北米のスナックバー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Snack Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684025

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

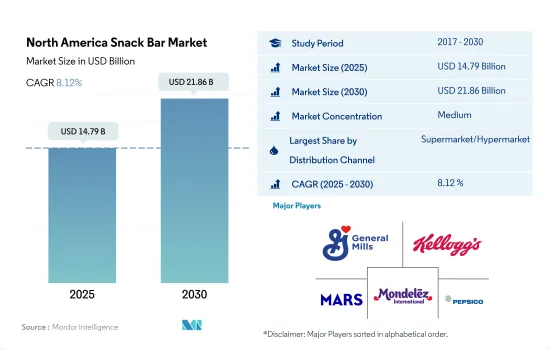

北米のスナックバー市場規模は2025年に147億9,000万米ドルと推定・予測され、2030年には218億6,000万米ドルに達し、予測期間(2025-2030年)のCAGRは8.12%で成長すると予測されます。

Walmart、Sprouts、Kroger、Meijerなどの大手小売チェーンがスナックバー専用の棚やキャビネットを設置しているため、スーパーマーケットとハイパーマーケットが大きなシェアを占めています。

- 北米の流通チャネルセグメント全体では、2022年に2021年比で8.01%の成長率を記録したが、これは主に、味や風味を犠牲にすることなく、小売チャネルを通じて健康志向でヘルシーなスナッキング・オプションの消費が増加しているためです。ウォルマート(Walmart)、スプラウト(Sprouts)、クローガー(Kroger)、メイジャー(Meijer)などの大手店舗は、健康志向の消費者の買い物体験を簡素化するため、スナックバー専用の棚やキャビネットを設けています。

- オンライン小売店は、予測期間中にCAGR 8.10%を記録し、最も急成長するセグメントとなりそうです。eコマース分野は、他のどの伝統的な小売チャネルよりも急速に成長しています。この成長は主に、スナックバーのような機能的で健康的な製品に対する需要の高まりによるもので、これらはオンライン小売店で広く入手可能です。この地域の大手小売業者が採用しているeコマース・アプローチも、スナックバー市場を牽引しています。コストコ(Costco)、トレーダージョーズ(Trader Joe's)、ウォルマート(Walmart)などの小売業者はオムニチャネル・ショッピングに力を入れており、特にオンライン機能を実店舗に拡大・統合しています。

- スーパーマーケットが金額ベースで大きなシェアを占めており、2026年の金額成長率は2025年比で5.6%に達する見込みです。これらの小売チャネルは、提供されるブランドの品揃えの豊富さ、棚面積の広さ、頻繁な価格プロモーションにより、強い地位を占めています。この地域の小売業界は広範でよく組織化されているため、顧客はスナックバーを含む様々な菓子製品を購入しやすく便利です。スーパーマーケットはまた、この地域の近接性により、市場で入手可能な幅広い商品の中で消費者の購買決定に影響を与えるという利点もあります。

米国が市場を独占しており、80%以上の消費者が栄養、プロテイン、万能スナックバーを定期的に消費しています。

- 北米地域の2023年のスナックバー販売額は前年比7.19%増。この成長は、多忙で慌ただしいライフスタイルの一環として、すぐに食べられる(RTE)、食事代替、パック食品に対する消費者の嗜好が高まっていることに起因しています。

- 米国はこの地域のスナックバー消費全体の大半を占めています。米国におけるスナックバーの販売額は、2022年と比較して2025年には21%成長すると予測されています。スナックバーの需要は、その健康上の利点と、様々なスナックバーカテゴリーで幅広いフレーバーが入手可能なことから、かなり伸びています。ビーガン(完全菜食主義者)傾向の高まりや、スナックバーにおけるオーガニック原料の使用により、消費者行動に変化が生じ、動物性原料に比べ植物性原料を使用した製品の採用率が高まっています。

- 2022年現在、米国では半数以上(51%)の消費者が通常の万能スナックバーを消費し、他のタイプのバー製品も好んでいます。同国の消費者の約36%がスナックまたは栄養プロテイン・バーを、成人の35%がファイバー・バーを、22%が栄養バーを消費しています。

- カナダは北米で2番目に成長している市場です。カナダにおけるスナックバーの販売額は、2022年から2023年にかけて6.6%成長しました。この成長は、クリーンラベル製品に対する需要の高まりと健康食品に対する意識の高まりに支えられています。カナダ人は、栄養豊富なグルテンフリー、シュガーフリー、その他多くの種類のスナックバーを消費するようになっています。

北米のスナックバー市場動向

消費者の健康志向の高まりに加え、様々なブランドのスナックバーが同地域全域で販売されるようになり、売上が増加

- 北米では、スナックバーは油菓子の代替品として社会人に好まれています。2023年には、米国人はスナックバーを持ち運びできる便利な製品として消費し、米国の消費者の75%が定期的にスナックバーを食べています。

- スナックバー・セグメントでは、ブランド・ロイヤルティが製品属性の第1位を占めています。北米では、43%の消費者が好みのブランドのスナックバーを選んでいることが確認されました。Crunch Plus、Nature Vallye、One、ProBar、MxBarなどが高い市場シェアを持つブランドです。

- 2023年には、スナックバーの売上が増加しました。売上の伸びは消費者の健康的な食習慣と関連しています。スナックバーは、その利点を強調し、油っこいスナックを健康的なスナックバーに置き換えることで販売が促進されました。2023年、スナックバー製品は2022年比で2.34米ドルの前年比成長を記録しました。

- 北米では、スナックバーの消費は一般的に健康の観点から見られています。様々なフレーバーのスナックバーが入手可能なため、若い世代に健康的なおやつとして楽しまれています。米国では、スナックバーの消費に関して、原材料の重要性など、健康の観点から考慮すべきいくつかの追加要因があります。

北米のスナックバー産業概要

北米のスナックバー市場は適度に統合されており、上位5社で41.92%を占めています。この市場の主要企業は以下の通りです。General Mills Inc., Kellogg Company, Mars Incorporated, Mondelez International Inc. and PepsiCo Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コンフェクショナリー種類

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 流通チャネル

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

- 国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 1440 Foods Company

- Abbott Laboratories

- Core Foods

- General Mills Inc.

- Go Macro LLC

- Jamieson Wellness Inc.

- Kellogg Company

- Mars Incorporated

- Mondelez International Inc.

- No Cow LLC

- PepsiCo Inc.

- Power Crunch Pty Ltd

- Probar Inc.

- Simply Good Foods Co.

- The Hershey Company

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Snack Bar Market size is estimated at 14.79 billion USD in 2025, and is expected to reach 21.86 billion USD by 2030, growing at a CAGR of 8.12% during the forecast period (2025-2030).

Supermarkets and hypermarkets hold the prominent share as major retail chains, including Walmart, Sprouts, Kroger, and Meijer, have dedicated shelves and cabinets for snack bars

- The overall North American distribution channel segment experienced a growth rate of 8.01% in 2022 compared to 2021, mainly because of the rising consumption of health-oriented and healthy snacking options through retail channels without sacrificing taste and flavor. Major stores like Walmart, Sprouts, Kroger, and Meijer are creating dedicated shelves and cabinets for snack bars to simplify the shopping experience of health-conscious consumers.

- Online retail stores are likely to be the fastest-growing segment by recording a CAGR of 8.10% during the forecast period. The e-commerce sector is growing faster than any other traditional retail channel. This increase is primarily due to the rising demand for functional and healthy products like snack bars, which are widely accessible at online retailers. The e-commerce approach adopted by major retailers across the region also drives the market for snack bars. Retailers such as Costco, Trader Joe's, and Walmart, among others, focus on omnichannel shopping, particularly expanding and integrating online capabilities into brick-and-mortar stores.

- Supermarkets accounted for a major share by value and are likely to attain a value growth rate of 5.6% during 2026 compared to 2025. These retail channels have a strong position due to the wide selection of brands offered, considerable shelf space, and frequent price promotions. The region's extensive and well-organized retail industry gives customers the accessibility and convenience to buy various confectionary products, including snack bars. The supermarket also has the advantage of influencing consumers' purchasing decisions within the wide range of products available in the market due to the proximity factor in the area.

The United States dominates the market, with over 80% of consumers regularly consuming nutrition, protein, and all-purpose snack bars

- The sales value of snack bars in the North American region increased by 7.19% in 2023 compared to the previous year. The growth is attributed to rising consumer preference toward ready-to-eat (RTE), meal replacement, and packed food items as a part of their busy and hectic lifestyles.

- The United States accounts for most of the region's overall snack bar consumption. The sales value of snack bars in the United States is anticipated to grow 21% in 2025 compared to 2022. The demand for snack bars is growing considerably due to their health benefits and the availability of a wide range of flavors within various snack bar categories. With the growing vegan trend and the use of organic ingredients in snack bars, there is a shift in consumer behavior, resulting in higher adoption of products made from plant sources compared to animal sources.

- As of 2022, in the United States, more than half (51%) of the consumers consumed regular, all-purpose snack bars and preferred other types of bar products as well. Around 36% of the consumers in the country consumed snack or nutrition protein bars, 35% of the adults consumed fiber bars, and 22% consumed nutrition bars.

- Canada is the second largest-growing market in North America. The sales value of snack bars in Canada grew 6.6% from 2022 to 2023. The growth is aided by the growing demand for clean-label products and the rising awareness of healthy food. Canadians increasingly consume snack bars containing nutrient-rich, gluten-free, sugar-free, and many other types of snack bars.

North America Snack Bar Market Trends

Rising health consciousness among consumers, along with the availability of various branded snack bars across the region, resulted in higher sales

- In North America, snack bars are highly preferred by working professionals as a replacement for oil-based snacks. In 2023, Americans consumed snack bars as a grab-and-go convenience product, and 75% of US consumers devoured snack bars on a regular basis.

- In the snack bars segment, brand loyalty acquires the first position under product attributes. In North America, it was observed that 43% of consumers are choosing snack bars of their preferred brands. Crunch Plus, Nature Vallye, One, ProBar, and MxBar are some brands holding higher market shares.

- In 2023, snack bars witnessed a hike in their sales. The sales growth was linked to the healthy eating habits of consumers. The sales of snack bars were promoted by highlighting their benefits and replacing oily snacks with healthy snack bars. In 2023, snack bar products recorded a Y-o-Y growth of USD 2.34 compared to 2022.

- In North America, the consumption of snack bars is generally viewed from a health perspective. With the availability of snack bars in different flavors, they are enjoyed as healthy treats by the young generation. In the United States, there are a few additional factors to consider from a health perspective in the context of snack bar consumption, including ingredient significance.

North America Snack Bar Industry Overview

The North America Snack Bar Market is moderately consolidated, with the top five companies occupying 41.92%. The major players in this market are General Mills Inc., Kellogg Company, Mars Incorporated, Mondelez International Inc. and PepsiCo Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Cereal Bar

- 5.1.2 Fruit & Nut Bar

- 5.1.3 Protein Bar

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 1440 Foods Company

- 6.4.2 Abbott Laboratories

- 6.4.3 Core Foods

- 6.4.4 General Mills Inc.

- 6.4.5 Go Macro LLC

- 6.4.6 Jamieson Wellness Inc.

- 6.4.7 Kellogg Company

- 6.4.8 Mars Incorporated

- 6.4.9 Mondelez International Inc.

- 6.4.10 No Cow LLC

- 6.4.11 PepsiCo Inc.

- 6.4.12 Power Crunch Pty Ltd

- 6.4.13 Probar Inc.

- 6.4.14 Simply Good Foods Co.

- 6.4.15 The Hershey Company

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日