|

市場調査レポート

商品コード

1686242

中東の飼料用酵素:市場シェア分析、産業動向、成長予測(2025年~2030年)Middle East Feed Enzymes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の飼料用酵素:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 203 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

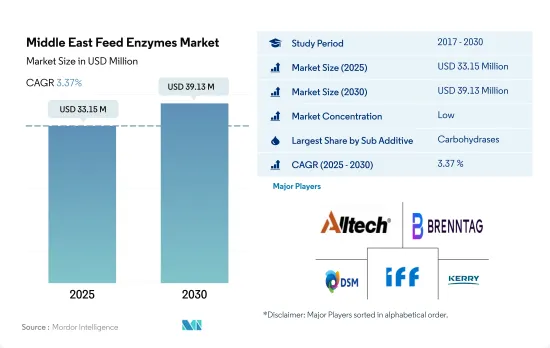

中東の飼料用酵素市場規模は2025年に3,315万米ドルと推定され、2030年には3,913万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは3.37%で成長する見込みです。

- 中東の飼料用酵素市場は、飼料添加物市場全体の中では小さいが成長しているセグメントです。2022年には、飼料添加物市場の3.6%を占めるに過ぎませんでした。しかし、特に穀物価格が高騰している場合に、飼料用酵素を使用して動物の栄養利用率を高める利点があるため、有望な市場となっています。

- 同市場は、飼料添加物の使用に直接関係する飼料生産の減少により、2019年には2018年比で6.2%の減少を経験しました。サウジアラビアは飼料生産量が多く、肉や乳製品の需要が高いことから、2022年には40.2%のシェアを占め、飼料用酵素市場で最大の国となりました。

- すべての飼料用酵素の中で、カルボヒドラーゼが市場金額で最も大きく、2022年の飼料用酵素市場の47.9%を占めました。カーボハイドラーゼが好まれるのは、動物飼料からのタンパク質、ミネラル、脂質の摂取量を増やす能力があるからです。この地域で最大の動物種セグメントは家禽類で、2022年の飼料用炭水化物分解酵素市場の57.9%を占める。この用途は、非水溶性多糖類の消化に関連しています。

- 予測期間中に中東で最も急成長する国はイランで、CAGR 3.7%を記録すると予想されます。フィターゼは同地域で最も急成長している分野であり、予測期間中のCAGRは3.4%と予想されます。

- 飼料添加物の使用に対する意識の高まりと食肉・家畜の需要が、この地域における飼料用酵素市場の主な促進要因になると予想されます。

- 2022年の中東の飼料添加物市場における飼料用酵素の金額シェアは3.6%で、前年から2.8%以上増加しました。しかし、市場は2019年から2020年にかけて若干の落ち込みを見せたが、これは主にCOVID-19パンデミックの影響によるもので、このパンデミックは世界の貿易と現地のサプライチェーンを混乱させ、飼料生産の減少をもたらしました。

- サウジアラビアは2022年に中東の飼料用酵素市場で最大のシェアを占め、金額ベースで約1,210万米ドルを占め、次いでイランが800万米ドルでした。サウジアラビアでは動物飼料への飼料添加物の採用率が高いため、同地域の他国と比較して消費量が最も多いです。

- 2022年の中東地域における飼料用酵素の最大の消費者は家禽類で、金額ベースで57.5%のシェアを占め、次いで反芻動物が39.7%、水産養殖が2.2%のシェアを占めています。酵素市場の成長を牽引するのは、この地域の畜産技術であり、食肉の輸入を制限し、水不足の国々が食肉産業から利益を得ることを目的としています。

- 2022年、中東地域の全動物種向け配合飼料の生産量は約2,400万トンに達し、イランだけでシェアの45%以上を占めました。この高い生産量は、2021年に中東地域の反芻家畜の18%以上を占めるなど、同国の動物人口が多いことに起因します。

- 飼料用酵素の使用需要は、食肉需要の増加と動物飼料における健康的な食生活への意識の高まりとともに増加しています。中東地域は、2023年から2029年にかけてCAGR 3.4%を記録し、市場の力強い成長が見込まれています。

中東の飼料用酵素市場の動向

中東地域では、家禽の一人当たり消費量の増加とともに新たな農場が設立され、家禽セクターが拡大しており、家禽生産の需要が増加しています。

- 中東では、養鶏業は農業セクターの中で最大のセグメントです。2022年には同地域の家畜頭数の90%を占めています。この部門は著しい成長を遂げ、2022年の生産量は2017年比で10.9%増加しました。同地域における肉・卵製品の需要増加が成長の主な要因となっています。観光、ビジネス旅行、ホテル・レストラン・施設(HRI)部門は、2022年の鶏肉生産量の前年比2.5%増に寄与しました。この生産量の増加により、家禽生産に使用される飼料添加物の価値は2.9%上昇しました。

- 中東諸国は、拡大する需要に対応するため、養鶏部門に投資して生産量を増やしています。例えば、サウジアラビアのAlmarai社は、11億2,000万米ドルを投資して工場と新しい農場を設立し、鶏肉生産を増加させようとしています。2022年、サウジアラビアの環境・水・農業省は275件の家禽プロジェクトライセンスを発行し、そのうち119件がブロイラープロジェクト、26件が年間20億個以上の卵生産能力、12件がブロイラー母鶏の繁殖・生産と年間4億8,050万羽の雛の生産能力を持つ孵化場の運営となっています。

- 同地域の鶏肉製品の1人当たり消費量は2017年の44.9kgから2022年には45.5kgに増加し、増産需要の原動力となっています。鶏肉産業への投資の増加や鶏肉製品の需要拡大といった要因は、予測期間中も鶏肉生産を後押しすると予想されます。

サウジアラビア、オマーン、アラブ首長国連邦などの政府は、大規模な養殖場を設立するために投資しており、この地域における水産飼料の需要を増加させると思われます。

- 中東の養殖産業は近年著しい成長を遂げており、養殖飼料の需要増につながっています。養殖用飼料の需要は2017年から2022年の間に25.1%増加しました。この成長は、同地域の養殖産業が拡大し、養殖種の生産が増加したためです。2022年には、養殖用飼料の生産量はこの地域の飼料生産量全体の2.1%を占め、合計50万トンとなります。イランはこの地域で最大の養殖飼料生産国で、2022年の生産量は28万トンです。この高い生産量は、同国の強力な養殖生産によるもので、さまざまな種類の養殖種の栽培に利用可能な淡水資源の恩恵を受けています。

- 魚類はこの地域で生産される最大の養殖種であり、養殖飼料生産の78.6%を占めています。サウジアラビア、オマーン、アラブ首長国連邦などの国々は、養殖に投資し、国際的な専門家や組織と提携して、生産性の高い地元養殖場を設立しています。湾岸地域の水産養殖組織は、英国湾岸海洋環境パートナーシップ(GMEP)プログラムを通じて、英国政府の環境漁業・水産養殖科学センター(Cefas)と協力し、魚類養殖の改善と生物多様性の損失に取り組んでいます。

- オマーンとアラブ首長国連邦は、この地域で養殖魚種の一人当たり消費量が最も多く、年間消費量は一人当たり28.6kgに達します。輸出を減らして国内生産を増やすため、オマーン政府は漁業・養殖業を補助金部門から同国経済に大きく貢献する部門に転換することを目指しています。

中東の飼料用酵素産業の概観

中東の飼料用酵素市場は細分化されており、上位5社で25.79%を占めています。この市場の主要企業は以下の通りです。 Alltech, Inc., Brenntag SE, DSM Nutritional Products AG, IFF(Danisco Animal Nutrition)and Kerry Group Plc(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- イラン

- サウジアラビア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 動物

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 国名

- イラン

- サウジアラビア

- その他の中東

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Adisseo

- Alltech, Inc.

- BASF SE

- Brenntag SE

- Cargill Inc.

- DSM Nutritional Products AG

- Elanco Animal Health Inc.

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Kerry Group Plc

- Novus International, Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Middle East Feed Enzymes Market size is estimated at 33.15 million USD in 2025, and is expected to reach 39.13 million USD by 2030, growing at a CAGR of 3.37% during the forecast period (2025-2030).

- The feed enzymes market in the Middle East is a small but growing segment of the overall feed additives market. In 2022, it accounted for only 3.6% of the feed additives market. However, the advantages of using feed enzymes to increase nutrient availability for animals, especially when cereal prices are high, make it a promising market.

- The market experienced a decline of 6.2% in 2019 compared to 2018 due to a decrease in feed production, which was directly related to the usage of feed additives. Saudi Arabia was the largest country in the feed enzymes market, accounting for a 40.2% share in 2022, owing to the country's higher feed production and demand for meat and dairy products.

- Among all the feed enzymes, carbohydrases were the most significant in terms of market value, accounting for 47.9% of the feed enzymes market in 2022. Carbohydrases are preferred because of their ability to increase the intake of protein, minerals, and lipids from animal feed. The largest animal type segment in the region was poultry birds, accounting for 57.9% of the feed carbohydrases market in 2022. The usage was associated with their digestion of non-soluble polysaccharides.

- The fastest-growing country in the Middle East during the forecast period is expected to be Iran, registering a CAGR of 3.7%. Phytases are expected to be the fastest-growing segment in the region, registering a CAGR of 3.4% during the forecast period.

- The increase in the awareness of the usage of feed additives and the demand for meat and livestock are expected to be the major drivers of the feed enzymes market in the region.

- In 2022, feed enzymes held a 3.6% share by value in the Middle Eastern feed additives market, representing an increase of over 2.8% from the previous year. However, the market witnessed a slight dip in 2019-2020, mainly due to the impact of the COVID-19 pandemic, which disrupted global trade and local supply chains, resulting in reduced feed production.

- Saudi Arabia held the largest share of the Middle Eastern feed enzymes market in 2022, accounting for around USD 12.1 million by value in the market, followed by Iran with USD 8.0 million. The high adoption of feed additives in animal diets in Saudi Arabia resulted in the highest consumption in the country compared to others in the region.

- Poultry birds were the largest consumers of feed enzymes in the Middle Eastern region in 2022, accounting for a 57.5% share by value in the market, followed by ruminants and aquaculture with 39.7% and 2.2% shares, respectively. The growth of the enzymes market is driven by the region's livestock-rearing technologies, which aim to limit meat imports and encourage water-scarce countries to benefit from their meat industries.

- In 2022, the Middle Eastern region produced around 24 million metric tons of compound feed for all animal types, with Iran alone accounting for more than 45% of the share. This high production was attributed to the country's large animal population, including more than 18% of ruminant cattle in the Middle Eastern region in 2021.

- The demand for feed enzyme usage has increased with the rising demand for meat and growing awareness of healthy diets in animal feeds. The Middle Eastern region is expected to witness strong growth in the market, recording a CAGR of 3.4% during 2023-2029.

Middle East Feed Enzymes Market Trends

Expanding poultry sector in the Middle East region with establishment of new farms with increasing per capita consumption of poultry has been increasing the demand for poultry production

- In the Middle East, the poultry industry is the largest segment in the agriculture sector. It accounted for 90% of the animal headcount in the region in 2022. The sector experienced significant growth, with production increasing by 10.9% in 2022 compared to 2017. The rise in demand for meat and egg products in the region has been the primary driver of the growth. The tourism, business travel, and the hotels, restaurants, and institutional (HRI) sectors contributed to a 2.5% increase in poultry production in 2022 compared to the previous year. This increased production led to a 2.9% rise in the value of feed additives used in poultry production.

- Middle Eastern countries are investing in their poultry sectors to boost production to meet the growing demand. For example, Saudi Arabia's Almarai company is investing USD 1.12 billion to establish a factory and new farms to increase poultry production. In 2022, the Saudi Arabian Ministry of Environment, Water, and Agriculture issued 275 poultry project licenses, including 119 for broiler projects, 26 for egg production with a capacity of more than two billion eggs per year, and 12 for breeding and producing broiler mothers and operating hatcheries with a capacity of 480.5 million chicks per year.

- The per capita consumption of poultry products in the region increased from 44.9 kg in 2017 to 45.5 kg in 2022, driving the demand for increased production. Factors such as increasing investments in the poultry industry and growing demand for poultry products are expected to continue to boost poultry production during the forecast period.

Government in the countries such as Saudi Arabia, Oman and the United Arab Emirates invested to establish large fish farms which will increase the demand for aqua feed in the region

- The aquaculture industry in the Middle East has experienced significant growth in recent years, leading to a rise in demand for aquaculture feed. Demand for aquaculture feed increased by 25.1% between 2017 and 2022. This growth was due to the expansion of the aquaculture industry in the region, which led to increased production of aquaculture species. In 2022, aquaculture feed production accounted for 2.1% of total feed production in the region, totaling 0.5 million metric tons. Iran is the largest producer of aquaculture feed in the region, with a production of 0.28 million metric tons in 2022. This high production could be attributed to the country's strong aquaculture production, which benefits from the availability of freshwater resources for the cultivation of different types of aquaculture species.

- Fish is the largest aquaculture species produced in the region, accounting for 78.6% of aquaculture feed production. Countries such as Saudi Arabia, Oman, and the United Arab Emirates have invested in aquaculture and partnered with international experts and organizations to establish productive local fish farms. Aquaculture organizations in the Gulf region are working with the UK Government's Centre for Environment Fisheries and Aquaculture Science (Cefas) through the UK Gulf Marine Environment Partnership (GMEP) Programme to improve fish farming and tackle biodiversity loss.

- Oman and the United Arab Emirates have the highest per capita consumption of aquaculture species in the region, with consumption reaching 28.6 kg per person annually. In an effort to reduce exports and increase domestic production, the Omani government aims to transform the fisheries and aquaculture industry from a subsidy sector to a significant contributor to the country's economy.

Middle East Feed Enzymes Industry Overview

The Middle East Feed Enzymes Market is fragmented, with the top five companies occupying 25.79%. The major players in this market are Alltech, Inc., Brenntag SE, DSM Nutritional Products AG, IFF(Danisco Animal Nutrition) and Kerry Group Plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Iran

- 4.3.2 Saudi Arabia

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Carbohydrases

- 5.1.2 Phytases

- 5.1.3 Other Enzymes

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Iran

- 5.3.2 Saudi Arabia

- 5.3.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 BASF SE

- 6.4.4 Brenntag SE

- 6.4.5 Cargill Inc.

- 6.4.6 DSM Nutritional Products AG

- 6.4.7 Elanco Animal Health Inc.

- 6.4.8 IFF(Danisco Animal Nutrition)

- 6.4.9 Kemin Industries

- 6.4.10 Kerry Group Plc

- 6.4.11 Novus International, Inc.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms