|

市場調査レポート

商品コード

1683497

アジア太平洋地域の動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 281 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

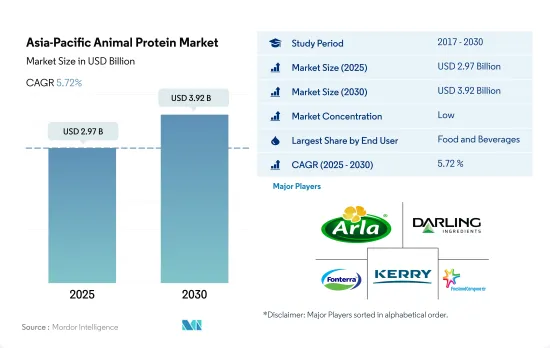

アジア太平洋地域の動物性タンパク質市場規模は2025年に29億7,000万米ドルと推定され、2030年には39億2,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは5.72%で成長すると予測されます。

革新的なクリーンラベル環境がセグメント成長を牽引

- アジア太平洋地域の動物性蛋白質市場では、F&B分野が依然として最大の動物性蛋白質消費者です。これはスナック、飲料、ベーカリーのサブセグメントによって大きく牽引され、2022年の数量シェアはそれぞれ26.93%、23.79%、20.5%でした。ベーカリーサブセグメントは、予測期間2023-2029年に金額ベースで最速のCAGR 5.70%を記録すると予測されています。カゼインとカゼイネートの用途が、この地域のベーカリー・サブセグメントを牽引しています。消化が容易なため、Threptin Biscuits(Diskettes)のような栄養価の高いビスケットでの利用が拡大しています。Threptin Biscuits(Diskettes)はビスケット1枚当たり1.5グラムのタンパク質価を高めることができ、子供から大人まで食べることができます。

- F&B分野では、乳清タンパク質とゼラチンの需要が高いです。この市場は、新しく改良されたプロテインを提供することで大きな利益を得ています。例えば、2020年にArla Foodsは100%天然たんぱく質で初のクリーンラベル環境ヨーグルトコンセプトNutrilac YO-4575を開発しました。同様に、2021年5月には、ダーリング・イングリーディエンツ社のRousselotブランドが、X-Pure(R)GelDAT-Gelatin Desaminotyrosineの発売により、精製された医薬品グレードの改良ゼラチンの品揃えを拡大しました。

- パーソナルケアと化粧品分野は、2023-2029年のCAGRが7.59%で、最も急成長する分野と予測されています。コラーゲンとゼラチンをベースとした美容・パーソナルケア製品の消費が増加しているため、パーソナルケア分野は、肌の滑らかさや髪のコンディショニングといった利点により、タンパク質の用途拡大を記録しています。しかし、可処分所得の増加と女性の労働人口の増加が主な促進要因となっています。例えば、アジア太平洋地域では、2021年に女性が同地域のGDPの約35~40%を占めています。

中国、インド、その他アジア太平洋地域のような国々からの需要の高まりがセグメント成長の原動力となります。

- アジア太平洋地域では、中国が2022年のアジア太平洋地域動物性タンパク質市場で最大のシェアを記録し、その牽引役となったのは、数量ベースで74.7%という大きなシェアを占める飲食品セクターであり、次いで16.75%のシェアを占める飼料セクターでした。飲食品部門は、動物性タンパク質の用途の主要なサブセグメントです。これは、乳清タンパク質、乳タンパク質、ゼラチン、コラーゲン、カゼインおよびカゼイン酸塩などの動物性タンパク質の溶解性が向上したためです。2022年の生産量が712万5,000トンで牛肉・仔牛肉生産国第2位の中国は、盛んな動物飼料部門を有し、動物性タンパク質の製剤への大幅な流入を記録しています。

- インドはこの地域で最も急成長している国であり、予測期間中のCAGRは金額ベースで6.26%を記録すると予測されています。特にソフトグミ菓子ではゲル化剤として機能し、マシュマロではその熱可逆性により安定剤やホイップ剤として機能するためです。新規参入企業も他業界の既存企業も、同国でサービスを拡大することで、市場開拓の可能性を生かすことができると思われます。

- 2022年のアジア太平洋地域の動物性タンパク質市場では、ホエイ・タンパク質の機能的利点が広く注目され、サプリメント・セグメントでのタンパク質消費量が高いことから、インドネシアがもう一つの成長国として浮上しました。ホエイプロテインはフィットネス志向のインドネシアの消費者に選ばれるようになり、同国ではホエイを含む製品の需要が生まれています。2020年8月現在、18歳以上の消費者の約30%がフィットネスクラブの会員となっています。こうした開発が市場開拓を後押ししています。

アジア太平洋地域の動物性タンパク質市場動向

動物性タンパク質消費において、乳清タンパク質と乳タンパク質のシェアが高まる見込み

- グラフに示した一人当たり消費量データには、アフガニスタン、オーストラリア、中国、インド、インドネシア、日本、マレーシア、ニュージーランド、パキスタン、フィリピン、韓国、タイ、ベトナムのデータが含まれています。日本はアジア市場におけるホエイプロテインの主要市場となっています。2020年のオリンピック東京大会やラグビーワールドカップなど、この地域で開催されたスポーツイベントの影響で、消費者はホエイ製品を選ぶようになっています。日本では、スポーツイベントと高齢者人口の増加が、それぞれスポーツ栄養と高齢者栄養における主なタンパク質サプリメントとして血清の消費を促進しています。日本の軍人の間でタンパク質の利点に対する意識が高まっていることも、ホエイプロテインの消費を後押ししています。インドは世界で最も急速に成長している国の一つです。

- 現在、中国の動物性タンパク質市場は着実な開拓を見せています。中国の生活水準が向上し、食品と医薬品に対する消費者の安全要求も改善されてきました。中国は、過去2年間のアフリカ豚熱による赤字と、過去2年間の動物性タンパク質の輸入増加により、豚の頭数が40%近く減少しています。

- ホエイタンパク濃縮物は、効率的で消化しやすい加工や安価な用途など、多様な利点を提供し、インドの市場成長に貢献しています。ホエイプロテイン濃縮物は、スポーツ栄養カテゴリーにおいて幅広い用途があります。インドの若者の間でスポーツ栄養の消費が増加しているため、濃縮乳清タンパク質の需要も増加しています。同国における一人当たりのホエイタンパク消費量は、2017年の14gから2022年には17.2gに増加しました。

動物性タンパク質原料メーカーの原料として牛乳と食肉生産が大きく貢献

- アジア太平洋地域全体から抽出したデータで示したグラフには、牛、鶏、豚の肉、牛や山羊の骨付き生乳、牛のスキムミルク、ホエイパウダーなど、動物性タンパク質製造に使用される原材料が含まれています。この地域の主要な生乳生産国はインドで、次いで中国です。2021年、インドの牛乳生産量は約9,600万トン、中国は約3,500万トンです。濃厚動物飼料施設(CAFO)や酪農生産工場のための工場農場がアジア全域で設立されており、その多くは何千頭もの牛を収容しています。過去10年間で生乳生産量が最も増加したのは東南アジアです。

- 中国の生乳生産量は、COVID-19の混乱により中国の生乳生産と消費が急速に伸びたため、生産性の向上により2021年には7.06%増加しました。輸入も消費者の需要と中国の製造業への要求によりプラス成長を見せています。乳タンパク質生産に主に使用される脱脂粉乳は、中国の食品産業が輸入脱脂粉乳に依存しているため増加しています。

- 牛、豚、鶏の動物性タンパク質は、コラーゲンとゼラチンの生産に使用されます。生産はインドや中国のような国々で著しく向上しており、政府のイニシアティブと各国での新しい近代的なと畜場の建設によって支えられています。2020年には、アフリカ豚熱が中国の養豚産業に影響を与え続けたため、豚の生産量全体が減少しました。

アジア太平洋地域の動物性たんぱく質産業の概要

アジア太平洋地域の動物性たんぱく質市場は断片化されており、上位5社で9.25%を占めています。この市場の主要企業は以下の通り。 Arla Foods amba, Darling Ingredients Inc., Fonterra Co-operative Group Limited, Kerry Group PLC and Koninklijke FrieslandCampina N.V.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タンパク質の種類

- カゼインおよびカゼイネート

- コラーゲン

- 卵タンパク質

- ゼラチン

- 昆虫プロテイン

- ミルクプロテイン

- ホエイプロテイン

- その他動物性タンパク質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Arla Foods amba

- Darling Ingredients Inc.

- Fonterra Co-operative Group Limited

- Gansu Hua'an Biotechnology Group

- Glanbia PLC

- Groupe LACTALIS

- Hilmar Cheese Company Inc.

- Jellice Pioneer Private Limited

- Kerry Group PLC

- Koninklijke FrieslandCampina N.V.

- Lacto Japan Co. Ltd

- Milligans Food Group Limited

- Morinaga Milk Industry Co. Ltd

- Nitta Gelatin Inc.

- Nutrition Technologies Group

- Olam International Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Animal Protein Market size is estimated at 2.97 billion USD in 2025, and is expected to reach 3.92 billion USD by 2030, growing at a CAGR of 5.72% during the forecast period (2025-2030).

Clean-label environment with innovations in the sector drove the segmental growth

- The F&B segment remained the largest consumer of animal proteins in the Asia-Pacific animal protein market. It was highly driven by the snacks, beverages, and bakery sub-segments, which accounted for shares of 26.93%, 23.79%, and 20.5%, respectively, by volume in 2022. The bakery sub-segment is projected to record the fastest CAGR of 5.70% by value during the forecast period 2023-2029. The application of casein and caseinates is driving the bakery sub-segment in the region. Its ease of digestion has expanded its use in highly nutritious biscuits like Threptin Biscuits (Diskettes), where it can increase the protein value of the biscuit to 1.5 grams per biscuit, which can be consumed by both children and adults.

- The F&B segment recorded high demand for whey protein and gelatin. The market largely benefits from introducing new and improved protein offerings. For instance, in 2020, Arla Foods created its first clean-label environment yogurt concept, Nutrilac YO-4575, which contains 100% natural whey protein. Similarly, in May 2021, Darling Ingredients Inc.'s Rousselot brand expanded its range of purified, pharmaceutical-grade and modified gelatin with the launch of X-Pure(R) GelDAT - Gelatin Desaminotyrosine.

- The personal care and cosmetics segment is projected to be the fastest-growing segment with a CAGR of 7.59% by value from 2023-2029. Owing to the rising consumption of collagen and gelatin-based beauty and personal care products, the personal care segment is recording increased protein applications due to its benefits, such as skin smoothing and hair conditioning. However, the rising disposable income and the growing women's working population are key drivers. For instance, in Asia-Pacific, women contributed around 35-40% of the region's GDP in 2021.

Growing demand from countries like China, India and rest of Asia-Pacific segments drive the segmental growth

- In the Asia-Pacific region, China recorded the largest share of the Asia-Pacific animal protein market in 2022, driven by the food and beverage sector, which held a significant share of 74.7% by volume, followed by the animal feed sector, with a share of 16.75% by volume. Beverages are the major sub-segment for applications of animal proteins in the food and beverages sector. This is due to improved solubility of animal proteins such as whey protein, milk protein, gelatin, collagen, and casein and caseinates. China, the second-largest beef- and veal-producing country, with a production of 7,125,000 ton in 2022, possesses a flourishing animal feed sector and is recording a significant influx of animal proteins in formulations.

- India is the fastest-growing country in the region and is projected to record a CAGR of 6.26% by value during the forecast period. During the review period, India saw the highest demand for gelatin protein, as it acts as a gelling agent, notably in soft gummy sweets, and acts as a stabilizer and whipping agent in marshmallows due to its thermo-reversible capabilities. Both new entrants and established businesses from other sectors may capitalize on the market's development potential by expanding their services in the country.

- Indonesia emerged as another growing country in the APAC animal protein market in 2022, driven by high protein consumption in the supplements segment because of the widespread attention that whey protein gained due to its functional benefits. It has become the choice of fitness-oriented Indonesian consumers, creating a demand for products containing whey in the country. As of August 2020, around 30% of consumers aged 18 or above had fitness club memberships. Such developments are boosting the market studied.

Asia-Pacific Animal Protein Market Trends

The share of whey and milk protein is expected to increase in animal protein consumption

- The per capita consumption data given in the graph includes data from Afghanistan, Australia, China, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, Philippines, the Republic of Korea, Thailand, and Vietnam. Japan has become the main market of whey proteins in the Asian market. Consumers are opting for whey products due to sporting events that took place in the region, like the Olympic Tokyo Games in 2020 and the Rugby World Cup. The sports events and the growing older population in Japan are driving serum consumption as the main protein supplement in sports nutrition and elderly nutrition, respectively. The increasing awareness about the benefits of proteins among the Japanese military is also boosting the consumption of whey proteins. India is one of the fastest-growing countries in the world.

- Currently, the animal protein market in China is witnessing a steady development. With improved living standards in China, consumer safety requirements for food and drugs have improved. China has seen a decline in its pig herd of almost 40% due to the deficit created by African Swine Fever in the last two years and an increase in the importation of animal proteins during the past two years.

- Whey protein concentrates offer versatile benefits, including efficient and easy-to-digest processing and inexpensive applications, which are contributing to India's market growth. They have a wide range of applications in the sports nutrition category. Owing to the increased consumption of sports nutrition among young Indians, the demand for whey protein concentrate also increased. The per capita consumption of whey protein in the country increased to 17.2g in 2022 from 14g in 2017.

Milk and meat production majorly contributes as raw material for animal protein ingredient manufacturers

- The raw materials used for animal protein production, such as meat from cattle, chickens, and pigs, along with bone raw milk of cattle and goats, skim milk of cows, and whey powder, are included in the graph given with data extracted from the whole of Asia-Pacific. India is the major milk-producing country in the region, followed by China. In 2021, India produced nearly 96 million tons of cow milk, while China produced around 35 million tons. Concentrated animal feeding operations (CAFOs) or factory farms for dairy production plants are being set up across Asia, many housing thousands of cows, by global and new national dairy corporations often working in partnership with governments. The strongest gains in milk production over the past decade have been registered in Southeast Asia.

- China's milk production in the region increased by 7.06% in 2021 due to improved productivity, as the COVID-19 disruption caused China's production and consumption of milk to grow rapidly. Imports are also showing positive growth due to consumer demand and requirements for the manufacturing industries in China. Skim milk powder, which is majorly used for milk protein production, has increased due to the Chinese food industry's dependence on imported skim milk powder.

- Animal protein from cattle, pigs, and chickens is used for collagen and gelatin production. Production is improving significantly in countries like India and China, and it is supported by government initiatives and the construction of new, modern slaughterhouses across the countries. Overall pig production declined in 2020 as African Swine Fever continued to impact China's hog industry.

Asia-Pacific Animal Protein Industry Overview

The Asia-Pacific Animal Protein Market is fragmented, with the top five companies occupying 9.25%. The major players in this market are Arla Foods amba, Darling Ingredients Inc., Fonterra Co-operative Group Limited, Kerry Group PLC and Koninklijke FrieslandCampina N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.4.4 Japan

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Arla Foods amba

- 5.4.2 Darling Ingredients Inc.

- 5.4.3 Fonterra Co-operative Group Limited

- 5.4.4 Gansu Hua'an Biotechnology Group

- 5.4.5 Glanbia PLC

- 5.4.6 Groupe LACTALIS

- 5.4.7 Hilmar Cheese Company Inc.

- 5.4.8 Jellice Pioneer Private Limited

- 5.4.9 Kerry Group PLC

- 5.4.10 Koninklijke FrieslandCampina N.V.

- 5.4.11 Lacto Japan Co. Ltd

- 5.4.12 Milligans Food Group Limited

- 5.4.13 Morinaga Milk Industry Co. Ltd

- 5.4.14 Nitta Gelatin Inc.

- 5.4.15 Nutrition Technologies Group

- 5.4.16 Olam International Limited

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms