるため、サプリメント分野、特にスポーツ栄養サブセグメントにおいて主要な用途があります。

アフリカの動物性たんぱく質市場動向

消費者の健康意識の高まりと健康的な食習慣により、動物性たんぱく質の一人当たり消費量は大幅な伸びを示します。

- グラフはアフリカの一人当たり動物性たんぱく質消費量を示しています。この消費は、消費者の健康意識の高まりと栄養価の高い食事への最近のシフトによって推進されています。乳児用調製粉乳、特に乳たんぱく質に由来する調製粉乳の栄養的利点に関する両親の意識が、消費に拍車をかけています。しかし、市場は菜食主義者の増加や乳糖不耐症の顕著な蔓延といった課題に直面しています。2017年以降、市場の成長は鈍化しているが、その一因は南アフリカの法律、特に栄養補助食品をめぐる法律が変化し、メーカーにとって追加の認証コストが発生するようになったことです。

- サハラ以南のアフリカでは、過去20年間で1人当たりの牛乳消費量が減少しているが、動物性たんぱく質の消費量は2017年の88gから2022年には105.7gに増加しています。2050年までにアフリカの人口が13億人から25億人に増加すると予測されていることから、動物性たんぱく質の需要は増加すると考えられます。

- 南アフリカのメーカーは、革新的な生産技術を導入し、市場のコスト・リーダーシップを獲得しています。高品質たんぱく質の乳児用調製粉乳に対する働く女性の需要の増加や、スポーツ選手の栄養ニーズが成長率を押し上げています。成熟し組織化された小売セクターにより、たんぱく質製品の棚スペースは増加し、アフリカ地域で大きなシェアを維持すると予想されます。その結果、消費者は栄養ニーズを満たし健康を維持するためにたんぱく質バーやサプリメントを購入するようになっています。消費者のライフスタイルの変化とヘルスケア支出の増加も、アフリカの植物性たんぱく質市場の成長に重要な役割を果たしています。

食肉と牛乳の生産は、動物性たんぱく質原料メーカーの一次原料情報です。

- 牛乳は、乳たんぱく質、乳清たんぱく質、カゼイン、カゼイネートなどの動物性たんぱく質を生産するための主原料となります。スーダン、エジプト、ケニア、南アフリカ、アルジェリアがアフリカの牛乳生産国トップ5です。西アフリカでは、2000年から2016年にかけて地元の牛乳生産量が50%急増し、2019年には約40億リットルに達します。南アフリカの2019年のヘルスクラブ会員数226万人に代表されるように、この地域のフィットネス文化の高まりが乳清たんぱく質の生産を押し上げました。

- 地元で生産された牛乳が消費の65~70%を占め、輸入粉乳がそのギャップを埋めています。2018年、EUは9万2,620トンの粉ミルクと27万6,982トンの脂肪入り粉ミルクを西アフリカに輸出しました。ケニアは東アフリカの主要な生乳生産国として際立っており、酪農産業はこの国の農業情勢をリードし、GDPに4%寄与し、所得創出と雇用において極めて重要な役割を果たしています。

- 一人当たりの畜産物消費量の記録に基づくと、南アフリカに必要な飼料は2021年に1,330万トンとなり、同地域における飼料用昆虫たんぱく質の需要増加により、予測期間中にさらに増加すると予測されます。アフリカでは、コラーゲンやゼラチンのような動物性たんぱく質は通常、動物や海洋廃棄物から調達されます。興味深いことに、豚は飼料をあまり必要としない点で際立っています。これは、消化と代謝の際に発生する余分な熱の管理に役立つだけでなく、たんぱく質含有量にも影響します。

アフリカの動物性たんぱく質産業の概要

アフリカの動物性たんぱく質市場は断片化されており、上位5社で11.63%を占めています。この市場の主要企業は以下の通りです。 Fonterra Co-operative Group Limited, Hilmar Cheese Company Inc., Kerry Group plc, Lactoprot Deutschland GmbH and Royal FrieslandCampina N.V(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- 南アフリカ

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- たんぱく質タイプ

- カゼインとカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他動物性たんぱく質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Amesi Group

- Fonterra Co-operative Group Limited

- Hilmar Cheese Company Inc.

- Kerry Group plc

- Lactoprot Deutschland GmbH

- Prolactal

- Royal FrieslandCampina N.V

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Animal Protein Market size is estimated at 0.8 billion USD in 2025, and is expected to reach 1.01 billion USD by 2030, growing at a CAGR of 4.81% during the forecast period (2025-2030).

Rising influx of affordable and high-quality products drive the food and beverages and personal care and cosmetics segment in the market

- By application, the food and beverages segment was the region's leading end-user segment for animal protein in 2022. The bakery and snacks sub-segment accounted for the major volume shares in the food and beverage segment, i.e., 27.14% and 23.58%, respectively, in 2022. Healthy snacking, rising demand for frozen snacks, and increased influx of affordable and high-quality private label products contribute to the growth of the snacks sub-segment. The health and wellness trend continued to support the growth of yogurt and other frozen snack products in South Africa since gelatin and whey protein is supposed to be highly nutritious and good at improving digestive health. Thus, the snacks sub-segment is projected to record a CAGR of 3.55% by value during the forecast period.

- However, the personal care segment is set to register the fastest CAGR of 5.95% by value during the forecast period. The increasing number of beauty clinics, rising per capita expenditure on personal appearance, robust regulatory framework, and the growing beauty and cosmetics market propel the region's demand for collagen ingredients.

- Supplements held the second position in the market. The sports and performance nutrition sub-segment, the fastest-growing sub-segment, aids the growth of supplements. It is projected to record a CAGR of 4.05%, by value, during the forecast period. African consumers are actively into sports, such as running and football, among other activities. There is a considerable portion of consumers in the region with gym memberships. For instance, in 2020, there were around 2,450 health clubs in South Africa. The increasing number of health and fitness centers has been positively influencing the growth of the sub-segment.

Rising demand for protein-enriched foods in countries like Nigeria and Rest of Africa segment draw the segmental demand

- The Rest of Africa (including Ethiopia, Kenya, Ghana, Guinea, and Ivory Coast) led the animal protein market in 2022. By protein type, whey protein dominated the market with a 32.30% volume share in 2022. The highest market demand was for whey protein-based functional snacks. Consumers in these countries are becoming increasingly concerned about healthy eating and prefer whey protein-based diets. They are opting for products like snack bars, protein-enriched cookies, and others to fulfill their nutritional requirements, thereby boosting the sub-segment's growth.

- However, Nigeria is projected to be the fastest-growing country for animal proteins, recording a CAGR of 6.94% during the forecast period. Gelatin was the most consumed protein in the country in 2022, with a value share of 27%. Gelatin is an easily digestible protein that caters to weight management and maintains a healthy immune system. These benefits have promoted its demand in the Nigerian animal protein market. Animal-based gelatin, particularly grass-fed beef gelatin, dominates the market as it contains no dangerous contaminants such as GMOs, pesticides, hormones, antibiotics, or chemical additives.

- South Africa held a minor share in the African animal protein market. It is projected to record a CAGR of 3.20% during the forecast period. Whey protein emerged as one of the country's major protein types among other animal proteins. It has major applications in the supplements segment, especially in the sports nutrition sub-segment, as it is ideal for muscle rehabilitation and pre-workout exercises.

Africa Animal Protein Market Trends

Per capita consumption of animal protein to witness significant growth due to growing health awareness and healthy eating habits of consumers

- This consumption is propelled by a rising health consciousness and a recent shift toward nutritious eating among consumers. The awareness among parents regarding the nutritional benefits of infant formulas, especially those derived from milk protein, is fueling their consumption. However, the market faces challenges from the increasing adoption of veganism and a notable prevalence of lactose intolerance. Since 2017, the market's growth has been sluggish, attributed in part to shifts in South African legislation, particularly around dietary supplements, which have led to additional certification costs for manufacturers.

- While Sub-Saharan Africa has seen a decline in per capita milk consumption over the past two decades, the consumption of animal protein rose from 88 g in 2017 to 105.7 g in 2022. Given Africa's projected population growth from 1.3 billion to 2.5 billion by 2050, the demand for animal protein is set to rise.

- South African manufacturers have embraced innovative production techniques to gain market cost leadership. Increasing demand from working women for high-quality protein infant formulas and the nutritional needs of athletes are driving growth rates. With a mature and organized retail sector, shelf space for protein products is expected to increase, maintaining a large share in the African region. As a result, consumers are increasingly buying protein bars and supplements to meet their nutritional needs and maintain their health. Changing consumer lifestyles and rising healthcare expenditures also play a vital role in the growth of the plant protein market in Africa.

Meat and milk production are primary sources of raw materials for manufacturers of animal protein ingredients

- Milk serves as the primary raw material for producing animal proteins like milk proteins, whey proteins, casein, and caseinates. Sudan, Egypt, Kenya, South Africa, and Algeria emerge as the top five milk-producing nations in Africa. West Africa saw a 50% surge in local milk production from 2000 to 2016, reaching approximately 4 billion liters by 2019. The region's growing fitness culture, exemplified by South Africa's 2019 figure of 2.26 million health club members, boosted whey protein production.

- Locally produced milk accounts for 65-70% of consumption, with imported milk powder filling the gap. In 2018, the European Union exported 92,620 tons of milk powder and 276,982 tons of fat-filled milk powder to West Africa. Kenya stands out as East Africa's primary milk producer, with the dairy industry leading the country's agricultural landscape, contributing 4% to its GDP and playing a pivotal role in income generation and employment.

- Based on the records of per capita animal product consumption, the feed required for South Africa was 13.3 million tons in 2021, which is projected to increase further during the forecast period due to the rising demand for insect proteins for animal feed in the region. In Africa, animal proteins like collagen and gelatin are typically sourced from animal and marine waste. Interestingly, pigs stand out by requiring less feed. This not only helps in managing the excess heat generated during digestion and metabolism but also influences their protein content.

Africa Animal Protein Industry Overview

The Africa Animal Protein Market is fragmented, with the top five companies occupying 11.63%. The major players in this market are Fonterra Co-operative Group Limited, Hilmar Cheese Company Inc., Kerry Group plc, Lactoprot Deutschland GmbH and Royal FrieslandCampina N.V (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 South Africa

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Nigeria

- 4.3.2 South Africa

- 4.3.3 Rest of Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Amesi Group

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Hilmar Cheese Company Inc.

- 5.4.4 Kerry Group plc

- 5.4.5 Lactoprot Deutschland GmbH

- 5.4.6 Prolactal

- 5.4.7 Royal FrieslandCampina N.V

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms