|

市場調査レポート

商品コード

1687313

英国のスナックバー:市場シェア分析、産業動向・統計、成長予測(2025~2030年)UK Snack Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のスナックバー:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

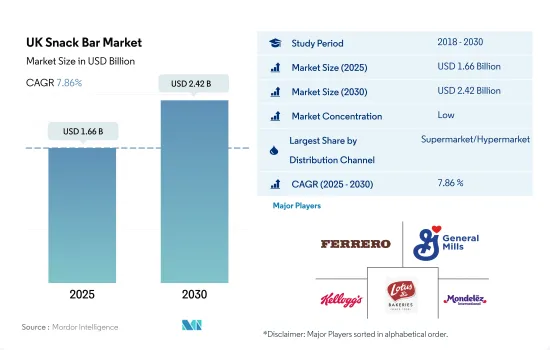

英国のスナックバーの市場規模は2025年に16億6,000万米ドルと推定され、2030年には24億2,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは7.86%で成長する見込みです。

スーパーマーケットやハイパーマーケットは、全国的な強い普及率とスナックバーに対する割引の提供により、大きなシェアを占めました。

- スーパーマーケットやハイパーマーケットは英国のスナックバー市場で最大のチャネルです。流通チャネル全体では金額ベースで53%のシェアを占めています。これらのチャネルは、嗜好性の高いスナック製品の適切な陳列と品揃えにより、超大型のショッピング体験を提供しています。これらのチャネルは、特に大都市や大都市圏に近接しているため、消費者の間食習慣に影響を与えるという利点があります。国内で営業している人気店舗には、Tesco PLC、J Sainsbury PLC、Asda Stores Ltd、Wm Morrison Supermarkets PLC、Lidl、Aldiなどがあります。2022年には、TescoとAsdaが3,456店舗、Morrisonが497店舗を英国内に展開していました。

- コンビニエンスストアは、スーパーマーケット、ハイパーマーケットに次いで、スナックバーの購入に広く選ばれている流通チャネルです。コンビニエンスストアを通じたスナックバーの販売量は、2024年には35.56%の数量シェアを記録すると推定されています。消費者がコンビニエンスストアを好むのは、従来の店舗に比べてアクセスが簡単で営業時間が長いためです。2022年には、英国全土に48,590店のコンビニエンスストアがありました。

- オンライン小売チャネルは、同国で最も急成長しているセグメントと考えられています。スナックバーの売上は、2023~2024年にかけて、金額ベースで6.58%の割合でこれらのチャネルを通じて成長すると予測されます。これは、消費者がインターネットでの購入を好むためで、特にお菓子など、メーカー名、ブランドポジショニング、イメージ、包装デザインなどの点で馴染みのある商品が好まれるためです。

英国のスナックバー市場動向

クリーンラベル、ナチュラル、オーガニックといったヘルシーなスナックバー製品が全国に導入された結果、売上が増加しました。

- 成人の平均食事時間は、特に労働者階級の消費者の間で短くなっており、ポーションコントロールのための代替品への欲求が高まっています。スナックバーは朝食の代替食品として人気が高まっています。

- フェアトレードのスナックバーやその他のクリーンラベリングの需要は、消費者の購買を左右する重要な動向であり、長年にわたって市場を前進させ続けると予想されます。2023年には、英国の77%の人々がスナックバーを含むフェアトレード製品を選ぶようになり、倫理的かつ持続可能な方法で生産された製品に対する消費者の継続的なコミットメントが実証されます。

- 英国の消費者のスナックバーの購買行動において、価格は重要な要素です。プレミアムスナックバーの動向は、同国の市場成長と消費者の認知を促進すると予想されます。

- 英国の消費者は、さまざまな健康効果を持つ多種多様なスナックバーを消費しています。例えば、高タンパク質(20グラム以上)のバーは激しい運動の後に食べることを目的としているため、活動的なタイプに最適です。

英国のスナックバー業界の概要

英国のスナックバー市場は細分化されており、上位5社で28.55%を占めています。この市場の主要企業はFerrero International SA、General Mills Inc.、Kellogg Company、Lotus Bakeries、Mondelez International Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- タイプ別

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 流通チャネル別

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Abbott Laboratories

- Associated British Foods plc

- August Storck KG

- Ferrero International SA

- General Mills Inc.

- Kellogg Company

- Lotus Bakeries

- Mars Incorporated

- Mondelez International Inc.

- PepsiCo Inc.

- Post Holdings Inc.

- Simply Good Foods Co.

- The Hershey Company

- Wholebake Limited

- YIldIz Holding AS

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 61163

The UK Snack Bar Market size is estimated at 1.66 billion USD in 2025, and is expected to reach 2.42 billion USD by 2030, growing at a CAGR of 7.86% during the forecast period (2025-2030).

Supermarket/hypermarket accounted for a major share due to strong penetration across the country coupled with discounts offered on the snack bars

- Supermarkets/hypermarkets are the largest channels in the UK snack bar market. The channel held the major share of 53% by value in the overall distribution channels segment. These channels provide a super-sized shopping experience with suitable displays and assortments of indulgent snacking products. The proximity factor of these channels, especially in bigger cities and metropolitan areas, gives them an added advantage of influencing the snacking habits of consumers. Some of the popular stores operating across the country are Tesco PLC, J Sainsbury PLC, Asda Stores Ltd, Wm Morrison Supermarkets PLC, Lidl, and Aldi. In 2022, Tesco and Asda had 3,456 stores and 497 Morrisons stores in the United Kingdom.

- Convenience stores are the second most widely preferred distribution channels after supermarkets and hypermarkets for the purchase of snack bars. The volume sales of snack bars through convenience stores is estimated to register a 35.56% volume share in 2024. Consumer preference toward convenience stores is due to ease of access and being open for longer hours compared to traditional stores. In 2022, there were 48,590 convenience stores located across the United Kingdom.

- The online retail channel is considered the fastest-growing segment across the country. Snack bar sales are anticipated to grow through these channels at a rate of 6.58% from 2023 to 2024 in value terms due to consumers' preference for buying on the internet, especially the goods they are familiar with, such as confectionaries, in terms of the manufacturer's name, brand positioning, image, and packaging design.

UK Snack Bar Market Trends

The introduction of healthy variants like clean label, natural, and organic snack bar products across the country resulted in higher sales

- Adults' average mealtimes are getting shorter, especially among consumers in the working class, and there is an increasing desire for alternatives for portion control. Snack bars have grown in popularity as acceptable alternatives to breakfast foods.

- The demand for fair trade snack bars and other clean labeling is expected to be the key trends that influence the consumer's purchase and continue to influence the market forward over the years. In 2023, 77% of people in the UK will choose Fairtrade products, including snack bars, demonstrating continued consumer commitment to products that are ethically and sustainably produced.

- Price is a significant factor in consumer buying behavior for snack bars in the United Kingdom. The trend of premium snack bars is expected to drive market growth and consumer recognition in this country.

- Consumers in the United Kingdom consume many kinds of snack bars with different health benefits. For instance, bars that are high in protein (20 grams or more) are aimed to be eaten after intense exercise, so they are perfect for active types.

UK Snack Bar Industry Overview

The UK Snack Bar Market is fragmented, with the top five companies occupying 28.55%. The major players in this market are Ferrero International SA, General Mills Inc., Kellogg Company, Lotus Bakeries and Mondelez International Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Cereal Bar

- 5.1.2 Fruit & Nut Bar

- 5.1.3 Protein Bar

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Abbott Laboratories

- 6.4.2 Associated British Foods plc

- 6.4.3 August Storck KG

- 6.4.4 Ferrero International SA

- 6.4.5 General Mills Inc.

- 6.4.6 Kellogg Company

- 6.4.7 Lotus Bakeries

- 6.4.8 Mars Incorporated

- 6.4.9 Mondelez International Inc.

- 6.4.10 PepsiCo Inc.

- 6.4.11 Post Holdings Inc.

- 6.4.12 Simply Good Foods Co.

- 6.4.13 The Hershey Company

- 6.4.14 Wholebake Limited

- 6.4.15 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms