|

市場調査レポート

商品コード

1683937

欧州の屋内用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Indoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の屋内用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 194 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

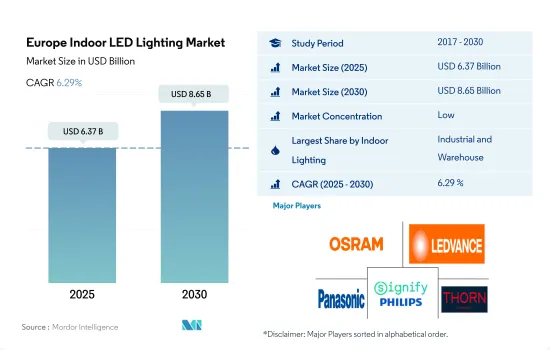

欧州の屋内用LED照明市場規模は、2025年に63億7,000万米ドルと推定され、2030年には86億5,000万米ドルに達すると予測され、予測期間(2025-2030)のCAGRは6.29%で成長します。

産業・住宅分野の開発増加が市場成長を牽引

- 金額ベースでは、2023年時点で産業用と倉庫用が大きなシェアを占め、商業用、住宅用、農業用照明がこれに続きます。フランス、ロシア、ポーランドが倉庫建設の大半を占めています。COVID-19危機は、フランスの工業生産能力をパンデミック以前の水準に戻す努力を加速させました。フランスの鉱工業生産は、2022年11月に2%増加した後、12月には1ヵ月で1.1%増加しました。ポーランドには440万㎡近いスペースがあります。2022年半ばまでに、ポーランドでは450万㎡近い倉庫・工業用スペースが建設中でした。

- 商業施設では、病院、学校、空港がシェアの大半を占めています。調査対象となった42カ国の可処分所得は大きく異なります。リヒテンシュタイン、スイス、ルクセンブルクは、可処分所得が圧倒的に高く、学校や大学で学ぶ余裕があります。

- 2023年の時点で、住宅部門が大きなシェアを占めています。イタリアの住宅市場は、旺盛な需要に支えられ、引き続き安定しています。2021年第4四半期の住宅用不動産取引は、前年同期比14.1%増の263,795戸となりました。全地域で好調な販売増となりました。多くの企業が移行期にあるにもかかわらず、オフィスの利用率は2022年1月の前回の封鎖終了から上昇傾向が続いた。2022年第3四半期現在、オフィスセクターの平均ディスカウント率は26%で、全体平均の31%を下回りました。2022年末時点の全体の空室率は7.2%で、2021年末時点(+10bp)と比べてほぼ安定しています。全体として、オフィスと住宅の吸収率は上昇傾向にあり、LED需要の大幅な増加につながります。

工業生産の増加と住宅の急増が市場の需要を牽引

- 2023年現在、金額と数量で見ると、その他欧州が大きなシェアを占めており、フランス、ドイツ、英国がこれに続いています。その他欧州には、スウェーデン、イタリア、スペイン、ロシア、ポーランド、オランダなどが含まれます。米国や北欧からの外国人バイヤーがスペイン南海岸の住宅を購入しています。住宅ローン金利が大幅に上昇したにもかかわらず、2022年の不動産需要は引き続き旺盛で、2021年と比較して取引件数は16%急増し、住宅ローン実行件数は11%増加しました。欧州では、ポーランドが約440万平方メートルのスペースを確保してトップに立りました。2022年半ばまでに、ポーランドではほぼ450万㎡の倉庫・産業用スペースが建設中でした。全体として、倉庫建設が増加し、この地域の住宅が急増することで、LEDの需要は増加すると予想されます。

- マヨットを除くフランスの2022年1~11月の新築許可戸数は、前年同期比5.6%増の44万8,416戸で、2021年中の18.5%増に続いて増加しました。COVID-19の閉じ込め以来、フランスでは多くの人々が大都市から地方に移り住んでいます。全体として、住宅市場は今後数年間はより安定すると予想されます。

- ドイツでは、研究開発費全体の約60%を占めるドイツの産業企業が国の繁栄に大きく貢献しています。企業は戦略的開発にも取り組んでいます。例えば2023年、オスヴェトレニ・セルノッホSROは工業生産能力を増強するため、新しい生産・貯蔵ホールを建設しました。このような拡張は、産業と保管場所の増加とLED照明の使用を示しています。

欧州の屋内用LED照明市場動向

可処分所得の増加と政府のインセンティブによりLEDの普及が進む可能性

- 2022年、EUには1億9,800万世帯が居住し、1世帯当たり平均2.2人が居住していました。同地域の人口は2020年に7億4,620万人でしたが、2023年には7億4,220万人に減少。EUの持ち家率は、2021年の69.90%から2022年には69.10%に低下しました。このような事例は、世帯数が若干減少しているにもかかわらず、住宅開発プロジェクトが例年より少ないことを示唆しています。したがって、LEDの普及はプラスに成長すると予想されるが、住宅セグメントでは以前に比べて減少しています。

- 欧州では、ほとんどの国で可処分所得が高く、その結果、特に新しい住宅スペースに対する個人の消費力が高まっています。英国の一人当たり所得は2022年に3万3,138米ドルに達し、フランスのそれは25,337.7米ドルに達しました。

- 欧州では、政府がLED普及のためのインセンティブ・プログラムを提供しています。英国政府は、エネルギー効率の高い照明に関する新たな提案を発表しました。この案では、エネルギー使用量の少ないLEDなどの照明が、古いハロゲン電球に取って代わることになります。このような取り組みにより、電球の耐用年数で2,000英ポンドから3,000英ポンドを家庭で節約できる可能性があります。ドイツでは2021年1月、「効率的な建物に対する連邦政府の資金援助」プログラムが開始されました。ドイツ国内に不動産を所有している人、または購入を検討している人は誰でもこの資金援助に応募できます。このエネルギー効率化プログラムには、照明エネルギー効率の高い建物も含まれています。2017年6月、フランス政府は省エネ証明書制度を発表し、世帯主の所得に応じてLED電球の価格の最大100%をカバーできる補助金を得ることができるようになりました。このような事例は、予測期間中、この地域におけるLED照明の需要を押し上げると予想されます。

政府プログラムとハロゲン電球の販売禁止がLED照明の成長を促進する可能性

- EUにおける主要なエネルギー消費者の1つである産業部門は、2021年の総エネルギー消費量の25.6%を占め、次いで家庭部門と商業部門が最も多くのエネルギーを使用しています。かなりの数の家庭がスマートホーム技術に移行しており、住宅などの屋内空間における照明制御の需要が予想外の割合で高まっています。2020年9月に発表された欧州グリーンディールの目玉は、EU政権が実施した住宅リノベーションプログラムです。こうしたプログラムは、この地域でのLED照明の拡大を支援しています。

- 商業部門の電力需要は8~10時間前後の傾向があり、工業部門の電力使用量は1日や1年を通して変動がないです。住宅部門の電力需要は、約7~9時間変動します。市長会議-実証事業計画では、カンテミール市の27の道路を改修し、419個のスマートLED照明を設置しました。オクニタでは、大気中に放出されるCO2の量を減らすため、約386個の非効率な電球が交換され、その結果、同地域でLEDの使用が増加しました。

- 2018年9月、同地域は無指向性ハロゲン電球の販売も禁止しました。こうした法改正により、消費者は従来の照明からLED技術への切り替えを徐々に進めやすくなっています。同地域の政府も、LEDアイテムの消費者受容を高めるために、旧式の効率の低い技術を段階的に廃止しており、また同地域のLEDの全体的な効率を高めるために補助金やインセンティブを与えています。

欧州の屋内用LED照明産業概要

欧州の屋内用LED照明市場は断片化されており、上位5社で37.37%を占めています。同市場の主要企業は以下の通りです。ams-OSRAM AG, LEDVANCE GmbH(MLS), Panasonic Holdings Corporation, Signify(Philips)and Thorn Lighting Ltd.(Zumtobel Group)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たり所得

- LEDの総輸入量

- 照明の電力消費量

- 世帯数

- LED普及率

- 園芸面積

- 規制の枠組み

- フランス

- ドイツ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 屋内照明

- 農業用照明

- 商業用照明

- オフィス

- 小売

- その他

- 産業・倉庫

- 住宅

- 国名

- フランス

- ドイツ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ams-OSRAM AG

- Dialight

- EGLO Leuchten GmbH

- LEDVANCE GmbH(MLS Co Ltd)

- NVC INTERNATIONAL HOLDINGS LIMITED

- Panasonic Holdings Corporation

- Signify(Philips)

- Thorlux Lighting(FW Thorpe Plc)

- Thorn Lighting Ltd.(Zumtobel Group)

- TRILUX GmbH & Co. KG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Indoor LED Lighting Market size is estimated at 6.37 billion USD in 2025, and is expected to reach 8.65 billion USD by 2030, growing at a CAGR of 6.29% during the forecast period (2025-2030).

Increasing development in the industrial and residential sectors drives market growth

- In terms of value, as of 2023, industrial and warehouse had a major share, followed by commercial, residential, and agricultural lighting. France, Russia, and Poland had the majority of warehouse constructions. The COVID-19 crisis accelerated France's efforts to return industrial production capacities to the pre-pandemic levels. French industrial production increased by 1.1% over one month in December 2022, after +2% in November 2022. Poland has close to 4.4 million sq. m of space. By the middle of 2022, almost 4.5 million sq. m of warehouse and industrial space was under construction in Poland.

- In commercial, hospitals, schools, and airports comprise the majority of the share. The disposable net income among the 42 countries surveyed varies significantly. Liechtenstein, Switzerland, and Luxembourg have the highest disposable net income by a wide margin, which means more affordability for schools and college studies.

- In terms of volume, as of 2023, the residential sector had a major share. Italy's housing market remains stable, supported by strong demand. In Q4 2021, residential property transactions increased by 14.1% to 263,795 units compared to a year earlier. All regions saw a strong sales increase during the period. Despite many businesses remaining in transition, office usage rates continued on an upward trend from the end of the last lockdown in January 2022. As of Q3 2022, the office sector traded at an average discount of 26%, which was below the 31% overall average. The overall vacancy rate stood at 7.2% at the end of 2022, almost stable compared to the end of 2021 (+10bp). Overall, there is a positive trend toward a higher office and residential absorption rate, leading to a major increase in the demand for LEDs.

Growing number of industrial production and surge in residential property drive the demand for market

- In terms of value and volume, as of 2023, the Rest of Europe held the major share, followed by France, Germany, and the United Kingdom. The Rest of Europe comprises Sweden, Italy, Spain, Russia, Poland, Netherlands, and others. Foreign buyers from the United States and northern Europe have been buying homes on Spain's southern coast. Despite a significant rise in mortgage rates, demand for real estate remained strong in 2022, with a 16% surge in transactions and an 11% uptick in mortgage production compared to 2021. In Europe, Poland was at the top with nearly 4.4 million sq. m of space. By the middle of 2022, almost 4.5 million sq. m of warehouse and industrial space was under construction in Poland. Overall, the demand for LEDs is expected to increase with increasing warehouse construction and a surge in residential property in the region.

- In the first eleven months of 2022, new dwellings authorized in France, excluding Mayotte, rose by 5.6% to 448,416 units compared to the same period the previous year, following an 18.5% increase during 2021. Since COVID-19 confinements, many people have moved from the major cities to the provinces in France. Overall, the residential market is expected to be more stable in the coming years.

- In Germany, with around 60% of total R&D expenditure, German industrial companies significantly contribute to the country's prosperity. Companies also engage in strategic development. For instance, in 2023, Osvetleni Cernoch SRO built a new production and storage hall to increase its industrial production capacity. Such expansions indicate an increase in the number of industries and storage areas and the use of LED lighting.

Europe Indoor LED Lighting Market Trends

Increasing disposable income and government incentives may lead to more LED penetration

- In 2022, 198 million households resided in the EU, with 2.2 members per household on average. The region's population was 746.2 million in 2020, which reduced to 742.2 million by 2023. Homeownership rates in the EU declined by 69.10% in 2022 from 69.90% in 2021. Such instances suggest that housing development projects are less than in previous years despite a slight decline in the number of households. Thus, LED penetration is expected to grow positively but less in the residential segment compared to previous years.

- In Europe, disposable income is high for most countries, resulting in rising spending power of individuals, especially on new residential spaces. The United Kingdom's per capita income reached USD 33,138 in 2022, while that of France reached USD 25,337.7.

- In Europe, the governments provide incentive programs to create more LED penetration. The UK government announced the launch of a new energy-efficient lighting proposal. Under this, lighting, such as low energy-use LEDs, would replace old halogen bulbs. Such initiatives could save households between GBP 2,000 and GBP 3,000 over the lifetime of these bulbs. The "Federal Funding for Efficient Buildings" program was launched in January 2021 in Germany. Anyone who owns a property in Germany or who is looking to buy property in the country can apply for the funding. The energy efficiency program also includes lighting energy efficiency buildings. In June 2017, the French government announced the Energy Savings Certificate scheme, which allows people to get subsidies that can cover up to 100% of the price of LED bulbs based on the householder's income. Such instances are expected to boost the demand for LED lighting in the region during the forecast period.

Government programs and the prohibition of the sale of halogen bulbs may drive the growth of LED lighting

- One of the main energy consumers in the EU, the industry sector accounted for 25.6% of total energy consumption in 2021, followed by the household and commercial sectors, which used the most energy. A significant number of households are converting to smart home technologies, which has increased the demand for lighting control in indoor spaces, such as residential buildings, at unexpected rates. The central feature of the European Green Deal, which was unveiled in September 2020, is the Housing Renovation Program, which was implemented by the EU administration. Such programs are assisting the expansion of LED lighting in the region.

- The demand for electricity in the commercial sector tends to be around 8-10 hours, while electricity use in the industrial sector does not fluctuate throughout the day or year. Electricity demand in the residential sector varies for about 7-9 hours. The Covenant of Mayors - Demonstration Projects scheme refurbished 27 roadways in Cantemir and installed 419 smart LED lighting. About 386 inefficient bulbs were replaced in Ocnita to lower the amount of CO2 released into the atmosphere, thus causing a rise in the use of LEDs in the region.

- In September 2018, the region also prohibited the sale of non-directional halogen bulbs. These legislative changes have made it easier for consumers to progressively switch from conventional lighting to LED technology. The governments in the region are also phasing out older, less efficient technologies to boost consumer acceptance of LED items, as well as giving subsidies and incentives to enhance the overall efficiency of LEDs in the region.

Europe Indoor LED Lighting Industry Overview

The Europe Indoor LED Lighting Market is fragmented, with the top five companies occupying 37.37%. The major players in this market are ams-OSRAM AG, LEDVANCE GmbH (MLS Co Ltd), Panasonic Holdings Corporation, Signify (Philips) and Thorn Lighting Ltd. (Zumtobel Group) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 Per Capita Income

- 4.3 Total Import Of Leds

- 4.4 Lighting Electricity Consumption

- 4.5 # Of Households

- 4.6 Led Penetration

- 4.7 Horticulture Area

- 4.8 Regulatory Framework

- 4.8.1 France

- 4.8.2 Germany

- 4.8.3 United Kingdom

- 4.9 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Indoor Lighting

- 5.1.1 Agricultural Lighting

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Others

- 5.1.3 Industrial and Warehouse

- 5.1.4 Residential

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 United Kingdom

- 5.2.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ams-OSRAM AG

- 6.4.2 Dialight

- 6.4.3 EGLO Leuchten GmbH

- 6.4.4 LEDVANCE GmbH (MLS Co Ltd)

- 6.4.5 NVC INTERNATIONAL HOLDINGS LIMITED

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Signify (Philips)

- 6.4.8 Thorlux Lighting (FW Thorpe Plc)

- 6.4.9 Thorn Lighting Ltd. (Zumtobel Group)

- 6.4.10 TRILUX GmbH & Co. KG

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms