|

|

市場調査レポート

商品コード

1683952

日本の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Japan Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

日本の自動車用LED照明市場規模は2025年に7億9,000万米ドルと推定され、2030年には11億7,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは8.13%で成長すると予測されます。

EV需要の増加と事故件数の増加が市場成長を牽引

- 金額シェアでは、2022年にヘッドライトがシェアの大半を占め、次いでその他、方向指示灯と続きます。予測期間中、方向指示器、後退灯、テールライト、ストップライトの市場シェアは変わらず、ヘッドライトは若干減少すると予想されます。前照灯のDRL(デイタイムランニングランプ)とプロジェクターライトの組み合わせは、日本の自動車照明市場における増加動向の一つです。

- 数量シェアでは、2022年には方向指示灯が過半数を占め、次いで前照灯、その他となっています。方向指示器用照明灯の市場シェアは変動が少なく、今後も変わらないと予想されます。方向指示灯は、あらゆるタイプの自動車において、小さな事故から大きな事故まで影響を受ける可能性が高く、交換が必要な主要部品です。

- 政府は安全基準を高めることで事故を減らすことを目指しており、その結果、自動ヘッドランプと方向指示器灯の需要が高まっています。例えば、日本政府は2025年までに交通関連死者を2,000人未満に減らすという目標を掲げています。2022年の全国の交通事故死者数は2,610人に減少し、2021年から1%減少しました。

- 事業拡大と技術革新の面で、日本は世界でも重要な自動車生産国のひとつです。市場の主要自動車メーカーは、市場における電気自動車の拡大に注力しています。例えば、2021年には新車販売台数に占める電気自動車の割合は36.2%となり、2019年の35.2%、2017年の32.9%から増加します。したがって、NEVの成長は市場におけるLEDの浸透を高めると思われます。

日本の自動車用LED照明市場動向

技術アップグレードとEV需要の増加がLED照明市場の成長を牽引

- インドの自動車総生産台数は2022年に941万台で、2023年には965万台に達すると予想されています。日本の自動車供給業界はCOVID-19の大流行により深刻な影響を受けました。日産は2020年5月下旬に世界生産を20%削減する方針でした。6月の日本の販売台数は23%の大幅減となり、トヨタが最も好調で、ホンダ、日産がこれに続いた。その結果、中国工場の閉鎖により、LED照明の生産に必要な自動車部品が不足しました。このため、日本の自動車用LED照明の生産は全体的に減少しました。

- 日本には、トヨタ、三菱、日産、ヤマハ発動機、いすゞ自動車、マツダ、レクサスといった大手自動車メーカーがあります。日本の自動車産業は、コネクティビティ、電動化、自動運転の開発に向かっています。CES 2017でトヨタは、同社のモビリティの未来像を示す「Concept-I」を発表しました。このクルマには「Yui」と名付けられた人工知能(AI)ヘルパーが搭載されており、LEDライトや音を通じてドライバーや道路上の他のドライバーとコミュニケーションをとる。

- 日本では、より安価な軽自動車(ガソリン車の場合、エンジンが660cc以下に分類される自動車)がEV市場の需要を牽引し、電気自動車の販売が急増しています。エネルギー効率が高いLEDライトは、需要の高まりとともにEVへの搭載が進んでいます。また、ダッシュボードストリップ照明の装飾用ストリップライトにLEDライトが使用されていることから、様々なスタイリングの自動車の室内照明にもLEDライトの使用が増加しています。

輸入車の増加と政府のEV購入補助金がLED照明市場の成長を促進

- 2022年現在、日本には28,546の充電ステーションがあります。2022年度の輸入電気自動車の国内販売台数は前年度比65%増の1万6,464台。日本で販売された乗用車は361万台で、2022年度中のEVは約7万7,000台でした。輸入車のEV比率が高いのは、海外メーカーが日本のライバルメーカーよりも幅広い商品を提供していることを反映している可能性があります。日本の自動車メーカーは一般に、中国のライバルの一部と比較して、電気自動車やプラグイン・ハイブリッド車の導入が遅れています。手頃な軽自動車が日本の電気自動車販売をリードしています。しかし、2022年度の日本の新車乗用車販売台数に占めるEVの割合は、中国や欧州の約20%に比べ、わずか2.1%にすぎないです。

- 日本政府はCEV購入補助金を提供しました。2021年の1台当たりのCEV補助金の上限額は80万円(7,200米ドル)でした。2023年1月、日本政府は、設置コストを削減するため、出力200kW以上の急速充電ステーションの安全規則を緩和する計画を発表しました。その過程で、HPCは50~200kWの直流充電ステーションと対等の立場に置かれることになります。

- 日本の自動車メーカーであるスバルは2022年5月、同国に電気自動車工場を新設し、2027年以降に操業を開始すると発表しました。日本初のEV専用工場となります。新工場に加え、現在の工場も電気自動車を一定台数生産できるよう改修する予定で、総投資額は約2,500億円(16億8,000万米ドル)を見込んでいます。このように、EV需要の拡大により、新たな発電所の開発・生産が見込まれ、それが自動車用LEDの需要を押し上げると予想されます。

日本の自動車用LED照明産業の概要

日本の自動車用LED照明市場はかなり統合されており、上位5社で108.03%を占めています。この市場の主要企業は以下の通りです。 KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH., Stanley Electric and Valeo(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- 日本

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

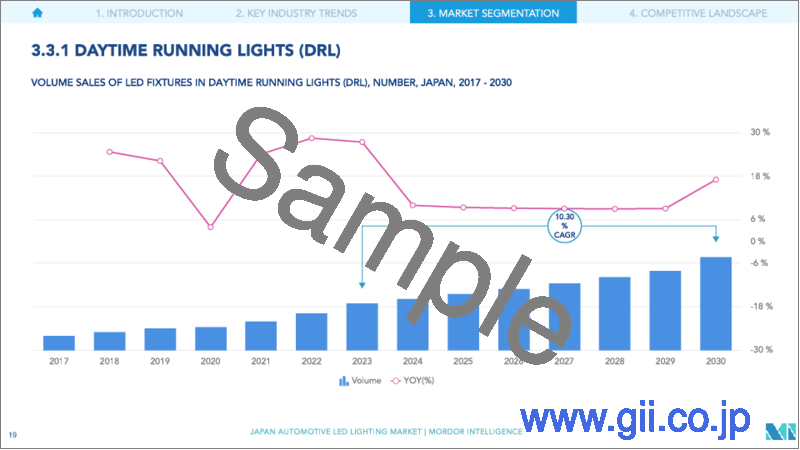

- デイタイムランニングライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- GRUPO ANTOLIN IRAUSA, S.A.

- HELLA GmbH & Co. KGaA

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

- Varroc Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Japan Automotive LED Lighting Market size is estimated at 0.79 billion USD in 2025, and is expected to reach 1.17 billion USD by 2030, growing at a CAGR of 8.13% during the forecast period (2025-2030).

Increasing demand for EVs and the increasing number of accidents are driving the growth of the market

- In terms of value share, in 2022, headlights accounted for the majority of the share, followed by others and directional signal lights. The market share is expected to remain the same for directional signal lights, reversing lights, taillights, and stoplights during the forecast period, with a small reduction in headlights. The combination of DRLs (daytime running lamps) with projector lights in frontal illumination is one of the increasing trends in the Japanese automobile lighting market.

- In terms of volume share, in 2022, directional signal lights accounted for the majority, followed by headlights and others. The market share is expected to remain the same with less fluctuation for these lights. Directional signal lights are the prime part that has a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement.

- The government aims to reduce accidents by increasing its safety standards, resulting in increasing demand for automated headlamps and directional signal lights. For instance, the Japanese government has set a goal of reducing traffic-related deaths to less than 2,000 by 2025. In 2022, the Traffic fatalities nationwide declined to 2,610, which is down by 1% from 2021.

- In terms of expansion and innovations, Japan is one of the significant auto-producing nations in the world. The key automotive manufacturers in the market are focusing on expanding electric vehicles in the market. For instance, in 2021, new electric vehicles accounted for 36.2% of total new car sales, up from 35.2% in 2019 and 32.9% in 2017. Thus, the growth in NEV would increase the penetration of LED in the market.

Japan Automotive LED Lighting Market Trends

Technology upgradation and increasing demand for EVs drive the LED lighting market's growth

- The total automobile vehicle production in India was 9.41 million units in 2022, and it is expected to reach 9.65 million units in 2023. The automotive supply industry in Japan was severely affected by the COVID-19 pandemic. Nissan intended to reduce global production by 20% in late May 2020. Sales in Japan fell drastically by 23% in June, with Toyota performing the best, followed by Honda and Nissan. As a result, the closure of Chinese factories led to a scarcity of the automobile components needed to produce LED lights. This led to a decline in Japan's overall manufacturing of car LED lighting.

- Japan has major automotive manufacturers such as Toyota, Mitsubishi, Nissan, Yamaha Motor Company, Isuzu Motors Ltd, Mazda, and Lexus. Japan's auto industry is moving toward developing connectivity, electrification, and automated driving. At CES 2017, Toyota unveiled its Concept-I car to demonstrate the company's vision for the future of mobility. The vehicle has an artificial intelligence (AI) helper named 'Yui' that communicates with the driver and other drivers on the road via LED lights and sounds.

- Sales of electric vehicles are rising rapidly in Japan, driven by cheaper "Kei" minicars (vehicles classified with engines of 660 cc or less in the case of gasoline models), which are driving the demand for the EV market. Due to their high energy efficiency, LED lights are becoming increasingly common in EVs as their demand rises. Due to the use of LED lights in strip lights for decorative purposes in dashboard strip lighting, the use of LED lights in interior lighting of vehicles in varied styling is also rising.

An increase in imported cars and government subsidies for the purchase of EVs drive the growth of the LED lighting market

- As of 2022, there were 28,546 charging stations in Japan. The number of imported electric vehicles sold in the country during FY 2022 rose 65% from the previous year to 16,464 units. There were 3.61 million passenger cars sold in Japan, and about 77,000 were EVs during FY 2022. The higher EV percentage for imported cars may reflect the wider variety of products offered by foreign makers than their Japanese rivals. Japanese car manufacturers have generally been slow to adopt electric and plug-in hybrid vehicles compared to some of their Chinese rivals. Affordable Kei minicars lead Japan's electric vehicle sales. However, EVs accounted for only 2.1% of new passenger car sales in Japan in FY 2022 compared to roughly 20% in China and Europe.

- The Japanese government offered subsidies to purchase CEVs. The maximum amount of the CEV subsidies given per vehicle in 2021 was JPY 800,000 (USD 7,200). In January 2023, the Japanese government announced the plan to ease safety rules for fast charging stations with more than 200 kW of power to reduce installation costs. In the process, HPCs will be placed on an equal footing with DC charging stations ranging from 50 to 200 kW.

- Subaru, a Japanese automaker, declared in May 2022 that it would build a new electric vehicle plant in the country, starting operations after 2027. It would be the first EV-only factory in Japan. In addition to the new facility, the current plant will be retooled to produce a specific number of electric vehicles, with an anticipated total investment of about JPY 250 billion (USD 1.68 billion). Thus, the above instances are expected to lead to the development and production of new power stations owing to the growing demand for EVs, which, in turn, is expected to boost the demand for automotive LEDs.

Japan Automotive LED Lighting Industry Overview

The Japan Automotive LED Lighting Market is fairly consolidated, with the top five companies occupying 108.03%. The major players in this market are KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 Japan

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA

- 6.4.3 KOITO MANUFACTURING CO., LTD.

- 6.4.4 Marelli Holdings Co., Ltd.

- 6.4.5 Nichia Corporation

- 6.4.6 OSRAM GmbH.

- 6.4.7 Signify (Philips)

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 Varroc Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms