|

市場調査レポート

商品コード

1692021

インドの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 205 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

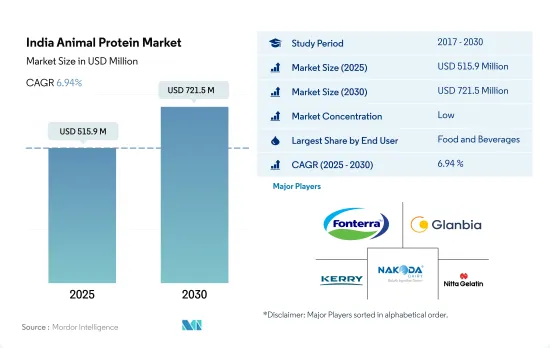

インドの動物性たんぱく質の市場規模は2025年に5億1,590万米ドルと推定され、2030年には7億2,150万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは6.94%で成長します。

消費者のたんぱく質ベースの食事への傾倒が全国のF&Bセクターを支配

- エンドユーザー別では、F&Bセクターが依然として最大であり、予測期間には数量ベースでCAGR 6.33%を記録すると予測されます。需要は主にスナック業界が牽引しているが、これは社会人の増加とヘルシーで持ち運び可能な食事オプションへの志向の高まりによるものです。インド人の約70%は、食生活の改善を優先することで、全体的な健康と免疫力の向上、ストレスや不安の軽減に力を入れたいと考えています。

- COVID-19の大流行は、地域の食品サービス部門の脆弱性を露呈させ、消費者をさらに小売部門へと向かわせた。この動向はRTE/RTC食品のサブセグメントに大きな恩恵をもたらし、2020年には数量ベースで前年比19.60%の2桁成長を達成しました。パンデミックは、消費者の外食を直接補う冷凍食品やピザなどの調理済み食品の需要をさらに押し上げました。国内では調理済み食品の消費が伸びているため、蛋白質の需要は今後も続くと予想されます。このため、RTE/RTC食品のサブセグメントは予測期間中に6.71%のCAGRで推移すると予測されます。

- パーソナルケアおよび化粧品セグメントは、予測期間中最も急成長し、CAGR 9.59%を記録すると予想されます。インドの化粧品分野では、天然成分へのニーズが動物性たんぱく質の用途を促進しています。また、肌の滑らかさや髪のコンディショニングなど、乳清たんぱく質の機能の増加も市場の需要を押し上げています。インドの消費者による生物活性成分への需要の高まりに伴い、メーカーはこれらの成分をこの分野に含めようとしています。

インドの動物性たんぱく質市場動向

一人当たりの動物性たんぱく質消費量の増加により、乳清たんぱく質とコラーゲンのサプライヤーにとって有利な環境が生まれます。

- 同国の食品産業は過去10年間で3倍に増加し、今後数年間も同様の傾向が続くと予想されます。機能性食品、飲食品、たんぱく質製品は、その健康上の利点から広く普及しつつあります。ホエイたんぱく質を含むパーソナルケア製品の需要も国内で増加しています。フィットネスに対する意識の高まりから、ボディビルダーや若いインド人の間でホエイたんぱく質パウダーの需要が増加しています。都市部のインド人の約33%は、ジムに簡単にアクセスできます。一方、インドでは、ジムに入会したこともフィットネス講師のレッスンを受けたこともない人口の25%が、2022年上半期に初めてジムに通い始めました。

- 市場を牽引しているのは、美容・健康サプリメント志向の高まりや研究開発活動の活発化といった要因です。コラーゲンの応用範囲は広く、主要製薬企業やバイオテクノロジー企業は、より優れたドラッグ・デリバリー・システムのためにコラーゲンをベースにした製品を取り入れています。しかし、天然素材やアーユルヴェーダ製品への嗜好が強く、動物性たんぱく質などの天然素材市場を押し上げています。

- 2020年には、動物性製品別の収量は生体重の50%から60%の間でした。皮革は通常、最も価値のある動物性製品別のひとつで、食用ゼラチンのような最終製品を生産します。皮の重量は生きた動物の重量の4%から11%です。生分解性の食品包装材料としてゼラチンの利用が増え、菓子類やスポーツ栄養製品の強化が進むことで、2024年から2029年にかけてインド市場に新たな展望が開けるかもしれないです。

インドの動物性たんぱく質産業の概要

インドの動物性たんぱく質市場は断片化されており、上位5社で6.01%を占めています。この市場の主要企業は以下の通りです。 Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC, Nakoda Dairy Private Limited and Nitta Gelatin Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- たんぱく質タイプ

- カゼインとカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他動物性たんぱく質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- EnNutrica

- Fonterra Co-operative Group Limited

- Glanbia PLC

- Hilmar Cheese Company Inc.

- Jellice Pioneer Private Limited

- Kerry Group PLC

- Nakoda Dairy Private Limited

- Nitta Gelatin Inc.

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The India Animal Protein Market size is estimated at 515.9 million USD in 2025, and is expected to reach 721.5 million USD by 2030, growing at a CAGR of 6.94% during the forecast period (2025-2030).

Consumer inclination towards protein-based meals dominates the F&B sector across the country

- By end user, the F&B sector remained the largest, and it is anticipated to register a CAGR of 6.33%, by volume, in the forecast period. The demand was majorly led by the snacks industry owing to the increasing number of working professionals and their widening inclination toward healthy, on-the-go meal options. About 70% of Indians are willing to focus on improving their overall health and immunity and reducing stress and anxiety by prioritizing dietary changes.

- The COVID-19 pandemic exposed the vulnerability of the regional foodservice sector, which further drove consumers toward the retail sector. This trend largely benefitted the RTE/RTC foods sub-segment, which saw double-digit growth of 19.60% by volume in 2020 compared to the previous year. The pandemic further bolstered the demand for ready-to-cook food products, such as frozen meals and pizzas, directly positioned to compensate for consumers' eating out. The demand for protein is expected to continue due to the growing consumption of ready-to-eat foods in the country. Thus, the RTE/RTC foods sub-segment is projected to record a CAGR of 6.71% during the forecast period.

- The personal care and cosmetics segment is expected to grow the fastest and record a CAGR of 9.59% during the forecast period. The need for all-natural components in the Indian cosmetics sector is driving applications of animal protein. The increasing functions of whey protein, such as skin smoothening and hair conditioning, are also boosting demand in the market. With the rise in demand for bioactive ingredients from Indian consumers, manufacturers are attempting to include these ingredients in the sector.

India Animal Protein Market Trends

Increase in per capita animal protein consumption to create a favorable environment for whey protein and collagen suppliers

- The country's food industry has tripled in the past decade and is expected to follow the same trend over the coming years. Functional foods, beverages, and protein products are becoming widely popular due to their health benefits. The demand for personal care products containing whey protein has also increased in the country. Due to the country's increasing awareness of fitness, the demand for whey protein powder among bodybuilders and young Indians is increasing. About 33% of urban Indians have easy access to a gym. Meanwhile, 25% of the population in India who had never joined a gym or taken a lesson from a fitness teacher began going to the gym for the first time in the first half of 2022.

- The market is driven by factors such as a growing inclination toward beauty and health supplements and increased R&D activities. The spectrum of applications of collagen is broad, with leading pharmaceutical and biotechnological companies incorporating collagen-based products for better drug delivery systems. However, there is a strong preference for natural and ayurvedic products, boosting the market for natural ingredients such as animal proteins.

- In 2020, the yield of animal byproducts ranged between 50% and 60% of the live weight. Hides and skins are typically among the most valuable animal byproducts, producing end products like edible gelatin. The weight of the hides ranges from 4% to 11% of the live animal's weight. Increased usage of gelatin as a viable biodegradable food packaging material and a boost in fortified confectionery and sports nutrition products may lead to new prospects for the Indian market from 2024 to 2029.

India Animal Protein Industry Overview

The India Animal Protein Market is fragmented, with the top five companies occupying 6.01%. The major players in this market are Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC, Nakoda Dairy Private Limited and Nitta Gelatin Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 India

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 EnNutrica

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Glanbia PLC

- 5.4.4 Hilmar Cheese Company Inc.

- 5.4.5 Jellice Pioneer Private Limited

- 5.4.6 Kerry Group PLC

- 5.4.7 Nakoda Dairy Private Limited

- 5.4.8 Nitta Gelatin Inc.

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms