|

市場調査レポート

商品コード

1687044

南米の飼料用酵素:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)South America Feed Enzymes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の飼料用酵素:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 205 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

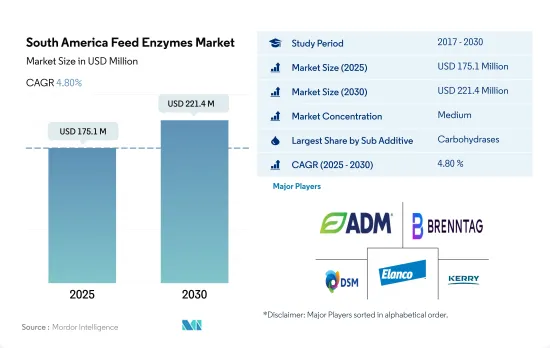

南米の飼料用酵素の市場規模は2025年に1億7,510万米ドルと推定され、2030年には2億2,140万米ドルに達すると予測され、予測期間中(2025-2030年)にCAGR 4.80%で成長する見込みです。

- 酵素は動物栄養学で使用される重要な飼料添加物の一種です。南米では、2022年の飼料添加物市場全体で酵素の市場シェアは3.8%でした。酵素は、動物体内のデンプン、タンパク質、脂肪の分解を含む多くの代謝反応において極めて重要です。

- 酵素の中でもカーボヒドラーゼは南米で最もよく消費されており、市場価値は7,070万米ドルです。カーボハイドラーゼは、エネルギーを増加させ、でんぷんを分解して動物にとって使用可能なエネルギー源となる分子を放出することにより、家畜の飼料コストを削減する上で重要です。また、動物飼料からのタンパク質、ミネラル、脂質の摂取量も増加させる。

- 飼料用炭水化物分解酵素の最大の動物種セグメントは家禽類で、2022年の市場シェア値の52.1%を占めました。これは、非デンプン性多糖類を多く含む穀類が家禽飼料に多く消費されることと関連しています。

- 一方、フィターゼは2022年に金額ベースで南米の飼料用酵素市場の33.6%を占め、飼料用酵素市場で2番目に大きなセグメントとなっています。動物性タンパク質に対する需要の高まり、動物人口の増加、酵素の利点が、飼料用酵素市場のプラス動向の原動力となっています。

- ブラジルは南米最大の飼料用酵素市場で、2022年の市場シェアの57.2%を占める。シェアが高いのは、同国で2017年から2022年にかけて家禽の頭数が9.1%増加したためです。このように、飼料用酵素市場は、動物栄養における飼料用酵素の重要性により、予測期間中にCAGR 4.8%で成長すると予想されます。

- 南米の飼料用酵素市場はブラジルが支配的であり、2017年から2022年にかけてブラジルの畜産人口全体が8.5%増加し、食肉および食肉製品の輸出が増加し、家畜生産が無秩序から組織化されたものに変化したことに起因して、2022年の市場価値は8,760万米ドルでした。ブラジルでは、家禽セグメントが飼料用酵素の最大消費者で、2022年には55.9%を占め、次いで養豚セグメントと反芻動物セグメントの市場シェアがそれぞれ21.6%と18.2%です。主な促進要因は、広大な草地と穀物生産に適した気候です。

- アルゼンチンは南米で2番目に大きな飼料用酵素市場です。予測期間中のCAGRは4.7%と予想されます。金額ベースでは、反芻動物部門が2022年のアルゼンチンの飼料用酵素市場の50.0%を占め、家禽部門は29.9%です。

- チリの市場は2017年から2022年にかけて32.3%成長したが、これは栄養吸収の向上など、動物飼料における酵素の健康上の利点に対する認識の高まりによる。2022年、チリの動物飼料で最も広く使用されている酵素は炭水化物分解酵素で、飼料用酵素市場全体の52.3%を占め、動物の種類別では豚の消費が最も多くなりました。

- その他南米は、2022年の南米の飼料用酵素市場全体の19.9%を占めました。家禽セグメントが2022年に66.9%の最大市場シェアを占め、次いで豚が14.1%でした。

- 全体として、飼料用酵素市場は、動物の栄養要求を補うための飼料における酵素の使用量の増加と食肉生産の急成長により、予測期間中に成長すると予想されます。

南米の飼料用酵素市場動向

高い投資収益率(ROI)と鶏肉製品の需要増加により養鶏が人気を博し、ブロイラーとレイヤーが養鶏生産の大半を占める

- 養鶏は南米では重要な産業であり、その養鶏部門は2017年と比較して2022年には10.1%という目覚ましい成長率を記録しています。この成長は、国内外で鶏肉とその製品の消費が増加していることに起因しています。2022年には、ブラジル国内だけで家禽肉の消費量は約1,030万トンとなり、2018年の960万トンから大幅に増加します。南米の多くの地域で鶏肉部門の成長と産業化が続いているため、この動向は今後も続くと思われます。

- ブロイラーとレイヤーの生産は、この地域の家禽部門に大きく貢献しており、2022年には家禽生産全体の約97.3%を占める。ブラジルは南米最大の鶏肉製品生産国で、2021年の鶏肉生産量は約1,460万トンです。同地域は世界的にも主要な鶏肉輸出国であり、ブラジルは同地域の鶏肉輸出の70%以上を輸出しています。2021年、ブラジルは鶏肉生産量の約3分の1を150カ国以上に輸出し、中国がこの地域の最大の輸出先となっています。

- 養鶏は高収量で投資回収が早いため、この地域、特にブラジルで重要性を増しています。その結果、南米、特にブラジルの養鶏産業は、国内外での鶏肉とその製品に対する需要の増加により、着実な成長を遂げています。工業化とそれがもたらす利益への注目が高まる中、この地域の養鶏セクターは今後数年間、継続的に成長する態勢を整えています。

淡水養殖が養殖生産の90%を占め、養殖産業の拡大が養殖飼料生産の増加に寄与しています。

- 南米における養殖飼料生産量は2017年以降急速に増加しており、2022年には57.5%増の約500万トンの水産種用配合飼料が生産されます。ブラジルとチリが養殖用飼料生産の成長に大きく貢献しており、両国は2022年にそれぞれ140万トンと120万トンを占める。この成長は主にこれらの国々における養殖種の淡水養殖の増加に起因しており、2020年以降、ブラジルでは平均して養殖生産量の90%を淡水養殖が占めることになります。

- 南米における魚用飼料生産は増加傾向にあり、2022年には養殖用飼料生産全体の80.4%を占める。この魚用飼料生産の増加は、ブラジルやチリのような国々で魚の養殖が増加していることに起因しており、2017年と比較して生産量は56%増加しています。この地域における漁業・養殖セクターの拡大の可能性は莫大であるため、この動向は今後数年間も続くと予想されます。

- ティラピアの養殖は同地域の水産養殖産業の拡大に大きく寄与しており、これが配合飼料の需要増につながっています。エビ飼料の生産量も、利益率の高いホワイトレッグ種のエビ需要の高まりにより、2019年と比較して2022年には51.4%増と大幅に増加しています。この動向は、エビの生産量と輸出需要の増加に牽引され、今後数年間も続くと予想されます。結論として、南米における水産養殖飼料生産は、漁業・水産養殖セクターの拡大、高品質タンパク質に対する需要の高まり、輸出需要の増加に牽引され、今後数年間増加し続けると予測されます。

南米の飼料用酵素産業の概要

南米の飼料用酵素市場は適度に統合されており、上位5社で46.25%を占めています。この市場の主要企業は以下の通りです。 Archer Daniel Midland Co., Brenntag SE, DSM Nutritional Products AG, Elanco Animal Health Inc. and Kerry Group Plc(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- サブ動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- サブ動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 生産国

- アルゼンチン

- ブラジル

- チリ

- その他南米

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Adisseo

- Archer Daniel Midland Co.

- Brenntag SE

- Cargill Inc.

- DSM Nutritional Products AG

- Elanco Animal Health Inc.

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Kerry Group Plc

- Novus International, Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The South America Feed Enzymes Market size is estimated at 175.1 million USD in 2025, and is expected to reach 221.4 million USD by 2030, growing at a CAGR of 4.80% during the forecast period (2025-2030).

- Enzymes are an important type of feed additive used in animal nutrition. In South America, enzymes held a market share of 3.8% in the total feed additives market in 2022. Enzymes are crucial in many metabolic reactions, including the breakdown of starch, protein, and fat in the animal body.

- Among enzymes, carbohydrases are the most commonly consumed in South America, with a market value of USD 70.7 million. Carbohydrases are important in reducing animal feed costs by increasing energy and degrading starch, which releases molecules that form a usable source of energy for the animal. They also enhance the intake of protein, minerals, and lipids from animal feed.

- Poultry birds were the largest animal type segment for feed carbohydrases, accounting for 52.1% of the market share value in 2022. This is associated with the higher consumption of cereal with high non-starch polysaccharide content in poultry feed.

- Phytases, on the other hand, accounted for 33.6% of the South American feed enzymes market in terms of value in 2022, making it the second-largest segment in the feed enzymes market. The rising demand for animal protein, the increasing animal population, and the benefits of enzymes are the driving factors in the positive trend of the feed enzymes market.

- Brazil is the largest market for feed enzymes in South America, accounting for 57.2% of the market share in 2022. The higher share is due to the increased headcount of poultry by 9.1% in the country between 2017 and 2022. Thus, the market for feed enzymes is expected to grow during the forecast period with a CAGR of 4.8%, owing to the importance of feed enzymes in animal nutrition.

- The South American feed enzymes market is dominated by Brazil, which held a market value of USD 87.6 million in 2022, attributed to an 8.5% increase in Brazil's overall livestock population from 2017 to 2022, coupled with rising meat and meat product exports and a transformation from disorganized to organized livestock production. In Brazil, the poultry segment is the largest consumer of feed enzymes, accounting for 55.9% in 2022, followed by swine and ruminant segments, with market shares of 21.6% and 18.2%, respectively. The major driving factors are large grassland areas and a favorable climate for grain production.

- Argentina has the second-largest feed enzymes market in South America. It is anticipated to record a CAGR of 4.7% during the forecast period. In terms of value, the ruminant sector accounted for 50.0% of the Argentinian feed enzymes market in 2022, while the poultry segment accounted for 29.9%.

- Chile's market grew by 32.3% from 2017 to 2022, driven by the growing awareness of the health benefits of enzymes in animal feed, such as better nutrient absorption. In 2022, carbohydrases were the most widely used enzymes in animal feed in Chile, accounting for 52.3% of the overall feed enzymes market value, with swine having the most consumption by animal type.

- The Rest of South America accounted for 19.9% of South America's total feed enzymes market in 2022. The poultry segment held the largest market share of 66.9% in 2022, followed by swine at 14.1%.

- Overall, the market for feed enzymes is expected to grow during the forecast period due to the increasing usage of enzymes in the feed to supplement animals' nutritional requirements and the rapid growth of meat production.

South America Feed Enzymes Market Trends

Broilers and layers dominate the poultry production as the poultry farming gained popularity due to high Return on Investment (ROI) and increased demand for poultry products

- Poultry farming is a vital industry in South America, with its poultry sector experiencing an impressive growth rate of 10.1% in 2022, compared to 2017. This growth can be attributed to the increased consumption of poultry meat and its products, both domestically and internationally. In 2022, the consumption of poultry meat in Brazil alone was around 10.3 million metric tons, a significant increase from 9.6 million metric tons in 2018. This trend is set to continue as the poultry sector continues to grow and industrialize across many parts of South America.

- The production of broilers and layers is a major contributor to the region's poultry segment, accounting for around 97.3% of the total poultry production in 2022. Brazil is the largest producer of poultry products in South America, which produced around 14.6 million metric tons of chicken meat in 2021. The region is also a major poultry exporter globally, with Brazil exporting over 70% of the region's poultry meat exports. In 2021, Brazil exported about one-third of its chicken production to over 150 countries, with China being the largest destination export hub for the region.

- Poultry farming is gaining importance in the region, particularly in Brazil, due to its high yield and quick return on investment. As a result, the poultry farming industry in South America, particularly in Brazil, is experiencing steady growth due to increasing demand for poultry meat and its products, both domestically and internationally. With an increasing focus on industrialization and the benefits it offers, the poultry farming sector in the region is poised for continued growth in the coming years.

Freshwater cultivation account for 90% of aqua production and expansion of aquaculture industry is contributing to increasing aqua feed production

- The aquaculture feed production in South America has been rapidly increasing since 2017, with a 57.5% rise in 2022, producing about 5 million metric tons of compound feed for aquatic species. Brazil and Chile have been the major contributors to the growth in feed production for aquaculture, with both countries accounting for 1.4 and 1.2 million metric tons, respectively, in 2022. This growth is primarily attributed to the rise in freshwater cultivation of aquaculture species in these countries, with freshwater cultivation accounting for 90% of the aquaculture production in Brazil on average after 2020.

- Fish feed production in South America has been on the rise and accounted for 80.4% of the total aquaculture feed production in 2022. This increase in fish feed production can be attributed to the rising fish farming in countries, like Brazil and Chile, with a 56% increase in production compared to 2017. This trend is expected to continue in the next few years as the potential for the expansion of the fisheries and aquaculture sector in the region is enormous.

- Tilapia farming is one of the major contributors to the expansion of the aquaculture industry in the region, and this has led to increased demand for compound feed. Shrimp feed production has also witnessed a significant increase of 51.4% in 2022 compared to 2019, driven by the rising demand for high-profit-margin white-leg shrimp species. This trend is expected to continue in the next few years, driven by increasing shrimp production and export demand. In conclusion, the aquaculture feed production in South America is projected to continue to increase in the next few years, driven by the expansion of the fisheries and aquaculture sector, rising demand for high-quality protein, and increasing export demand.

South America Feed Enzymes Industry Overview

The South America Feed Enzymes Market is moderately consolidated, with the top five companies occupying 46.25%. The major players in this market are Archer Daniel Midland Co., Brenntag SE, DSM Nutritional Products AG, Elanco Animal Health Inc. and Kerry Group Plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Carbohydrases

- 5.1.2 Phytases

- 5.1.3 Other Enzymes

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Archer Daniel Midland Co.

- 6.4.3 Brenntag SE

- 6.4.4 Cargill Inc.

- 6.4.5 DSM Nutritional Products AG

- 6.4.6 Elanco Animal Health Inc.

- 6.4.7 IFF(Danisco Animal Nutrition)

- 6.4.8 Kemin Industries

- 6.4.9 Kerry Group Plc

- 6.4.10 Novus International, Inc.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms