|

市場調査レポート

商品コード

1684022

中東のスナックバー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Middle East Snack Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のスナックバー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 184 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

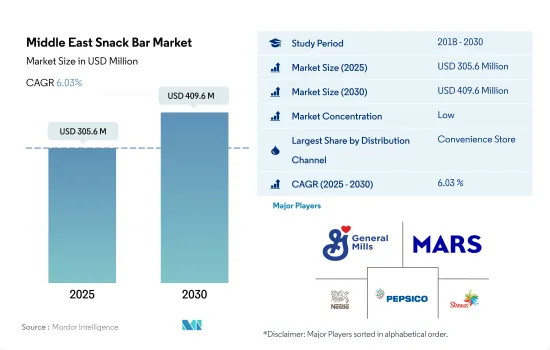

中東のスナックバーの市場規模は2025年に3億560万米ドルと推定・予測され、2030年には4億960万米ドルに達し、市場推計・予測期間(2025-2030年)のCAGRは6.03%で成長すると予測されます。

コンビニエンスストアが市場シェアの50%以上を占める。

- 中東では、小売事業全体が2022年と比較して2023年には4.87%の成長を維持しました。同市場では、消費者の利便性の高いショッピング施設への志向が高まっており、成長が見込まれています。対面ショッピングへの関心の高まりや、割引オファーへの需要などの側面が、小売業界を劇的に牽引する可能性が高いです。2024年から2027年にかけて、中東の小売部門全体は数量シェアで6.10%の成長を達成すると推定されます。

- 小売業全体では、コンビニエンスストアが一等地に店舗を構えているため、2023年には数量ベースで最大の小売業になると考えられています。有名な店舗としては、Meed Murabbah、KSA、You Martなどがあります。2026年までに、この地域のコンビニエンスストア・セグメントは、2025年と比較して数量シェアで5.42%の成長を維持すると推定されます。

- スーパーマーケットとハイパーマーケットは、中東のスナックバー業界では第2位の規模を誇る。これらの店舗では、幅広い種類のスナックバー商品を革新的なオファーとともに顧客に提供する傾向があります。スーパーマーケットとハイパーマーケットにおけるスナックバー製品の販売量は2022年に4.18%増加したと報告されており、中東では2026年から2028年にかけてCAGR 19.7%を記録すると予測されています。

- オンライン小売またはeコマース小売は、この地域で最も急成長している小売部門と考えられています。eコマース事業の2023年からのCAGRは6.32%です。eコマース・ウェブサイトの加速に影響を与えている主な側面は、自宅でのショッピングや24時間365日の商品購入オプションなど、これらのウェブサイトが提供する利便性の高さに関連しています。さらに、インターネット・ユーザーの増加がこの産業を大きく牽引すると予想されます。

この地域の消費者の70%以上が健康とウェルネスにお金を使うことを望んでおり、中東では市場の急成長が見られます。

- 中東では、スナックバー分野は2023年には2022年比で5.8%という良好な成長率を記録したが、これは主に健康的な食事動向に対する消費者の意識の高まりに加え、多忙なライフスタイルを送る若者や勤労消費者の存在が大きいためです。また、健康的なライフスタイルを維持するために、多くの人が食事中にカロリーを計算し、それに応じて献立を計画しています。2023年には、この地域の消費者の約70%が、病気や不純物の蔓延を受けて健康志向が高まるにつれて、健康とウェルネスへの支出を増やす意向を示しています。

- 国別では、サウジアラビアがスナックバー市場で最も高い消費量に支えられて同地域の主要シェアを占めており、2023年の前年比成長率は2022年比で4.22%を記録しました。スナックバーの中でも、プロテイン・バーはタンパク質が強化された他の製品よりも健康的であると消費者は認識しています。サウジアラビアでスナックバーの売上を伸ばすため、メーカーは昆虫、大豆、エンドウ豆、その他の植物性タンパク質などの代替タンパク源を取り入れるなど、革新的な風味を提供しています。スナックバーの味や栄養面での利点以外にも、メーカーはクリーンなラベリングや革新的なパッケージングを通じて、製品の利点をより分かりやすく伝えることに注力しています。

- オマーンは最も急成長しているセグメントであり、2024年と比較して2030年には9%の金額成長率を達成すると予想され、予測期間中のCAGRは7.8%となる見込みです。同国のスナックバー分野は、ライフスタイルや消費者の嗜好の進化に加え、食の選択における欧米文化の影響により急成長を遂げています。

中東のスナックバー市場動向

世界的・地域的なスナックバーブランドを幅広く扱う組織化された小売ネットワークの強力な浸透が市場成長に重要な役割を果たしています。

- 同地域におけるスナックバーの消費は、少量の食品を摂取するという個人のライフスタイルの変化により増加傾向にあります。プロテイン・バーは、スナックバーの中でもより健康的な代替品として需要が増加しています。

- 体に良い」という謳い文句は、ここ数年、新製品の革新や発売の主なセールスポイントとなっています。高タンパク質バーからアレルゲン無添加の食物繊維バーまで幅広い選択肢があり、これらのバーは消費者にとってフィットネス、ダイエット、健康全般を改善する便利な方法であり続けています。

- 2023年、中東では平均スナックバーが1.36米ドルから10.89米ドルの間で販売されます。スナックバーは高級な高級焼き菓子と考えられているが、価格が高いため中東の一般消費者にはあまり人気がないです。

- スナックバーはよく作られる汎用性の高い製品であり、シリアル、果物、ナッツは健康的な栄養素、生物活性化合物、食物繊維を消費者に届ける理想的な食品形態です。

中東のスナックバー産業の概要

中東のスナックバー市場は断片化されており、上位5社で30.11%を占めています。この市場の主要企業は以下の通りです。 General Mills Inc., Mars Incorporated, Nestle SA, PepsiCo Inc. and Strauss Group Ltd(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コンフェクショナリー種類

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 流通チャネル

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

- 国

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Associated British Foods PLC

- Bright Lifecare Private Limited

- Ferrero International SA

- General Mills Inc.

- Glanbia PLC

- Kellogg Company

- Mars Incorporated

- Mondelez International Inc.

- Naturell India Pvt. Ltd

- Nestle SA

- PepsiCo Inc.

- Post Holdings Inc.

- Riverside Natural Foods Ltd

- Simply Good Foods Co.

- Strauss Group Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001794

The Middle East Snack Bar Market size is estimated at 305.6 million USD in 2025, and is expected to reach 409.6 million USD by 2030, growing at a CAGR of 6.03% during the forecast period (2025-2030).

Convenience stores account for more than 50% market share as consumers are inclined toward convenient and in-person shopping at discounted offers

- In the Middle East, the overall retailing segment maintained a growth of 4.87% in 2023 compared to 2022. The growth is anticipated with the consumers' growing inclination for convenience shopping facilities in the market. Aspects such as rising interest in in-person shopping and demand for discount offers, etc., are likely to drive the retailing industry drastically. During 2024-2027, it is estimated that the overall retailing unit in the Middle East will attain a growth of 6.10% by volume share.

- Under the overall retailing segment, the convenience store segment was considered the largest retailing unit by volume in 2023 because of its establishment in prime locations. Some of the famous stores are Meed Murabbah, KSA, You Mart, etc. By 2026, the convenience store segment in this region is estimated to preserve a growth of 5.42% by volume share compared to 2025.

- Supermarkets and hypermarkets are marked as the second-largest units in the Middle Eastern snack bar industry. These stores tend to offer a wide range of snack bar products with innovative offers for their customers. It is reported that the sales volume of snack bar products in supermarkets and hypermarkets grew by 4.18% in 2022, and it is anticipated to register a CAGR of 19.7% during 2026-2028 in the Middle East.

- Online retailing or e-commerce retailing is considered the fastest-growing retailing unit in this region. The e-commerce business held a CAGR of 6.32% from 2023. The major aspect influencing the acceleration of e-commerce websites is associated with the greater convenience offered by these websites, such as at-home shopping and 24*7 product purchasing options. In addition, the increasing number of internet users is expected to drive this industry significantly.

With more than 70% of the region's consumers willing to spend on health and wellness, Middle East has observed a surge in the market growth

- In the Middle East, the snack bar segment witnessed a favorable growth rate of 5.8% in 2023 compared to 2022, primarily growing consciousness among consumers about healthy eating trends together with a significant presence of youth and working consumers who have a hectic lifestyle. Also, many people count calories while eating and plan their menu accordingly to maintain a healthy lifestyle. In 2023, about 70% of the consumers in the region were willing to increase their spending on health and wellness as they become more health-conscious following the prevalence of ailments and adulteration.

- By country, Saudi Arabia holds the major share in the region supported by the highest consumption of snack bars in the market, registering a Y-o-Y growth rate of 4.22% in 2023, relative to 2022. Among all the available snack bar variants, consumers in the market perceive protein bars as healthier than any other product that is fortified with protein. In order to increase the sales of snack bars in Saudi Arabia, manufacturers are providing innovative flavors such as the incorporation of alternative protein sources like insects, soy, peas, and other plant-based proteins. Apart from the taste and nutritional benefits of the snack bars, makers are focusing on better communicating the product benefits through clean labeling and innovative packaging efforts.

- Oman is likely to be the fastest-growing segment and is expected to achieve a value growth rate of 9% in 2030 compared to 2024, and it is likely to attain a CAGR of 7.8% during the forecast period. The snack bar sector in the country is experiencing rapid growth due to the evolving lifestyle and consumer preferences, as well as the influence of Western culture in terms of food choices.

Middle East Snack Bar Market Trends

Strong penetration of organized retail networks carrying a wide range of global and regional snack bar brands plays a vital role in the market's growth

- Consumption of snack bars in the region has been on the rise due to the changing lifestyles of individuals, which involve consuming smaller portions of food. Protein bars, being a healthier alternative in the snack bar range, have seen an increase in demand.

- The "good for you" claims have been the primary selling point for new product innovations and launches in the past years. With a wide range of options available, ranging from high-protein bars to added-fiber bars with no allergens, these bars remain a convenient way for consumers to improve their fitness, diet, and overall health.

- In 2023, an average snack bar will range between USD 1.36 and USD 10.89 in the Middle East. A snack bar is considered to be a high-end, premium baked product, which is less popular among the average Middle Eastern consumers due to its high price.

- Snack bars are versatile products often made, with cereals, fruits, and nuts being an ideal food format to deliver healthy nutrients, bioactive compounds, and dietary fiber to consumers.

Middle East Snack Bar Industry Overview

The Middle East Snack Bar Market is fragmented, with the top five companies occupying 30.11%. The major players in this market are General Mills Inc., Mars Incorporated, Nestle SA, PepsiCo Inc. and Strauss Group Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Cereal Bar

- 5.1.2 Fruit & Nut Bar

- 5.1.3 Protein Bar

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Bahrain

- 5.3.2 Kuwait

- 5.3.3 Oman

- 5.3.4 Qatar

- 5.3.5 Saudi Arabia

- 5.3.6 United Arab Emirates

- 5.3.7 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Associated British Foods PLC

- 6.4.2 Bright Lifecare Private Limited

- 6.4.3 Ferrero International SA

- 6.4.4 General Mills Inc.

- 6.4.5 Glanbia PLC

- 6.4.6 Kellogg Company

- 6.4.7 Mars Incorporated

- 6.4.8 Mondelez International Inc.

- 6.4.9 Naturell India Pvt. Ltd

- 6.4.10 Nestle SA

- 6.4.11 PepsiCo Inc.

- 6.4.12 Post Holdings Inc.

- 6.4.13 Riverside Natural Foods Ltd

- 6.4.14 Simply Good Foods Co.

- 6.4.15 Strauss Group Ltd

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms