|

市場調査レポート

商品コード

1693741

中国の飼料用酵素市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Feed Enzymes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の飼料用酵素市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 183 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

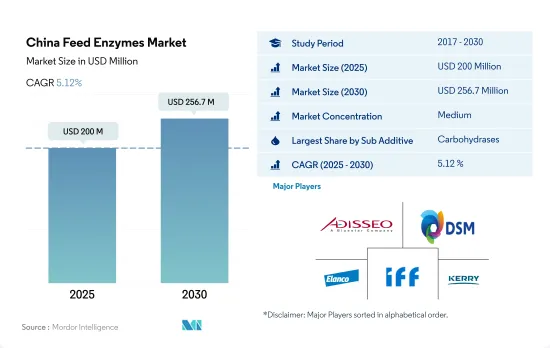

中国の飼料用酵素市場規模は2025年に2億米ドルと推定され、2030年には2億5,670万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.12%で成長すると予測されます。

- アジア太平洋の飼料用酵素市場は、中国が2022年の市場シェア43.6%を占め、1億7,200万米ドルとなりました。COVID-19の影響により、同国では配合飼料の生産が減少し、2020年の酵素市場の減少につながっていました。

- すべての飼料用酵素の中で、カルボヒドラーゼが市場規模に関して最大で、2022年の中国の飼料用酵素市場全体の46%を占めます。これは、カーボハイドラーゼが胃の中で作用して、繊維、デンプン、非デンプン多糖類などの炭水化物を、動物が使用するエネルギーとなる単糖に分解・分解し、効果的な消化をもたらすためです。

- 飼料用炭水化物分解酵素の最大の消費者は家禽類で、2022年の市場シェアは49.6%、次いで養豚(35%)、水産養殖(10.5%)となっています。カーボハイドラーゼに加えて、フィターゼも中国で需要が伸びており、予測期間(2023~2029年)のCAGRは5.1%と予測されます。

- フィターゼは、フィチン酸の抗栄養効果を低減し、単胃動物タイプのリンの消化率を改善するのに役立ちます。リンの吸収を促進し、動物体内のデンプン、タンパク質、アミノ酸の利用可能性を高めることで、糞便中に生成されるリンのレベルを低下させています。

- すべての動物タイプは、カーボハイドラーゼやフィターゼのような、天然では合成できない1つ以上の飼料酵素を必要とするため、これらは動物飼料を通じて供給されるべきです。そのため、中国の飼料用酵素市場は予測期間(2023~2029年)にCAGR 5%で拡大すると予測されています。

中国の飼料用酵素市場の動向

家禽製品の一人当たり消費量の増加と、豚に影響を与えたアフリカ豚熱(ASF)が家禽需要と家禽生産の増加に貢献

- 中国の家禽産業は世界市場で支配的な地位を占めており、主要な家禽生産者は北京、天津、上海、山東、広東に位置しています。このセクタの成長の主要因は、人口の増加と都市化、所得水準の向上、豚肉の供給を減少させたアフリカ豚熱の発生による鶏肉への消費者の嗜好の変化です。2017~2022年にかけて、中国の1人当たり鶏肉消費量は2.06kg増加し、鶏肉製品の需要をさらに押し上げました。

- 同国の養鶏産業は鶏、アヒル、ウズラを生産しており、鶏は主要な家禽鳥で、2022年には4億9,590万頭、世界の鶏卵生産の40%を占めます。レイヤー飼育の導入が進んだことで、国内最大のレイヤー飼育センターでは年間9億羽を超える採卵鶏と6,000万羽のヒナが孵化するようになりました。中国における鶏肉消費は、有利な価格、高タンパク食への意識の高まり、消費者の嗜好の変化により増加しました。その結果、鶏肉需要を満たすためにブロイラーの飼育率が高まっています。生産性を向上させ、鶏肉製品の需要増に対応するため、2021年には、Shengze 901、Guangming No.2、Wode 188の3種類の国産ブロイラー遺伝品種が発表されました。

- 市場での継続的な投資、商業化、新品種や改良品種のリリースは、家禽の生産量の増加と一人当たりの消費量の増加と相まって、予測期間中、中国の家禽産業の成長を促進すると予想されます。その他の特典として、鶏肉の健康上の利点と栄養価に対する意識の高まりが、同国における鶏肉産業の成長を促進すると予想されます。

水産物の需要増加と生産者の従来型飼料から配合飼料への移行が養殖種用飼料生産を増加させている

- 中国における養殖用飼料生産量は、2017年と比較して2022年には54.1%の大幅増となり、2,280万トンに達しました。しかし、COVID-19の大流行とそれに伴う飼料産業の閉鎖により、2020年には前年比21.3%減となりました。同国における水産物需要の増加と飼料生産部門の拡大が、中国における養殖生産の拡大を後押ししています。例えば、Grobest Chinaは広東省雷州に新しい養殖飼料工場を設立し、3,770万米ドルを投資し、年間生産能力は25万トンです。

- 中国では魚が主要な養殖種であり、魚の養殖量が2018年の3,740万トンから2022年には3,750万トンに増加するため、飼料需要が増加し、飼料生産量は前年から3.2%増加しました。生産者は、栄養管理と優良養殖プラクティスに関する意識の高まりにより、従来の飼料から配合飼料にシフトしています。

- 2022年には、エビの生産量が60万トンとなり、同国の水産飼料市場シェアの2.9%を占めました。中国におけるエビ飼料の需要は、中国の消費者が栄養転換期を迎えていることから、エビの需要が増加していることが強く影響しています。エビは抗酸化物質とアスタキサンチンの優れた供給源であり、神経系と筋骨格系を強化します。水産養殖セクタの急速な拡大と、水産養殖生産における栄養管理に対する意識の高まりが、予測期間中の市場成長を後押しすると予想されます。

中国の飼料用酵素産業概要

中国の飼料用酵素市場は適度に統合されており、上位5社で60.79%を占めています。この市場の主要企業は、Adisseo、DSM Nutritional Products AG、Elanco Animal Health Inc.、IFF(Danisco Animal Nutrition)and Kerry Group PLCなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adisseo

- Archer Daniel Midland Co.

- BASF SE

- DSM Nutritional Products AG

- Elanco Animal Health Inc.

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Kerry Group PLC

- Novus International, Inc.

- Olmix Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93775

The China Feed Enzymes Market size is estimated at 200 million USD in 2025, and is expected to reach 256.7 million USD by 2030, growing at a CAGR of 5.12% during the forecast period (2025-2030).

- China dominated the feed enzymes market in the Asia-Pacific region with a market share of 43.6% in 2022, valued at USD 172 million. Due to the impact of COVID-19, the production of compound feed in the country had declined, leading to a decrease in the market for enzymes in 2020.

- Of all feed enzymes, carbohydrases were the largest concerning market value, representing 46% of the total feed enzymes market in China in 2022. This is because carbohydrases act in the stomach to break down and degrade carbohydrates such as fiber, starch, and non-starch polysaccharides into simple sugars that provide energy for use by the animal and lead to effective digestion.

- Poultry birds are the largest consumers of feed carbohydrases, with a market share of 49.6% in 2022, followed by swine (35%) and aquaculture (10.5%). In addition to carbohydrases, phytases are also growing in demand in China, with a projected CAGR of 5.1% during the forecast period (2023-2029).

- Phytases aid in reducing the antinutritional effect of phytate and improving the digestibility of phosphorus in monogastric species. They lower the level of phosphorus produced in feces by enhancing phosphorus absorption and increasing the availability of starch, protein, and amino acids in the animal body.

- As all animal species require one or more feed enzymes that cannot be synthesized naturally, such as carbohydrases and phytases, these should be provided through animal feed. It is therefore anticipated that the feed enzymes market in China will expand at a CAGR of 5% during the forecast period (2023-2029).

China Feed Enzymes Market Trends

Increasing per capita consumption of poultry products and African Swine Fever (ASF) affecting swine helped in increasing the poultry demand and poultry production

- China's poultry industry holds a dominant position in the global market, with the major producers of poultry located in Beijing, Tianjin, Shanghai, Shandong, and Guangdong. The sector's growth is primarily attributed to rising population and urbanization, increased income levels, and shifting consumer preferences toward poultry meat, as a result of the African Swine Fever outbreak that reduced the pork meat supply. From 2017 to 2022, China's per capita consumption of poultry increased by 2.06 kg, further driving the demand for poultry products.

- The country's poultry industry produces chickens, ducks, and quails, with chickens being the major poultry bird, accounting for 495.9 million heads and 40% of global egg production in 2022. The increasing adoption of layer farming led to over 900 million stock-laying hens and 60 million chicks hatching annually at the country's largest layer farming center. Poultry meat consumption in China increased due to favorable prices, increasing awareness of high-protein diets, and a shift in consumer preferences. As a result, broilers are raised at a higher rate to meet the demand for poultry meat. To improve productivity and meet the growing demand for poultry products, three domestic varieties of broiler genetics were released in 2021, including Shengze 901, Guangming No. 2, and Wode 188.

- The continued investment, commercialization, and release of new and improved breeds in the market, coupled with rising production of poultry and increasing per capita consumption, are expected to drive the growth of the poultry industry in China during the forecast period. Additionally, the increasing awareness of health benefits and the nutritional value of poultry meat is anticipated to fuel the growth of the poultry industry in the country.

Rising demand for seafood and shifting of producers from conventional feed to compound feed is increasing the feed production for aquaculture species

- The aquaculture feed production in China witnessed a significant increase of 54.1% in 2022, reaching 22.8 million metric tons, compared to 2017. However, there was a 21.3% drop in 2020 from the previous year due to the COVID-19 pandemic and the resulting closure of feed industries. The increasing seafood demand in the country and expansions of the feed production units drive the expansion of aquaculture production in China. For instance, Grobest China established a new aquaculture feed factory in Guangdong Leizhou with an investment of USD 37.7 million and an annual production capacity of 250,000 tons.

- Fish is the primary aquaculture species in China, and feed production increased by 3.2% in 2022 from the previous year due to increased demand for feed as the cultivation of fish increased to 37.5 million metric tons in 2022 from 37.4 million metric tons in 2018. Producers are shifting from conventional feed to compound feed due to the increasing awareness regarding nutrient management and good farming practices.

- In 2022, shrimp accounted for 2.9% of the aquafeed market share in the country, with a production of 0.6 million metric tons. The demand for shrimp feed in China is strongly driven by the increasing demand for shrimps, as Chinese consumers undergo a nutrition transition. Shrimps are a good source of antioxidants and astaxanthin, which bolsters the nervous and musculoskeletal systems. The rapid expansion of the aquaculture sector and increasing awareness about nutrient management in aquaculture production are expected to boost market growth during the forecast period.

China Feed Enzymes Industry Overview

The China Feed Enzymes Market is moderately consolidated, with the top five companies occupying 60.79%. The major players in this market are Adisseo, DSM Nutritional Products AG, Elanco Animal Health Inc., IFF(Danisco Animal Nutrition) and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Carbohydrases

- 5.1.2 Phytases

- 5.1.3 Other Enzymes

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Archer Daniel Midland Co.

- 6.4.3 BASF SE

- 6.4.4 DSM Nutritional Products AG

- 6.4.5 Elanco Animal Health Inc.

- 6.4.6 IFF(Danisco Animal Nutrition)

- 6.4.7 Kemin Industries

- 6.4.8 Kerry Group PLC

- 6.4.9 Novus International, Inc.

- 6.4.10 Olmix Group

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms