インドの決済-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

India Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644590

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

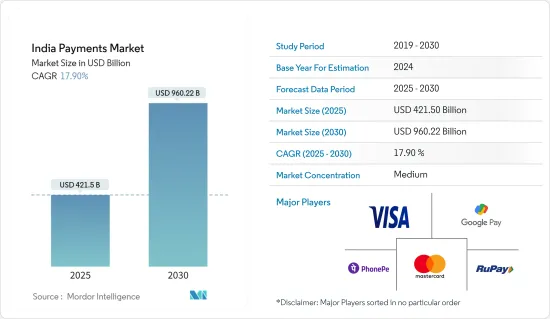

インドの決済市場規模は2025年に4,215億米ドルと推定され、予測期間中(2025~2030年)のCAGRは17.9%で、2030年には9,602億2,000万米ドルに達すると予測されます。

主要ハイライト

- インドではオンラインショッピング利用者の増加に支えられ、インターネット上で商品やサービスを購入することが決済市場の主要促進要因の1つとなっており、UPI取引と決済カードの両方を通じてオンライン決済が行われています。デジタルウォレットの利便性とキャッシュレス取引の重視が、カードやデジタルウォレットを使ったオンライン決済の普及をさらに後押しし、市場の成長を支えています。

- しかし、デジタル決済の拡大はUPIエコシステムと統合されたアプリケーションだけにとどまりません。決済カード、特にクレジットカードは、インドにおけるユーザー普及と取引量の両方で堅調な伸びを示しています。インド準備銀行(RBI)によると、ATMによる引き出し取引は、2022年3月の67万9,820件から2023年3月には82万6,490件以上に達しました。さらに、POS端末でのクレジットカード取引は、2022年3月の1億1,300万件から、2023年3月には1億4,000万件に増加しました。このデータは、過去1年間にATMを利用した現金引き出しが大幅に増加したことを裏付けています。

- 決済市場では、ウォレット、決済サービスプロバイダー(PSP)、フィンテック、ビッグテックなど、多様な利害関係者がデジタル決済プラットフォームの確立を目指してしのぎを削っています。こうした新規参入企業は、従来の銀行が提供するサービス一式を提供することはできないかもしれないが、特定のニッチに対応することに秀でており、より優れた顧客体験を、多くの場合、より競合料金で提供しています。さらに、こうした新規参入企業は銀行よりも規制が緩く、コスト面で大きな優位性を持っています。顧客を引き付け、維持するために、FinTech、ウォレット、BigTechは多くの場合、特典やキャッシュバックアプローチを活用しています。このような顧客中心のアプローチは、価格を引き下げるだけでなく、市場での競争を激化させています。

- 政府の規制支援、インド国家決済公社(NPCI)による継続的な技術進歩、拡大する決済サービスプロバイダーのネットワークによる革新的なソリューションが、人々の関心を大幅に高めました。COVID-19の大流行時には非接触型決済への需要が高まり、その動向は大流行が沈静化した後も続いており、消費者行動の長期的な変化を示しています。

- パンデミックは、実店舗の閉鎖によるオンライン購入やキャッシュレス取引の需要を高めました。その結果、消費者の購買行動はデジタルウォレットを通じた決済を選択するように変化し、これはインドの全地域におけるモバイルウォレットとインターネットサービスの成長に支えられ、インドのパンデミック期とパンデミック後の決済市場に成長機会をもたらしました。

インドの決済市場動向

POSが市場成長を牽引する見込み

- 加盟店や企業は、クレジットカードの決済の普及や、顧客のさまざまな決済嗜好に対応する必要性から、新しいPOS(販売時点情報管理)端末の導入を加速させています。しかし、QRコードベースのUPI取引へのシフトが著しいです。非接触型決済、QRコードベースの決済、BNPL(Buy Now Pay Later)オプションの出現は、POS取引の利便性と安全性を継続的に向上させ、より多くのユーザーや小売業者が決済を受け入れるためにこれらの決済端末を採用するようになりました。

- eコマースの成長により、オンラインショッピングは標準的なプラクティスとして確立され、デジタル決済が主要な取引方法となりました。このような行動は実店舗の小売業にも影響を与え、消費者は決済時にデジタルウォレットやカードを使用することを好むようになっています。インド準備銀行(RBI)によると、2023年1月の1億7,425万件の取引に対し、2024年5月にはインド全土で約2億9,800万件のPOS取引がデビットカードを通じて行われました。

- さらに、POS企業の様々な取り組みにより、インドのmPOS動向は改善傾向にあります。例えば、RapiPayはモバイルPOS(mPOS)機として機能するハイブリッドマイクロATMを設立しました。その結果、顧客はRapiPayステーションでの取引や購入において、デビットカードに加えてクレジットカードをスワイプできるようになります。

- デジタルウォレットやカードなどを使った店頭取引の人気が高まっていることが、インドの決済市場の主要な促進要因となっています。利便性、安全性、幅広い顧客層、政府の取り組みが、技術の継続的な進歩や金融包摂への注力とともに、この成長を後押ししています。PoS取引がよりシームレスで利用しやすくなるにつれて、予測期間中の市場成長はさらに促進される展望です。

小売産業が主要市場シェアを占める見込み

- 小売業の売上が増加するにつれ、取引件数も増加します。このため、デジタルウォレット、モバイル決済、POSシステムなど、効率的で安全な決済手段に対する需要が高まっています。例えば、インド小売業協会(Retailers Association of India)によると、2022年6月から2023年6月にかけて、小売産業は様々なカテゴリーで大幅な成長を遂げました。食品、食料品、靴のカテゴリーが15%増と最も高い伸びを示し、宝飾品が14%増と僅差で続きました。さらに、スポーツ用品はインド全土で13%の売上増を記録しました。

- デジタル化とキャッシュレス取引を推進するインド政府の取り組みは、消費者の現金離れを促しています。これは、小売産業におけるデジタル決済手段の採用を促進します。政府は、BHIMやUPIなどのデジタルウォレットの普及、RuPayデビットカードやUPI決済の取引手数料無料化、Bharat QRコードシステムの設置など、小売業におけるデジタル決済を促進するためのイニシアチブをいくつか開始しました。これらの取り組みにより、消費者と小売業者の双方にとって、デジタル決済がより安く、より速く、より利用しやすくなり、インドの小売産業におけるキャッシュレス取引の大幅な増加につながりました。

- さらに、インド電子情報技術省は、小売デジタル決済産業の大幅な拡大を報告しており、2017~2023年までの取引量のCAGRは50.84%を達成しました。インド準備銀行(RBI)のデータによると、小売クレジット送金、デビット送金、口座引き落とし、プリペイドの決済手段(PPI)、カードの決済が対象です。2022~2023年度、インドは1日当たり約3億6,882万件のデジタル取引を処理しました。驚くべきことに、2023年12月までに、2023~2024年度のデジタル取引件数はすでに1,000億件を超えていました。市場成長にはいくつかの要因が寄与しており、主要要因としては、決済インフラの進歩、情報通信技術の大幅な進歩、ダイナミックな規制枠組みの導入などが挙げられます。

- デジタル決済の利便性がその普及を大きく後押しし、オフラインの小売店舗でのデジタル決済オプションに対する顧客の需要が急増しました。悪政廃止に伴うATMや銀行支店での現金不足を受け、顧客の嗜好に影響された多くの加盟店がカードやQRコードによる決済に移行しました。

インドの決済産業概要

インドの決済市場は、複数の企業が存在するためセグメント化しています。しかし、Paytmのような少数の重要な参入企業が市場の成長に大きく貢献しています。さまざまな参入企業が利益を最大化しようと競争しているため、市場競争は激しいです。決済アグリゲーターも同様に、製品ラインの拡大や買収・提携といった戦略の採用など、さまざまな手段を講じて市場シェアの拡大を図っています。決済市場の主要企業には、Visa Inc.、Mastercard Inc.、Phonepe Pvt Ltd(Flipkart Internet Pvt.Ltd)、Google Pay(Google LLC)、Rupayなどがあります。

- 2024年6月:Hitachi Payment Servicesは、インド準備銀行(RBI)より、決済システム法によるオンライン決済アグリゲーターとしての最終認可を取得しました。これにより、UPI、ネットバンキング、カード、ウォレットなどの革新的で加盟店にとって使いやすい決済手段や、EMI、後払い、BNPL(Buy Now Pay Later)、リンクベース決済、加盟店向けカスタマイズ・ロイヤルティソリューションなどの付加価値サービスを包括的に提供し、デジタルソリューションとサービスのポートフォリオを強化します。

- 2024年5月、Paytm Payments Bank(PPBL)は、最近、小売POS事業をRBL銀行に、加盟店決済サービスをアクシス銀行に切り替えた後、請求書決済事業を、インドの多数のデジタル決済チャネルのバックエンドの決済システムの管理を専門とする米国の決済技術企業、Euronet Services Indiaに移管しました。

- 2024年5月、Amnex InfotechnologiesとMastercardは戦略的提携を結び、都市モビリティ産業における先進的決済ソリューションを開発。この取り組みは、交通システムの効率性と利便性を高めることを目的としています。この提携は、先進的交通ソリューションを共同開発するという両社の相互コミットメントを強調するものです。両社は、まず2つのパイロットプロジェクトを開始し、その後中東やその他の中東・アフリカにも取り組みを拡大しながら、インドの20都市でこれらのイノベーションを実施する計画です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- インドにおける決済環境の進化

- インドにおけるキャッシュレス取引の拡大に関連する主要市場動向

- COVID-19がインドの決済市場に与える影響

第5章 市場力学

- 市場促進要因

- eコマースの急成長とMコマースの台頭が決済市場を牽引する見込み

- 市場のデジタル化を促す主要小売企業と政府による支援プログラム

- UPIやBuy Now Pay Laterなどのリアルタイム決済がインドの決済市場を牽引

- 市場課題

- デジタル取引における高い失敗率

- 市場機会

- キャッシュレス社会への移行

- 新規参入企業によるイノベーションが普及を促進

- デジタル決済産業における主要規制と基準

- 主要事例と使用事例の分析

- インドの決済産業に関連する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢・所得などを網羅)

- インドにおける顧客満足度重視の高まりと世界の動向の融合に関する分析

- インドにおける現金離れと非接触決済の台頭の分析

第6章 市場セグメンテーション

- 決済モード別

- 販売時点情報管理(POS)

- カードの決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他の決済方法

- オンライン販売

- カードの決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- 販売時点情報管理(POS)

- エンドユーザー産業別

- 小売

- エンターテインメント

- 医療

- ホスピタリティ

- その他

第7章 競合情勢

- 企業プロファイル

- Visa Inc.

- Mastercard Inc.

- PhonePe Pvt Ltd(Flipkart Internet Pvt Ltd)

- Google Pay(Google LLC)

- Rupay

- Paytm(One97 Communications Limited)

- Amazon Pay(Amazon.com Inc.)

- American Express Company

- One MobiKwik Systems Limited

- Freecharge Payment Technologies Pvt. Ltd

第8章 投資分析

第9章 市場の将来展望

目次

The India Payments Market size is estimated at USD 421.50 billion in 2025, and is expected to reach USD 960.22 billion by 2030, at a CAGR of 17.9% during the forecast period (2025-2030).

Key Highlights

- Shopping for goods and services on the internet, supported by an increasing number of online shoppers in India, is among the primary drivers for the payments market in the country, with payments made online through both UPI transactions and payment cards. The convenience of digital wallets and the emphasis on cashless transactions further fuel the adoption of online payments using cards and digital wallets, supporting market growth.

- However, the expansion of digital payments extends beyond applications integrated with the UPI ecosystem. Payment cards, particularly credit cards, have demonstrated a robust increase in both user adoption and transaction volumes in India. According to the Reserve Bank of India (RBI), ATM withdrawal transactions reached over 826.49 thousand in March 2023, up from 679.82 thousand in March 2022. Furthermore, credit card transactions at point-of-sale terminals rose to 140 million in March 2023, compared to 113 million in March 2022 made via credit cards. This data underscores a significant rise in cash withdrawals via ATMs over the past year.

- The payments market has seen a surge in diverse stakeholders, including wallets, payment service providers (PSPs), FinTechs, and BigTechs, all competing to establish their digital payment platforms. While these new players may not offer the full suite of services traditional banks do, they excel in catering to specific niches, delivering enhanced customer experiences, often at more competitive rates. Furthermore, these entrants face less stringent regulations than banks, translating into significant cost advantages. To attract and retain customers, FinTechs, wallets, and BigTechs often leverage rewards and cashback approaches. This customer-centric approach has not only driven down pricing but also intensified competition in the market.

- Government regulatory support, continuous technical advancements by the National Payments Corporation of India (NPCI), and innovative solutions from an expanding network of payment service providers have significantly increased public interest. There was an increased demand for contactless payments during the COVID-19 pandemic, and the trend continued even as the pandemic receded, indicating a long-standing shift in consumer behavior.

- The pandemic raised the demand for online purchases and cashless transactions due to the closure of physical shops. It transformed consumer buying behavior to go for payment options through digital wallets, which has been supported by the growth of mobile wallets and internet services in all the regions of the country, creating a market growth opportunity for the payment market during the pandemic and post-pandemic period in India.

India Payments Market Trends

Point-of-Sale is Expected to Drive Market Growth

- Merchants and businesses are increasingly deploying new point-of-sale (PoS) terminals, driven by the growing popularity of credit card payments and the need to accommodate various customer payment preferences. However, there is a significant shift toward QR code-based UPI transactions. The emergence of contactless payments, QR code-based payments, and buy now pay later (BNPL) options continuously enhanced the convenience and security of PoS transactions, attracting more users and retailers to adopt these payment terminals to accept payments.

- The growth of e-commerce has established online shopping as a standard practice, with digital payments becoming the primary transaction method. This behavior has also influenced physical retail, where consumers increasingly prefer using digital wallets or cards at the time of payment. According to the Reserve Bank of India (RBI), in May 2024, nearly 298 million point-of-sale transactions were made through debit cards across India, compared to 174.25 million transactions in January 2023.

- Moreover, the mPOS trends in India are improving because of various initiatives of POS companies. For instance, RapiPay established hybrid micro-ATMs that can function as mobile point-of-sale (mPOS) machines. As a result, customers will be able to swipe credit cards in addition to debit cards for any transaction or purchase at a RapiPay station.

- The rising popularity of point-of-sale transactions using digital wallets, cards, and other modes is a key driver of the Indian payments market. Convenience, security, wider customer reach, and government initiatives are fueling this growth, along with continuous advancements in technology and a focus on financial inclusion. As PoS transactions become more seamless and accessible, they are poised to further drive market growth over the forecast period.

Retail Industry Expected to Hold Major Market Share

- As retail sales rise, there is a corresponding increase in the number of transactions. This translates to a higher demand for efficient and secure payment methods, including digital wallets, mobile payments, and point-of-sale (POS) systems. For instance, according to the Retailers Association of India, from June 2022 to June 2023, the retail industry experienced substantial growth across various categories. The food, grocery, and footwear categories experienced the highest sales growth at 15%, while jewelry followed closely with a 14% increase in sales. Furthermore, sports goods witnessed a 13% growth in sales across India.

- The Government of India's initiatives to promote digitalization and cashless transactions are encouraging consumers to move away from cash. This fuels the adoption of digital payment methods within the retail industry. The government launched several initiatives to fuel digital payments in retail, including promoting digital wallets like BHIM and UPI, offering zero-transaction charges for RuPay debit cards and UPI payments, and setting up the Bharat QR code systems. These initiatives have made digital payments cheaper, faster, and more accessible for both consumers and retailers, leading to a significant increase in cashless transactions within India's retail industry.

- Furthermore, the Indian Ministry of Electronics and Information Technology has reported a significant expansion in the retail digital payment industry, which achieved a compound annual growth rate (CAGR) of 50.84% in transaction volume from 2017 to 2023. According to data from the Reserve Bank of India (RBI), it covers retail credit transfers, debit transfers, direct debits, prepaid payment instruments (PPI), and card payments. During the FY 2022-2023, India processed approximately 368.82 million digital transactions daily. Remarkably, by December 2023, the country had already exceeded 100 billion digital transactions for the FY 2023-2024. Several factors aided in market growth, with key contributors being advancements in payment infrastructure, significant progress in information and communications technology, and the implementation of a dynamic regulatory framework.

- The convenience of digital payments has significantly driven their adoption, leading to a surge in customer demand for digital transaction options at offline retail outlets. In response to the cash shortages at ATMs and bank branches following demonetization, many merchants, influenced by their customers' preferences, transitioned to accepting card and QR code payments.

India Payments Industry Overview

The Indian payments market is fragmented due to the presence of several companies. However, a few significant market players, like Paytm, have contributed considerably to the market's growth. There is intense market competition as different players compete to maximize their profits. Payment aggregators are likewise attempting to expand their market share by implementing various measures, including expanding their product line and adopting strategies like acquisitions and partnerships. Some major companies in the payments market are Visa Inc., Mastercard Inc., Phonepe Pvt Ltd (Flipkart Internet Pvt. Ltd), Google Pay (Google LLC), and Rupay.

- June 2024: Hitachi Payment Services obtained final authorization from the Reserve Bank of India (RBI) to operate as an online payment aggregator under the Payments and Settlement Systems Act. This approval allows the company to enhance its digital solutions and services portfolio, offering a comprehensive array of innovative and merchant-friendly payment options, including UPI, net banking, cards, and wallets, along with value-added services such as EMI, pay later, buy now pay later (BNPL), link-based payments, and customized loyalty solutions for merchants.

- May 2024: Paytm Payments Bank (PPBL) moved its bill payment operations to Euronet Services India, a US-based payment technology firm that specializes in managing backend settlement systems for numerous digital payment channels in India after recently switching its retail point-of-sale business to RBL Bank and merchant payment settlement services to Axis Bank.

- May 2024: Amnex Infotechnologies and Mastercard formed a strategic collaboration to develop advanced payment acceptance solutions within the urban mobility industry. This initiative aims to enhance the efficiency and convenience of transit systems. The partnership highlights the mutual commitment of both companies to co-create advanced transit solutions. They plan to implement these innovations across 20 cities in India, beginning with two pilot projects and subsequently extending their efforts to the Middle East and other regions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the Payments Landscape in India

- 4.5 Key Market Trends Pertaining to the Growth of Cashless Transactions in India

- 4.6 Impact of COVID-19 on the Payments Market in India

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Robust Growth of E-commerce and Rise of M-commerce is Expected to Drive the Payments Market

- 5.1.2 Enablement Programs by Key Retailers and Government Encouraging Digitization of the Market

- 5.1.3 Real-time Payments, such as UPI and Buy Now Pay Later to Drive the Indian Payments Market

- 5.2 Market Challenges

- 5.2.1 Higher Rate of Failure in Digital Transactions

- 5.3 Market Opportunities

- 5.3.1 Move Toward Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of Major Case Studies and Use-cases

- 5.6 Analysis of Key Demographic Trends and Patterns Related to the Payments Industry in India (Coverage to Include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income, etc.)

- 5.7 Analysis of the Increasing Emphasis on Customer Satisfaction and Convergence of Global Trends in India

- 5.8 Analysis of Cash Displacement and Rise of Contactless Payment Modes in India

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (Includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (Includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Other Modes of Payment

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (Includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (Includes Mobile Wallets)

- 6.1.2.3 Others (Includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Visa Inc.

- 7.1.2 Mastercard Inc.

- 7.1.3 PhonePe Pvt Ltd (Flipkart Internet Pvt Ltd)

- 7.1.4 Google Pay (Google LLC)

- 7.1.5 Rupay

- 7.1.6 Paytm (One97 Communications Limited)

- 7.1.7 Amazon Pay (Amazon.com Inc.)

- 7.1.8 American Express Company

- 7.1.9 One MobiKwik Systems Limited

- 7.1.10 Freecharge Payment Technologies Pvt. Ltd

8 Investment Analysis

9 Future Outlook of the Market

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日