|

市場調査レポート

商品コード

1690985

ドイツの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Germany Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの動物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 233 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

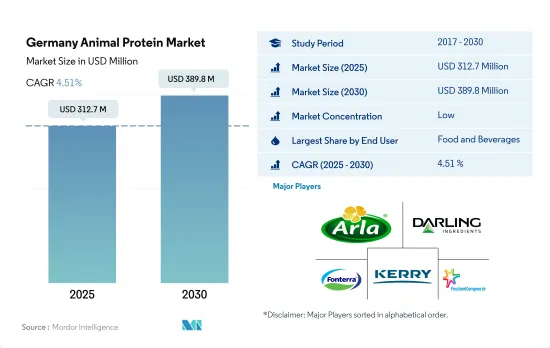

ドイツの動物性たんぱく質市場規模は2025年に3億1,270万米ドルと推定・予測され、2030年には3億8,980万米ドルに達し、予測期間(2025-2030年)のCAGRは4.51%で成長すると予測されます。

パーソナルケアと化粧品分野は、コラーゲンベースの美容製品、すなわち肌に良い製品に対する消費者の嗜好の高まりにより、予測期間中に売上高が増加すると予想されます。

- エンドユーザーの中では、2022年にF&Bセグメントが様々な動物性たんぱく質のアプリケーションを支配しました。これは主にベーカリーサブセグメントが市場を独占しているためであり、2022年の市場シェアは約30%です。ベーカリー分野での動物性たんぱく質の用途は、機能性パンへの需要の高まりに後押しされて増加しています。現地の消費者は、主にたんぱく質など、その他の健康特典を備えた製品を強く好むようになっています。そのため、ユーザーは高炭水化物ベーカリー製品を高たんぱく質ベーカリー製品に置き換えつつあります。飲料におけるホエイプロテイン需要は、国内での健康意識の高まりとともに増加しています。有機ホエイや牧草飼育ホエイなどの原料は、健康と倫理的な懸念から注目されています。

- 成長率では、パーソナルケアと化粧品分野が2番目に急成長しています。予測期間中、金額ベースでCAGR 4.19%を記録すると予測されています。コラーゲンは、毛包の損傷や白髪を防ぐと同時に、皮膚の弾力性を強化し、潤いを与える特性があるため、パーソナルケア用途に使用される最も一般的な動物性たんぱく質です。

- 2022年の動物性たんぱく質市場では、サプリメント部門が金額ベースで第2位のシェアを占めました。同分野はスポーツ/パフォーマンス栄養セグメントによって大きく支配されており、予測期間中のCAGRは6.24%(金額ベース)で市場を牽引すると予測されています。健康への関心の高まり、肥満の有病率の上昇、国内のフィットネスクラブの増加などが、特にスポーツ栄養カテゴリーの需要増につながっています。全国のジム会員数は1,166万人で、2021年にはドイツ人口の約14%がジム会員となり、スポーツ栄養サプリメントの需要を牽引しています。

ドイツの動物性たんぱく質市場動向

動物性たんぱく質消費の成長が原料部門の主要企業にチャンスをもたらす

- ドイツには420万頭の牛を飼養する巨大な酪農産業があり、その規模は140億米ドルに達します。IOP Publishingによると、一人当たりの消費量は一日平均約104g、一人当たり年間6.1kgのたんぱく質Nを摂取しています。ドイツの乳製品は大部分が輸出されており(輸出全体の約15%)、フランス、ニュージーランド、オランダ、ベルギー、米国、デンマークがこれに続きます。自由貿易政策はドイツに大きな利益をもたらし、輸出を容易にしました。余計な関税をかけないという措置により、世界最大の輸出国となっています。

- 高度に成熟した飲食品業界は、健康志向の高い人々から高品質の蛋白質原料の大量需要を目の当たりにしました。同国ではパーソナルケアやスポーツ栄養製品の人気が高まり、一人当たりの動物性たんぱく質消費量は2016年の47gから2021年には51.8gに増加します。消費者がイノベーションの背後にある科学的研究を求めるようになっているため、イノベーションに対する強い要求がプライベート・ラベルの市場成長を妨げています。しかし、脱脂粉乳は主に乾燥エキス含量やたんぱく質含量を標準化するために使用され、再構成乳をベースにした様々な製品に様々な用途で使用されています。

- ドイツは欧州最大のフィットネス市場で、1,000万人以上がジムに通っています。人々は、身体の栄養要求を満たすために、ホエイプロテイン、カゼイン、カゼイネート、乳製品プロテインのようなサプリメントを好んで摂取しています。ホエイプロテインの中では、分離ホエイプロテインが市場を独占しており、たんぱく質含有量の90%以上を占めています。カゼインは消化が遅いたんぱく質であるため、カゼインとカゼイン酸塩はアスリートに好まれています。

食肉と牛乳の生産は、植物性たんぱく質原料メーカーの原料として大きく貢献しています。

- ドイツはEUにおける生乳の主要生産国であり、2020年にはEUにおける生乳出荷量の21%以上を占める。ドイツでは畜産農家数が減少しているが、平均的な畜産規模は増加しています。生乳生産量の増加は、牛1頭当たりの生乳生産量の増加に起因しています。長年にわたり、牛乳生産はドイツ北西部と南部の草原地帯に集中しています。

- 赤身肉の主な生産品目は鶏肉であり、次いで豚肉、牛肉です。ドイツの牛肉生産は専門的な体制を整えています。繁殖、農業経営における人工授精、家畜の飼育、食肉処理、加工、そして性能と品質のチェックはすべて、非常に高い基準に従って行われます。約64,500の農業関連企業、合計350万頭の牛が、肉と乳の性能試験の対象となっています。2022年、ドイツでは13万3,000の企業で1,100万頭の牛が飼われていました。これにより、ドイツは欧州で2番目の牛肉生産国となりました。

- 2022年、ドイツでは約4,700万頭の豚が屠殺され、450万トンの豚肉が生産されました。したがって、ドイツは欧州最大の豚肉生産国です。国際的には、ドイツは中国、米国に次いで第3位です。豚の在庫は主にドイツ北西部に集中しています。豚の飼養頭数の約30%を占めるニーダーザクセン州は、ドイツで最も重要な生産地であり、ノルトライン=ヴェストファーレン州とバイエルン州が僅差でこれに続きます。

ドイツ動物性たんぱく質産業の概要

ドイツの動物性たんぱく質市場は断片化されており、上位5社で31.32%を占めています。この市場の主要企業は以下の通りです。 Arla Foods amba, Darling Ingredients Inc., Fonterra Co-operative Group Limited, Kerry Group PLC and Koninklijke FrieslandCampina N.V.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- ドイツ

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- たんぱく質タイプ

- カゼインとカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫プロテイン

- ミルクプロテイン

- ホエイプロテイン

- その他動物性たんぱく質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Agrial Enterprise

- Arla Foods amba

- Darling Ingredients Inc.

- Fonterra Co-operative Group Limited

- GELITA AG

- Hoogwegt Group

- Kerry Group PLC

- Koninklijke FrieslandCampina N.V.

- Lactoprot Deutschland GmbH

- Lapi Gelatine SpA

- MEGGLE GmbH & Co.KG

- Morinaga Milk Industry Co. Ltd

- Tessenderlo Group

- Ynsect

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Germany Animal Protein Market size is estimated at 312.7 million USD in 2025, and is expected to reach 389.8 million USD by 2030, growing at a CAGR of 4.51% during the forecast period (2025-2030).

Personal care and cosmetic segment is expected to gain higher sales in forecast period due to growing consumer preferences for collagen-based beauty products i.e. beneficial for skin

- Among end users, the F&B segment dominated the application of various animal proteins in 2022. This is majorly due to the bakery sub-segment dominating the market, with a market share of around 30% in 2022. The application of animal proteins in the bakery sector is rising, aided by pumped demand for functional bread. Local consumers are developing a strong liking for products with additional health benefits, mainly protein. Thus, users are replacing high-carb bakery goods with high-protein bakery goods. Whey protein demand in beverages is rising with the growing health awareness in the country. Ingredients, such as organic and grass-fed whey, have gained prominence due to health and ethical concerns.

- In terms of growth rate, the personal care and cosmetics segment is the second fastest-growing segment. It is projected to register a CAGR of 4.19%, by value, during the forecast period. Collagen is the most common animal protein used for personal care applications owing to its skin elasticity strengthening and hydration properties while preventing hair follicle damage and greying.

- The supplements segment held the second-largest share of the animal protein market, by value, in 2022. It was majorly dominated by the sports/performance nutrition segment, which is anticipated to drive the market with a CAGR of 6.24%, by value, in the forecast period. Rising health concerns, a higher prevalence of obesity, and the rise in fitness clubs in the country are leading to increased demand for the segment, especially in the sports nutrition category. With 11,660,000 gym members nationwide, around 14% of the German population were gym members in 2021, driving the demand for sports nutrition supplements.

Germany Animal Protein Market Trends

The growth of animal protein consumption fuels opportunities for key players in the ingredients segment

- Germany has a huge dairy farming industry containing 4.2 million cows, valued at USD 14 billion. According to the IOP Publishing, per capita consumption is associated with an average daily protein intake of around 104 g per capita daily or 6.1 kg protein-N per capita a year. Germany's dairy products are largely exported (around 15% of all its exports), followed by France, New Zealand, the Netherlands, Belgium, the United States, and Denmark. The free trade policy hugely benefited Germany, providing easy exports. The country's measure of no extra tariffs makes it the largest exporter in the world.

- The highly matured food and beverage industry witnessed a massive demand for high-quality protein ingredients from the health-conscious population. The popularity of personal care and sports nutrition products increased in the country, increasing the per capita consumption of animal protein from 47 g in 2016 to 51.8 g in 2021. The strong demand for innovation prevents private labels from growing in the market, as consumers are increasingly looking for scientific studies behind the innovation. However, skimmed milk powder is used mainly to standardize dry extract content or protein content, and it is used in various applications in various products based on reconstituted milk.

- Germany is Europe's largest fitness market, with over 10 million people attending the gym. People prefer taking supplements like whey proteins, casein and caseinates, and dairy proteins to fulfill the body's nutrition demands. Among whey proteins, isolated whey protein dominates the market, containing more than 90% of the protein content. Casein and caseinates are highly preferred by athletes as casein is a slow-digesting protein.

Meat and milk production contributes majorly as raw material for plant protein ingredients manufacturers

- Germany is the leading producer of milk in the European Union, accounting for more than 21% of milk deliveries in the European Union in 2020. Although the country has been observing a decline in the count of cattle farms, the average size of the farms is witnessing an upsurge. The rise in milk production is attributed to the escalated volume of milk production per cow. Over the years, milk production has been concentrated in the grassland regions of northwestern and southern Germany.

- Chicken meat is a largely produced type of red meat, followed by pig meat and cattle meat. Beef production in Germany has a professional setup. Breeding, insemination in agricultural businesses, animal keeping, slaughtering, processing, and performance and quality checks are all subject to very high standards. Some 64,500 agrarian companies with a total of 3.5 million cows are subject to meat and milk performance tests. In 2022, in Germany, 11 million cows were kept in 133,000 businesses. This made Germany the second biggest producer of cattle meat in Europe.

- In 2022, almost 47 million pigs were slaughtered in Germany to produce 4.5 million tonnes of pork. Germany, therefore, is the largest pork producer in Europe. Internationally, Germany is third behind China and the United States. The stock of pigs is mainly concentrated in the North West of Germany. With around 30% of the stock of pigs, Lower Saxony is the most essential production location in Germany, closely followed by North Rhine-Westphalia and Bavaria.

Germany Animal Protein Industry Overview

The Germany Animal Protein Market is fragmented, with the top five companies occupying 31.32%. The major players in this market are Arla Foods amba, Darling Ingredients Inc., Fonterra Co-operative Group Limited, Kerry Group PLC and Koninklijke FrieslandCampina N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Germany

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Arla Foods amba

- 5.4.3 Darling Ingredients Inc.

- 5.4.4 Fonterra Co-operative Group Limited

- 5.4.5 GELITA AG

- 5.4.6 Hoogwegt Group

- 5.4.7 Kerry Group PLC

- 5.4.8 Koninklijke FrieslandCampina N.V.

- 5.4.9 Lactoprot Deutschland GmbH

- 5.4.10 Lapi Gelatine SpA

- 5.4.11 MEGGLE GmbH & Co.KG

- 5.4.12 Morinaga Milk Industry Co. Ltd

- 5.4.13 Tessenderlo Group

- 5.4.14 Ynsect

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms