|

市場調査レポート

商品コード

1644805

シンガポールの決済-市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Singapore Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポールの決済-市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 99 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

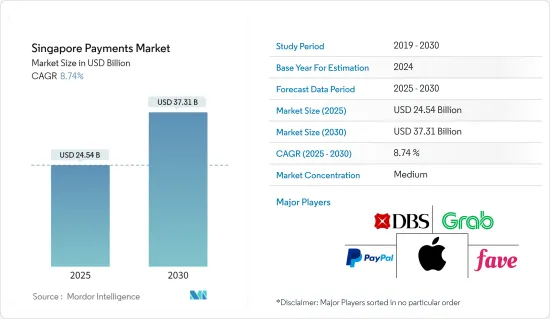

シンガポールの決済市場規模は2025年に245億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.74%で、2030年には373億1,000万米ドルに達すると予測されます。

主要ハイライト

- リアルタイム決済の継続的な成長と、デジタル化を奨励する政府の取り組みが市場成長を促進すると予想されます。政府がノンバンク金融機関(NFI)に銀行リテールの決済インフラへのアクセスを許可したことで、シンガポールのインスタント決済はさらに増加するとみられます。決済サービス法による大手決済機関の認可を受けたNFIは、FASTとPayNowに直接リンクすることができるようになりました。

- シンガポール政府が掲げるスマート決済国家構想の主要目標のひとつに、電子決済社会の構築があります。シンガポールの決済部門は現在、近代的で、新しい参入企業にも開かれています。この産業はノンバンク金融機関(NFI)も利用でき、電子財布間の競争と相互運用性を促進しています。例えば、ライドヘイリング会社のGrabはGrab Payを導入し、通信会社のSingtelはダッシュペイDash Payを導入しました。

- 世界経済の急速な発展に伴い、携帯電話(特にスマートフォン)は個人の生活に欠かせないものとなりました。さらに、世界中のほとんどの個人にとって、インターネットは日常生活に欠かせない要素となっています。その結果、携帯電話やインターネットの利用者数は世界的に急増し、決済セグメントは大きく拡大しました。

- さらに、Visaが実施した最新のBack to Business調査では、国内の中小・零細企業(SMB)の過半数(94%)が2022年に新たな決済手段の導入を模索しており、89%がそうすることが成長の基礎になると回答していることが明らかになりました。SMBが利用を検討している決済方法には、電子財布アプリ(59%)、モバイル非接触決済(58%)、非接触カード(43%)、Buy Now Pay Laterソリューション(35%)、デジタル通貨(33%)があります。

- シンガポール警察(SPF)の最新の数字によると、同国の詐欺・サイバー犯罪件数は2022年に3万3,669件と過去最高を記録し、前年比25.2%増となりました。eコマースはシンガポールで報告された詐欺の上位5種類に入っています。詐欺師はしばしば電子メール、テキストメッセージ、電話を使って対象をだます。例えば、役人や信頼できる団体のふりをして、被害者に銀行口座やクレジットカード情報などの個人情報を明かすよう説得します。、詐欺師はそのデータを使って不正な取引を行っています。こうした動向は市場の成長を妨げる可能性があります。

シンガポールの決済市場動向

シンガポールの決済市場はeコマースのブームが牽引役

- 国際貿易局(ITA)によると、シンガポールのeコマース市場は2021年に59億米ドルと評価され、2026年には100億米ドルに拡大すると予想されています。この地域のeコマース利用者は300万人を超えます。一人当たりの所得が6万5,000米ドルであるシンガポールは、アジアで最も豊かな国のひとつでもあります。

- インターネット普及率の上昇は、eコマース市場を牽引する主要要因のひとつです。例えば、ITAによると、シンガポールのインターネット普及率は98%、スマートフォンの普及率は93%で、58%の国民がオンラインショッピングを利用しています。

- シンガポールの決済ビジネスでは、革新的なデジタルの決済の選択肢が急増しています。スマートフォンの利用が増加し、PayPalやBuy Now Pay Laterサービスなどのデジタルウォレット決済オプションが登場したことで、シンガポールのオンライン決済の最新動向第1位に浮上しました。

シンガポールの決済市場で著しい成長を見せる小売産業

- 小売産業はシンガポールで最も急成長している産業のひとつです。その結果、小売産業は新しいビジネス、取引、投資の機会が豊富にあります。シンガポールの決済市場は、顧客行動の変化とともに開拓されています。モバイルの決済、インターネット・バンキング、インスタント決済、政府の成長イニシアティブなどの動向は、シンガポールの決済市場に影響を与えています。

- さらに、小売業はシンガポールを旅行や居住に適した場所にする上で極めて重要な役割を果たしています。このセグメントもパンデミックの影響から力強く回復を続けており、シンガポール統計局(DoS)は2022年11月の小売売上高が前年同月比6.2%増となったと発表しました。

- さらに、このような小売セクターの着実な成長は、この地域の決済プロバイダーにとって、拡大する需要に対応するために決済プラットフォームやアプリを改善する多くの機会をもたらしています。さらに、同地域ではデジタルウォレットや非接触型カード決済の利用が増加しており、決済プロバイダーにとって有利な可能性があります。

- また、2022年4月から、シンガポールの小売業者は、シンガポールを拠点とする大手決済機関FOMO Payが導入した新しい暗号決済ソリューションを通じて、デジタルの決済トークン(DPT)を受け入れることができるようになりました。小売業者を対象としたこの新しい決済方法は、シンガポールのDPTライセンシーによって開発された初めてのものだといいます。FOMO Payは、EuroSports Global、2ToneVintage、Luxehouzeなどの高級小売業者を対象に、規制に準拠した新しいソリューションの導入を開始しました。

- シンガポールでは、地元のタクシー会社ComfortDelgroがフードデリバリーサービスを開始し、Googleがシンガポール全土でフードピックアップとデリバリーの選択肢を見つけることを可能にするなど、インターネットデリバリーの需要増に対応した新しいサービスが開始されています。住民が自宅にこもり、COVID-19の流行を管理するために国の安全距離規制に従っているため、小売店や食事の宅配サービスが大幅に増加しています。

シンガポールの決済産業概要

シンガポールの決済市場は、DBS PayLah、GrabPay、Paypal、Fave Pay、Alipayなどの主要な市場参入企業によって適度な競合を示しています。これらの企業は市場でのプレゼンスを積極的に拡大しており、市場全体の成長に貢献しています。さらに、デジタルの決済を推進する政府の積極的な取り組みにより、当面の市場競争は激化すると予想されます。

DBSは2022年12月、国際航空運送協会(IATA)と提携し、アジアの主要3市場でIATA Payを開始すると発表しました。この取り組みは香港で開始され、2023年にはインドネシアとシンガポールにも拡大する予定です。IATAペイは、銀行口座からの引き落としを可能にすることで、旅行者がオンラインで航空券を購入する方法に革命をもたらします。この技術革新により、特にクレジットカードやデビットカードを利用できない消費者の金融包摂が促進されます。

2022年11月、StraitsXとGrabは、2022年シンガポール・フィンテック・フェスティバルの期間中、5,000人の参加者の中から選ばれたグループでPurpose Bound Money(PBM)を試行するための協力関係を発表しました。PBMトークンは、決済用の代替デジタル通貨を提供し、加盟店のデジタルウォレットに即座に送金することができ、革新的な決済ソリューションを記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 国内における決済環境の進化

- 国内におけるキャッシュレス取引の拡大に関連する主要市場動向

- COVID-19が同国の決済市場に与える影響

第5章 市場力学

- 市場促進要因

- シンガポールの決済市場はeコマース産業の活況に牽引されています。

- 大手小売業者と政府は、活性化プログラムを通じて市場のデジタル化を推進しています。

- リアルタイム決済、特にBuy Now Pay Laterの利用増加

- 市場課題

- 業務システムへのデジタルツールの統合が困難

- シンガポールにおけるeコマース詐欺

- 市場機会

- キャッシュレス社会への移行

- 新規参入企業によるイノベーションが普及を促進

- デジタルの決済産業における主要規制と基準

- 主要事例と使用事例の分析

- 国内の決済産業に関連する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢・所得などを含む範囲)

- 国内における顧客満足度重視の高まりと世界の動向の融合に関する分析

- 国内における現金離れと非接触型決済モードの台頭の分析

第6章 市場セグメンテーション

- 決済モード別

- 販売時点情報管理(POS)

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他の店頭販売

- オンライン販売

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他のオンライン販売(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- 販売時点情報管理(POS)

- エンドユーザー産業別

- 小売

- エンターテインメント

- 医療

- ホスピタリティ

- その他

第7章 競合情勢

- 企業プロファイル

- DBS Bank Ltd

- PayPal Holdings, Inc.

- Grab

- Fave

- Apple Inc.

- Google Pay

- SingCash Pte. Ltd.

- Samsung

- Alipay

- Amazon.com, Inc.

第8章 投資分析

第9章 市場の将来展望

The Singapore Payments Market size is estimated at USD 24.54 billion in 2025, and is expected to reach USD 37.31 billion by 2030, at a CAGR of 8.74% during the forecast period (2025-2030).

Key Highlights

- The ongoing growth of real-time payments and the government's efforts to encourage digitalization are expected to drive market growth. With the government now allowing non-bank financial institutions (NFIs) to access banking retail payment infrastructure, instant payments in Singapore are set to increase even more. NFIs that have been granted a major payment institution licensed under the Payment Services Act are now permitted to link directly to FAST and PayNow.

- One of the primary goals of the Singapore government's Smart Nation vision is to build an e-payments society, which is one of the key goals. The payments sector in Singapore is now modern and open to new players. This industry is available to non-bank financial institutions (NFIs), promoting competition and interoperability among e-wallets. For instance, Grab, a ride-hailing firm, introduced GrabPay, and Singtel, a telecommunications company, introduced DashPay.

- Mobile phones (notably smartphones) have become an integral aspect of an individual's life as the global economy has grown rapidly. Furthermore, for most individuals worldwide, the internet has become an indispensable element of their daily lives. As a result, the number of cell phones and internet users has surged worldwide, resulting in a major expansion in the payments sector.

- Further, the latest Back to Business study by Visa revealed that the majority (94%) of small and micro businesses (SMBs) in the country were seeking to adopt new payment methods in 2022, with 89% saying doing so would be fundamental to their growth. Amongst the methods that SMBs were considering using are e-wallet apps (59%), mobile contactless payments (58%), contactless cards (43%), Buy Now Pay Later solutions (35%), and digital currencies (33%).

- As per the latest figures from the Singapore Police Force (SPF), the number of scam and cybercrime cases in the country hit an all-time high of 33,669 in 2022, with a 25.2% YoY increase. E-commerce was among the top five types of scams reported in Singapore. Scammers often use emails, text messages, or phone calls to deceive their targets. For instance, they pretend to be officials or trusted entities to convince victims to reveal their personal information, like bank accounts or credit card details. Scammers then use the data to carry out unauthorized transactions. Such trends may hinder market growth.

Singapore Payments Market Trends

The payments market in Singapore is driven by boom in the e-commerce industry

- According to the International Trade Administration (ITA), the Singapore e-commerce market was valued at USD 5.9 billion in 2021 and is expected to rise to USD 10 billion by 2026. The region has over 3 million e-commerce users. With a per capita income being USD 65,000, Singapore is also one of the most affluent countries in Asia.

- The increase in Internet penetration is one main factor driving the e-commerce market. For instance, as per ITA, the country has an internet penetration rate of 98% and a smartphone penetration rate of 93%, along with a 58% rate of residents making online purchases.

- Singapore's payments business is seeing a surge of innovative digital payment alternatives. It has emerged as the newest number-one trend for online payments in Singapore, owing to the increasing use of smartphones and the advent of digital wallet payment options such as PayPal and Buy Now Pay Later services.

Retail industry shows the significant growth in Payments Market of Singapore

- The retail industry is one of the fastest-growing industries in Singapore. As a result, the retail sector represents a wealth of opportunities for new business, trading, and investing. The payment market in Singapore is developing with the changing customer behavior. Trends such as mobile payments, internet banking, instant payments, and the Government's growth initiatives are affecting the payment market in the country.

- Moreover, retailing plays a pivotal role in making Singapore a viable place to travel and reside. The sector also continues to recover strongly from the impacts of the pandemic, with the Department of Statistics (DoS) of Singapore announcing that the country's retail sales grew by 6.2% year on year in November 2022.

- Furthermore, This steady growth in the retail sector presents many opportunities for payment providers in the region to improve their payment platforms and apps to meet the growing demand. In addition, the increasing use of digital wallets and contactless card payments in the region presents a lucrative potential for payment providers.

- Also, starting in April 2022, retailers in Singapore were able to accept digital payment tokens (DPT) through a new crypto payment solution introduced by Singapore-based major payment institution FOMO Pay. The new payment method targeted at retailers was claimed to be the first such to be developed by a DPT licensee in Singapore. FOMO Pay started implementing its new solution with luxury retailers - such as EuroSports Global, 2ToneVintage, and Luxehouze, amongst others - in compliance with regulations.

- In Singapore, new services are being launched to meet the increased demand for internet delivery, with local cab company ComfortDelgro establishing a food delivery service and Google enabling the finding of food pick-up and delivery choices throughout the city-state. As residents hide down at home and follow the country's safe-distance regulations to manage the COVID-19 epidemic, there has been a huge increase in retail and meal delivery services.

Singapore Payments Industry Overview

The Singapore payments market exhibits moderate competitiveness with key market players, including DBS PayLah, GrabPay, Paypal, Fave Pay, and Alipay. These companies are actively expanding their market presence, thereby contributing to the overall market growth. Furthermore, the government's proactive initiatives to promote digital payments are anticipated to intensify market competition in the foreseeable future.

In December 2022, DBS announced its partnership with the International Air Transport Association (IATA) to launch IATA Pay across three key Asian markets. This initiative commenced in Hong Kong and is scheduled to extend to Indonesia and Singapore in 2023. IATA Pay revolutionizes the way travelers purchase air tickets online by enabling direct debits from their bank accounts. This innovation enhances financial inclusion, particularly for consumers without access to credit or debit cards.

In November 2022, StraitsX and Grab unveiled their collaboration to trial Purpose Bound Money (PBM) with a selected group of 5,000 participants during the 2022 Singapore Fintech Festival. The PBM token offers an alternative digital currency for making payments and can be instantly transferred to a merchant's digital wallet, presenting an innovative payment solution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in the country

- 4.5 Key market trends pertaining to the growth of cashless transaction in the country

- 4.6 Impact of COVID-19 on the payments market in the country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The payments market in Singapore is driven by boom in the e-commerce industry

- 5.1.2 Major retailers and the government are promoting Market Digitization through activation programs.

- 5.1.3 Increased use of real-time payments, specifically Buy Now Pay Later.

- 5.2 Market Challenges

- 5.2.1 Difficult to integrate digital tools into the business systems

- 5.2.2 e-Commerce scams in Singapore

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in the country (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in the country

- 5.8 Analysis of cash displacement and rise of contactless payment modes in the country

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Other Point of Sales

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 DBS Bank Ltd

- 7.1.2 PayPal Holdings, Inc.

- 7.1.3 Grab

- 7.1.4 Fave

- 7.1.5 Apple Inc.

- 7.1.6 Google Pay

- 7.1.7 SingCash Pte. Ltd.

- 7.1.8 Samsung

- 7.1.9 Alipay

- 7.1.10 Amazon.com, Inc.