スマートホームオートメーションの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

Smart Home Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698548

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

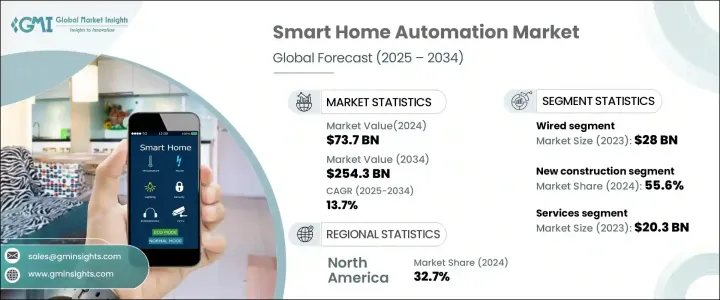

スマートホームオートメーションの世界市場規模は2024年に737億米ドルとなり、2025年から2034年にかけて13.7%のCAGRで成長すると予測されています。

人工知能(AI)とモノのインターネット(IoT)の急速な普及は、これらの技術がホームオートメーションの利便性と効率を高めるため、需要を促進しています。消費者は、スマートホームデバイスと統合し、照明、セキュリティシステム、サーモスタット、家電製品のシームレスな音声制御を可能にするAI搭載のバーチャルアシスタントを選ぶようになってきています。ハンズフリー操作とパーソナライズされた自動化の人気の高まりが、市場拡大の原動力となっています。

セキュリティは依然として、スマートホームソリューションの採用に影響を与える重要な要因です。AI主導の監視カメラ、スマートロック、警報システムは、顔認識やパターン認識を利用して個人を特定し、住宅所有者にリアルタイムで通知します。ホームセキュリティに対する懸念が高まる中、消費者は遠隔監視と保護強化を提供するインテリジェントセキュリティシステムに投資しています。さらに、主要エレクトロニクス企業はAIを製品に組み込んでおり、スマートホームデバイスがユーザーの行動を学習し、タスクを自動化し、よりパーソナライズされた生活体験を生み出すことを可能にしています。スマートホームの数は2023年に3億戸に達し、2028年には4億2,500万戸を超えると予測されており、世界の普及の著しい伸びを示しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 737億米ドル |

| 予測金額 | 2,543億米ドル |

| CAGR | 13.7% |

技術に基づき、市場は有線システムと無線システムに分類されます。2023年、有線セグメントは280億米ドルを占め、物理的なケーブルを通じて信頼性の高い接続性を提供します。設置には専門知識が必要ですが、これらのシステムは安定性があり、大規模な住宅や商業スペースに最適です。一方、無線セグメントは2022年に383億米ドルと評価され、その設置の容易さとWi-Fi、Zigbee、Z-Wave技術との互換性により人気を集めています。無線ソリューションは、特に既存住宅の改修に好まれており、自動化機能をアップグレードする一方で、混乱を最小限に抑えることができます。

フィットメント別の市場セグメンテーションには、新築と改修ソリューションがあります。2024年には、自動照明、高度なセキュリティシステム、インテリジェントなエネルギー管理ソリューションなど、エネルギー効率の高いスマートホーム機能の統合により、新築セグメントが市場シェアの55.6%を占めると予測されます。また、再生可能エネルギーの利用や節水機能など、持続可能性の側面も採用を後押ししています。一方、既存の住宅を自動化ソリューションでアップグレードすることで、エネルギー効率、快適性、全体的な機能性が向上するため、後付けセグメントは市場シェアの44.4%を占めると予想されます。

製品タイプ別に見ると、市場はハードウェアとサービスに分けられます。照明制御、セキュリティシステム、HVAC制御、エンターテイメントオートメーションなどを含むハードウェア分野は、2024年に517億米ドルで市場を独占しました。成長の背景には、スマートサーモスタット、ロック、カメラ、照明器具の普及があります。2023年に203億米ドルとなったサービス分野は、音声制御バーチャルアシスタントの家庭管理への利用の高まりにより拡大しています。

地域別では、利便性の向上、エネルギー効率、遠隔ホーム管理に対する消費者の需要が牽引し、北米が2024年に32.7%のシェアを獲得して市場をリードしました。米国市場だけで209億米ドルを占め、ホームオートメーションのためのスマート技術の採用が増加していることを反映しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 無線技術とIoTコネクティビティの進歩

- 政府の取り組みと支援

- エネルギー効率に対する需要の高まり

- 可処分所得の増加と都市化

- 業界の潜在的リスク・課題

- 急速な技術革新

- インターネット接続の信頼性と依存性

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ハードウェア

- 照明制御

- セキュリティ・アクセス

- 空調制御

- エンターテイメントコントロール・その他

- その他

- サービス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 有線

- 無線

第7章 市場推計・予測:フィットメント別、2021年~2034年

- 主要動向

- 新築

- レトロフィット

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- ABB Ltd.

- Acuity Brands

- Amazon(Ring)

- Apple Inc.(HomeKit)

- Control4 Corporation

- Crestron Electronics, Inc.

- Ecobee Inc.

- Google(Nest Labs)

- Honeywell International, Inc.

- Johnson Controls

- Koninklijke Philips N.V

- Legrand SA

- Leviton Manufacturing Company, Inc.

- Lutron Electronics Co., Inc.

- Resideo Technologies

- Samsung Electronics

- Savant Systems LLC

- Schneider Electric

- Siemens AG

目次

The Global Smart Home Automation Market was valued at USD 73.7 billion in 2024 and is projected to grow at a CAGR of 13.7% from 2025 to 2034. The rapid adoption of artificial intelligence (AI) and the Internet of Things (IoT) is fueling demand as these technologies enhance convenience and efficiency in home automation. Consumers are increasingly opting for AI-powered virtual assistants that integrate with smart home devices, enabling seamless voice control of lighting, security systems, thermostats, and household appliances. The rising popularity of hands-free operation and personalized automation is driving market expansion.

Security remains a key factor influencing the adoption of smart home solutions. AI-driven surveillance cameras, smart locks, and alarm systems utilize facial and pattern recognition to identify individuals and notify homeowners in real time. With growing concerns about home security, consumers are investing in intelligent security systems that offer remote monitoring and enhanced protection. Additionally, leading electronics companies are incorporating AI into their product offerings, enabling smart home devices to learn user behavior, automate tasks, and create a more personalized living experience. The number of smart homes reached 300 million in 2023 and is projected to surpass 425 million by 2028, indicating significant growth in adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $73.7 billion |

| Forecast Value | $254.3 billion |

| CAGR | 13.7% |

Based on technology, the market is categorized into wired and wireless systems. In 2023, the wired segment accounted for USD 28 billion, offering reliable connectivity through physical cables. Although installation requires professional expertise, these systems provide stability and are ideal for large residences and commercial spaces. Meanwhile, the wireless segment was valued at USD 38.3 billion in 2022, gaining traction due to its ease of installation and compatibility with Wi-Fi, Zigbee, and Z-Wave technologies. Wireless solutions are particularly favored for retrofitting existing homes, thus minimizing disruptions while upgrading automation capabilities.

Market segmentation by fitment includes new construction and retrofit solutions. In 2024, the new construction segment is anticipated to capture 55.6% of the market share, driven by the integration of energy-efficient smart home features such as automated lighting, advanced security systems, and intelligent energy management solutions. The sustainability aspect, including renewable energy harvesting and water conservation features, further boosts adoption. Meanwhile, the retrofit segment is expected to hold 44.4% of the market share, as upgrading existing homes with automation solutions enhances energy efficiency, comfort, and overall functionality.

By product type, the market is divided into hardware and services. The hardware segment, encompassing lighting control, security systems, HVAC control, and entertainment automation, dominated the market with USD 51.7 billion in 2024. Growth is attributed to the widespread adoption of smart thermostats, locks, cameras, and lighting fixtures. The services segment, valued at USD 20.3 billion in 2023, is expanding due to the rising use of voice-controlled virtual assistants for home management.

Geographically, North America led the market with a 32.7% share in 2024, driven by consumer demand for enhanced convenience, energy efficiency, and remote home management. The US market alone accounted for USD 20.9 billion, reflecting increasing adoption of smart technologies for home automation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in wireless technologies and IoT connectivity

- 3.6.1.2 Government initiatives and support

- 3.6.1.3 Increasing demand for energy efficiency

- 3.6.1.4 Rising disposable incomes and urbanization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Rapid technological changes

- 3.6.2.2 Reliability and dependence on internet connectivity

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Lighting control

- 5.2.2 Security & access

- 5.2.3 HVAC control

- 5.2.4 Entertainment control & others

- 5.2.5 Others

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Wired

- 6.3 Wireless

Chapter 7 Market Estimates & Forecast, By Fitment, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 New construction

- 7.3 Retrofit

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB Ltd.

- 9.2 Acuity Brands

- 9.3 Amazon (Ring)

- 9.4 Apple Inc. (HomeKit)

- 9.5 Control4 Corporation

- 9.6 Crestron Electronics, Inc.

- 9.7 Ecobee Inc.

- 9.8 Google (Nest Labs)

- 9.9 Honeywell International, Inc.

- 9.10 Johnson Controls

- 9.11 Koninklijke Philips N.V

- 9.12 Legrand SA

- 9.13 Leviton Manufacturing Company, Inc.

- 9.14 Lutron Electronics Co., Inc.

- 9.15 Resideo Technologies

- 9.16 Samsung Electronics

- 9.17 Savant Systems LLC

- 9.18 Schneider Electric

- 9.19 Siemens AG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日