EVバッテリー製造装置:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636538

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

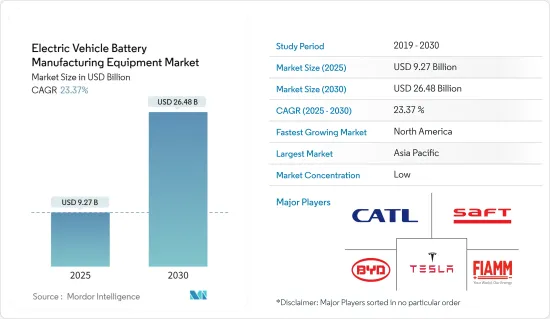

EVバッテリー製造装置の市場規模は、2025年に92億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは23.37%で、2030年には264億8,000万米ドルに達すると予測されます。

主なハイライト

- 長期的には、電気自動車の普及と原料電池材料のコスト低下が市場を牽引すると予想されます。

- 一方、内燃機関自動車への長期的な依存が電気自動車への急速な移行を妨げ、市場の成長を抑制する可能性もあります。

- しかし、高容量化と低放電率化の技術進歩が進むことで、電池装置の実現性と効率性が高まり、電気自動車用電池製造装置市場に巨大な機会が生まれると予想されます。

- アジア太平洋が市場を独占しており、その成長は、インド、中国、オーストラリアなどの国々における投資の増加と政府政策の促進につながっています。

EVバッテリー製造装置市場の動向

市場を独占する電気自動車の急速な普及

- ガソリンや天然ガスのコスト変動が激しくなり、各国で排ガス規制の要求が高まっていることから、従来の自動車から電気自動車(EV)に注目が移っています。電気自動車は効率が高く、電気代が安いため、ガソリンやディーゼルを満タンにして移動するよりも電気自動車を充電した方が安く済みます。再生可能エネルギーを使用すれば、電気自動車はより環境に優しいものになります。

- さらに、電気自動車の需要が高まるにつれて、自動車メーカー各社は、あらゆる自動車セグメント向けに、さまざまなタイプやデザインの電気自動車を設計し、販売台数を伸ばしています。このような自動車設計のカスタマイズは、自動車メーカーの需要を満たす電池製造に大きな成長機会をもたらします。

- 2023年10月、BMWはミュンヘン近郊に新しいバッテリー・セル・パイロット工場を設立し、「ローカル・フォー・ローカル」バッテリー・サプライ・チェーンおよび生産戦略を実現しました。BMWセル製造コンピテンス・センター(CMCC)は円筒型セルを製造する予定で、これにより同社のバッテリー生産と供給の効率、品質、安定性が高まると期待されています。

- 近年の電気自動車の流入は、予測期間中のバッテリー製造装置の需要を促進すると予想されます。国際エネルギー機関(IEA)によると、2023年の世界の電気自動車の総販売台数は1,380万台で、前年の1,020万台から増加しました。

- 2030年までに、いくつかの国が電気自動車のシェアを拡大することを決定しています。例えば、中国などは2030年までに販売される自動車の40%を電気自動車にすることを目指しています。EV人口の増加に伴い、バッテリー需要も大きく伸びることが予想されます。国際エネルギー機関(IEA)によると、2035年までにEV用バッテリーの需要は2023年比で7倍に増加すると予想されています。

- こうしたシナリオを考慮すると、自動車産業は予測期間中に最も急成長するセグメントとなる見込みです。

アジア太平洋地域は市場の著しい成長が期待される

- アジア太平洋地域では、環境問題や悪化の一途をたどる状況を改善する技術に対する人々の意識が高まっているため、EVバッテリー製造装置市場が常に上昇しています。アジア太平洋地域は人口が多く、経済が急成長しているため、中国、インド、ASEAN諸国などの国が市場を牽引しており、アジア太平洋地域のバッテリー需要は着実に成長すると予想されます。

- 中国は、電気自動車産業が盛んで、サプライチェーン全体で業界をリードするプレーヤーが存在し、経済が急成長していることから、バッテリー製造装置市場を独占しています。この地域は、世界のリチウムイオン埋蔵量の大半を占めています。国際エネルギー機関の発表によると、2023年の中国における電気自動車の販売台数は、前年の590万台から約810万台に増加します。これはアジア太平洋で最も高いです。

- アジア太平洋における電気自動車用バッテリー製造ギガファクターの成長は、今後数年間、その製造装置市場を押し上げると予想されます。例えば、2023年1月、リチャージ・インダストリーズ社は、2024年までに年間2GWh、2026年までに6GWhの電気自動車用電池をオーストラリアのジーロング地域に建設すると発表しました。3億米ドル相当のこの巨大工場は、同国の電気電池サプライ・バリュー・チェーンを改善することが期待されています。

- 電気自動車の開発を促進する政府の目標やイニシアチブは、アジア太平洋地域の市場成長をさらに促進する可能性があります。例えばインドでは、2030年までに電気自動車(EV)が自家用車販売の30%、商用車販売の70%、二輪車・三輪車販売の80%を占めることを政府は目指しています。

- 従って、アジア太平洋地域は、EVバッテリー製造装置市場における生産の増加、技術の進歩、政府の支援政策により、予測期間中に市場を独占すると予想されます。

EVバッテリー製造装置産業の概要

電気自動車用電池製造装置市場は断片化されており、複数のプレーヤーが存在します。主なプレーヤー(順不同)には、NEC、Duerr AG、日立製作所、Schuler AG、Buhler Holding AGなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 電池原材料コストの低下

- 抑制要因

- 内燃機関自動車への長期依存

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- プロセス別

- 混合

- コーティング

- カレンダー

- スリット・電極加工

- その他のプロセス

- バッテリー別

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- マレーシア

- タイ

- インドネシア

- ベトナム

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- ナイジェリア

- カタール

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- NEC Corporation

- Duerr AG

- Hitachi Ltd

- Schuler AG

- Buhler Holding AG

- Manz AG

- Sovema Group S.p.A

- Komatsu NTC Ltd

- KROENERT GmbH & Co. KG.

- List of Other Prominent Companies

- 市場ランキング分析

第7章 市場機会と今後の動向

- 様々な技術における技術進歩の高まり

目次

Product Code: 50003971

The Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 9.27 billion in 2025, and is expected to reach USD 26.48 billion by 2030, at a CAGR of 23.37% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing adoption of electric vehicles and the decline in the cost of raw battery materials are expected to drive the market.

- On the other hand, the long-term dependency on internal combustion engine vehicles could hinder the rapid transition to electric vehicles, which may restrain the growth of the market.

- However, the growing technological advancements in higher capacity and low discharge rates are expected to make battery equipment more feasible and efficient and create enormous opportunities for the electric vehicle battery manufacturing equipment market.

- Asia-Pacific dominates the market, and its growth will be linked to rising investments and conducive government policies in countries such as India, China, and Australia.

Electric Vehicle Battery Manufacturing Equipment Market Trends

Rapid Adoption of Electric Vehicles to Dominate the Market

- The increasing cost fluctuations of gasoline and natural gas and the growing demand for emission controls in various countries have shifted the focus from conventional vehicles to electric vehicles (EVs). Electric vehicles are more efficient, which, combined with the lower cost of electricity, makes charging an electric vehicle cheaper than filling up with petrol or diesel for your travel needs. Using renewable energy sources can make electric vehicles more eco-friendly.

- Moreover, as the demand for electric vehicles increases, automobile manufacturing companies are designing electric vehicles for all car segments in various types and designs to increase their sales. This customization in automobile design provides a significant growth opportunity for battery manufacturing to meet automobile manufacturers' demands.

- In October 2023, BMW established its new battery cell pilot plant near Munich to fulfill its 'local for local' battery supply chain and production strategy. BMW Cell Manufacturing Competence Center (CMCC) will manufacture cylindrical cells, which is expected to boost the company's efficiency, quality, and stability in battery production and supply.

- The influx of electric vehicles in recent years is expected to propel the demand for battery manufacturing equipment during the forecast period. According to the International Energy Agency (IEA), the total sales of electric vehicles worldwide were 13.8 million in 2023, an increase from 10.2 million the previous year.

- By 2030, several countries have decided to increase the share of electric vehicles. For instance, countries like China aim to have 40% of vehicles sold by 2030 to be electric. With the growth in the EV population, battery demand is expected to witness significant growth. According to the International Energy Agency, by 2035, EV battery demand is expected to increase by seven times compared to 2023.

- Considering such a scenario, the automotive industry is expected to be the fastest-growing segment during the forecast period.

Asia-Pacific is Expected to Witness Significant Growth in the Market

- The electric vehicle battery manufacturing equipment market is constantly rising in Asia-Pacific due to the rising public awareness of environmental issues and techniques to improve constantly deteriorating conditions. Due to the region's large population and fast-growing economy, the demand for batteries in Asia-Pacific is expected to grow steadily, with countries such as China, India, and the ASEAN countries driving the market.

- China dominates the battery manufacturing equipment market with a significant electric car industry, leading industry players across the supply chain, and a rapidly rising economy. The region has the majority of the world's lithium-ion reserves. As per the International Energy Agency, the sales of electric cars in China in 2023 were about 8.1 million, from 5.9 million in the previous year. This appeared to be the highest in Asia-Pacific.

- The growth of electric vehicle battery manufacturing gigafactors in Asia-Pacific is expected to push its manufacturing equipment market in the coming years. For instance, in January 2023, the Recharge Industries firm noted that it would construct close to 2 GWh of annual electric vehicle battery production by 2024 and 6 GWh by 2026 in Australia's Geelong region. The gigagactory worth USD 300 million is expected to improve the country's electric battery supply-value chain.

- Government targets and initiatives to expedite the development of electric vehicles could further drive market growth in Asia-Pacific. For instance, in India, by 2030, the government aims for electric vehicles (EVs) to make up 30% of private car sales, 70% of commercial vehicle sales, and 80% of sales of two- and three-wheelers.

- Hence, Asia-Pacific is expected to dominate the market during the forecast period due to increased production, technological advancements, and supportive government policies in the electric vehicle battery equipment manufacturing market.

Electric Vehicle Battery Manufacturing Equipment Industry Overview

The electric vehicle battery manufacturing equipment market is fragmented, with several players. Some of the major players (not in particular order) include NEC Corporation, Duerr AG, Hitachi Ltd, Schuler AG, and Buhler Holding AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing adoption of electric vehicles

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Long-term dependency on internal combustion engine vehicles

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendering

- 5.1.4 Slitting and electrode making

- 5.1.5 Other Processes

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Spain

- 5.3.2.3 NORDIC Countries

- 5.3.2.4 Turkey

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Thailand

- 5.3.3.5 Indonesia

- 5.3.3.6 Vietnam

- 5.3.3.7 South Korea

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 NEC Corporation

- 6.3.2 Duerr AG

- 6.3.3 Hitachi Ltd

- 6.3.4 Schuler AG

- 6.3.5 Buhler Holding AG

- 6.3.6 Manz AG

- 6.3.7 Sovema Group S.p.A

- 6.3.8 Komatsu NTC Ltd

- 6.3.9 KROENERT GmbH & Co. KG.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing technological advancements in various technologies

EVバッテリー製造装置:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日