|

市場調査レポート

商品コード

1687158

欧州のスナックバー市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Snack Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のスナックバー市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 203 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

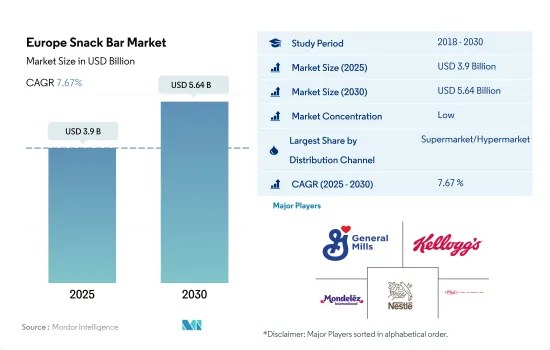

欧州のスナックバー市場規模は2025年に39億米ドルと推定・予測され、2030年には56億4,000万米ドルに達し、予測期間(2025~2030年)のCAGRは7.67%で成長すると予測されます。

スーパーマーケット/ハイパーマーケットとコンビニエンスストアは、この地域全体で強い存在感を示しているため、スナックバー販売の金額シェアは合計で80%以上です。

- スーパーマーケットとハイパーマーケットは欧州のスナックバー市場で最大のチャネルです。欧州のスナックバー市場全体の流通チャネルでは、金額ベースで56%のシェアを占めています。スナックバーカテゴリーの専用棚における戦略的な製品ポジショニングは、潜在的消費者の衝動購買行動に影響を与えます。Carrefour、Super U、Tesco、Asda、Lidlは、この地域の大手食料品店経営者の一部です。例えば、2023年3月現在、TescoとAsdaは英国で3,456店舗を展開しています。このチャネルの人気を支えている主要要因は、魅力的な割引キャンペーン、ロイヤリティプログラム・スキーム、キャッシュバック・スキームです。

- コンビニエンスストアは、スーパーマーケット、ハイパーマーケットに次いで、スナックバーの購入に広く選ばれている流通チャネルです。コンビニエンスストアは都市部や農村部の街角に存在するため、2024年にはコンビニエンスストアを通じたスナックバーの数量は33.22%のシェアを占めると推定されます。消費者は、自宅や職場の近くに食料品店があることを重要視しています。そのため、スナックバー製品の販売は、この地域全体でこのチャネルを通じて広く行われています。

- オンライン小売チャネルは、国内で最も急成長しているセグメントと考えられています。スナックバーの販売は、2023~2024年にかけて、こうしたチャネルを通じて7.20%の割合で成長すると予測されます。これは、消費者がインターネットでの購入を好み、特に菓子類のように、メーカー名、ブランドポジショニング、イメージ、包装・デザインといった点で馴染みのある商品を好むためです。

英国、ドイツ、フランスでスナックバー消費が急増、予測期間中の市場成長を牽引

- 英国とイタリアが同地域の主要市場であり、イタリア、ドイツ、その他の欧州がこれに続きます。英国とイタリアは、2023年の同地域全体のスナックバー販売額の53.03%のシェアを占めています。健康的で便利な嗜好性間食に対する消費者の嗜好が、この地域の主要な市場促進要因であることが確認されています。2021年には、フランスの消費者の33%が日中仕事中にシリアルバーを消費し、26%の消費者が身体活動の周辺でシリアルバーを消費しました。

- グラノーラ/シリアル/スナックバーの消費は、バーの消費者の間に浸透しています。2022年には、英国の消費者の半数以上(58%)、ドイツの消費者の44%、フランスの消費者の30%が、外出先でのスナックの1つとしてスナックバーを含む食間の間食をとっています。2021~2022年にかけて、英国の人口の約96%がグラノーラ/シリアル/スナックバーを少なくとも時折消費しています。グラノーラ/シリアル/スナックバーとキャンディーバーの消費は、以前と比較して同期間に25%増加しました。欧州のスナックバー消費は、2027年には42億7,767万米ドルの市場規模に達すると予測され、2024~2027年の間に20%の金額成長が見込まれています。

- プロテインバーは、この地域で最も急成長しているスナックバーのタイプであり、予測期間中のCAGRは7.8%と予想され、2030年には欧州の市場規模は16億米ドルに達します。2023年には、英国、ロシア、フランス、ドイツが、各国のスポーツジムでさまざまなフィットネス活動を利用できることから、合計金額シェア86%で主要なプロテイン消費国であり続けた。2021年には、ドイツ全土に535のクライミングジムがありました。2021~2022年にかけて、英国のプロテインバー消費者の3人に1人は「高タンパク質」が重要な属性であることに変わりはないです。

欧州スナックバー市場動向

健康的なライフスタイルの普及とスポーツ愛好家の増加が、欧州全域での売上増につながりました。

- 欧州では利便性の動向が拡大し続け、ますます忙しくなるライフスタイルの中で、消費者はいつでもどこでもシリアルバー、プロテインバー、ナッツバーなどのスナックバーを手に取るようになりました。2022年には、英国の消費者の58%がスナックバーを頻繁に消費すると回答しました。

- この地域では、プロテインバー、フルーツバー、ナッツバー、シリアルバーなど、さまざまな形態のスナックバーが販売されています。この地域の多くのメーカーは、消費者の嗜好を満たすために革新的なフレーバーのスナックバーを発売しています。

- 欧州のスナックバー売上は2022年に成長しました。同地域ではスナックバーの需要が伸びているため、主要企業がイノベーションで売上を伸ばしています。同地域ではドイツがプロテインバーの売上をリードしています。ドイツのプロテインバーのトップブランドには、Myprotein、Multipower、Champ、PowerBar、Power Systemなどがあります。

- この地域の消費者は、より健康的な選択肢として、シリアルバー、プロテインバー、フルーツ&ナッツバーなどのスナックバーを選ぶようになってきています。スナックバーの多くは、炭水化物、タンパク質、健康的な脂肪などの栄養素をバランスよく摂取できるように配合されています。

欧州のスナックバー産業概要

欧州のスナックバー市場は細分化されており、上位5社で37.41%を占めています。この市場の主要企業は、 General Mills Inc.、Kellogg Company、Mondelez International Inc.、Nestle SA、Post Holdings Inc.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 流通チャネル

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- スイス

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Abbott Laboratories

- Associated British Foods PLC

- August Storck KG

- Ferrero International SA

- General Mills Inc.

- Halo Foods Ltd

- Kellogg Company

- Lotus Bakeries

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- PepsiCo Inc.

- Post Holdings Inc.

- Simply Good Foods Co.

- The Hershey Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 55769

The Europe Snack Bar Market size is estimated at 3.9 billion USD in 2025, and is expected to reach 5.64 billion USD by 2030, growing at a CAGR of 7.67% during the forecast period (2025-2030).

Supermarkets/hypermarkets and convenience stores collectively hold more than 80% value share for sales of snack bars due to their strong presence across the region

- Supermarkets and hypermarkets are the largest channels in the European snack bar market. The channel held the major share of 56% by value in the overall distribution channels segment for the European snack bar market. Strategic product positioning on the dedicated shelves for the snack bar category influences impulse purchase behavior among potential consumers. Carrefour, Super U, Tesco, Asda, and Lidl are some of the leading grocery store operators in the region. For instance, as of March 2023, Tesco and Asda had 3,456 stores in the United Kingdom. The major factors behind the popularity of this channel were attractive discount offers, loyalty program schemes, and cashback schemes.

- Convenience stores are the second most widely preferred distribution channels after supermarkets and hypermarkets to purchase snack bars. The volume sales of snack bars through convenience stores is estimated to register a 33.22% volume share in 2024 due to their presence in the streets of urban and rural areas. Consumers consider it important for a grocery store to be located near their home or office. Thus, sales of snack bar products happen widely through the channel across the region.

- The online retail channel is considered the fastest-growing segment across the country. Snack bar sales are anticipated to grow through these channels at a rate of 7.20% from 2023 to 2024 due to consumer's preference for buying on the Internet, especially the goods they are familiar with, such as confectioneries, in terms of the manufacturer's name, brand positioning, image, and packaging design.

Snack bar consumption is soaring in the UK, Germany, and France, driving market growth during the forecast period

- The United Kingdom and Italy are identified as the major markets in the region, followed by Italy, Germany, and the Rest of Europe. The United Kingdom and Italy collectively accounted for 53.03% share of the overall snack bar sales value across the region in 2023. Consumer preference for healthy and convenient indulgent snacking is identified as the key market driver in the region. In 2021, 33% of French consumers consumed cereal bars at work during the day, while 26% of consumers consumed them around physical activity.

- The consumption of granola/cereal/snack bars is pervasive among bar consumers. In 2022, more than half (58%) of United Kingdom consumers, 44% of Germans, and 30% of France consumers snacked between meals, including snack bars as one of the on-the-go snacks. During 2021-2022, around 96% UK population consumed granola/cereal/snack bars at least occasionally. The consumption of granola/cereal/snack bars and candy bars had increased by 25% during the same period compared to former years. The snack bar consumption in Europe is anticipated to reach a market value of 4277.67 million in 2027, with a value growth of 20% during 2024-2027.

- Protein bars are the fastest-growing snack bar type in the region, with an anticipated CAGR of 7.8% during the forecast period, reaching a market value of USD 1.6 billion by 2030 in Europe. In 2023, the UK, Russia, France, and Germany remained the major protein-consuming countries with a combined value share of 86%, owing to the access to different fitness activities in gyms across the countries. In 2021, there were 535 climbing gyms across Germany. During 2021-2022, for one in three protein bar consumers in the United Kingdom "high protein" remained an important attribute among the bar consumers.

Europe Snack Bar Market Trends

The adoption of a healthy lifestyle, along with the increasing number of sports enthusiasts, resulted in higher sales across Europe

- The convenience trend continued to grow in Europe, and increasingly busy lifestyles meant consumers were grabbing a few snack bars such as cereal bars, protein bars, nut bars, and others whenever and wherever they could.; In 2022, 58% of consumers in the United Kingdom claimed that they frequently consume snack bars.

- Snack bars are available in different formats in the region, including protein bars, fruit and nut bars, and cereal bars. Many manufacturers in the region are launching snack bars with innovative flavors to meet consumer preferences.

- Snack bar sales in Europe witnessed growth in 2022. As the demand for snack bars grows in the region, major key players are increasing their sales with their innovations; Germany is the leading country in the sales of protein bars in the region. The top brands in German protein bars include Myprotein, Multipower, Champ, PowerBar, and Power System.

- Consumers in the region are increasingly turning to snack bars such as cereal bars, protein bars, and fruit and nut bars as a perceived healthier option. Many Snack bars are formulated to provide a balance of nutrients, including carbohydrates, protein, and healthy fats.

Europe Snack Bar Industry Overview

The Europe Snack Bar Market is fragmented, with the top five companies occupying 37.41%. The major players in this market are General Mills Inc., Kellogg Company, Mondelez International Inc., Nestle SA and Post Holdings Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Cereal Bar

- 5.1.2 Fruit & Nut Bar

- 5.1.3 Protein Bar

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Switzerland

- 5.3.9 Turkey

- 5.3.10 United Kingdom

- 5.3.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Abbott Laboratories

- 6.4.2 Associated British Foods PLC

- 6.4.3 August Storck KG

- 6.4.4 Ferrero International SA

- 6.4.5 General Mills Inc.

- 6.4.6 Halo Foods Ltd

- 6.4.7 Kellogg Company

- 6.4.8 Lotus Bakeries

- 6.4.9 Mars Incorporated

- 6.4.10 Mondelez International Inc.

- 6.4.11 Nestle SA

- 6.4.12 PepsiCo Inc.

- 6.4.13 Post Holdings Inc.

- 6.4.14 Simply Good Foods Co.

- 6.4.15 The Hershey Company

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms