アジア太平洋地域のEVバッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia Pacific Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636471

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

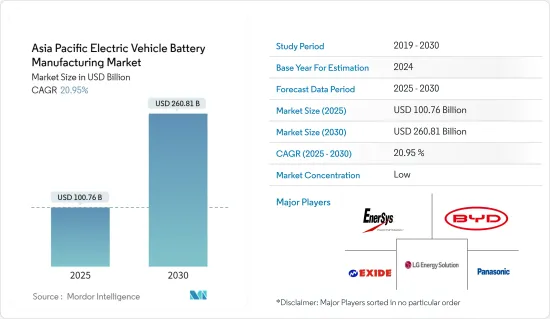

アジア太平洋地域のEVバッテリー製造の市場規模は、2025年に1,007億6,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは20.95%で、2030年には2,608億1,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、電池生産能力増強のための投資増加と電池原料コストの低下が、予測期間中の電気自動車用電池製造需要を牽引すると予想されます。

- 一方、信頼性の高さから従来型自動車の販売が増加しており、予測期間中は電気自動車用電池市場にマイナスの影響を与えると予想されます。

- とはいえ、生産能力の拡大、技術進歩の強化、コスト削減といった電気自動車に関する長期的な野心的目標は、近い将来、EVバッテリー製造市場に大きなチャンスをもたらすと予想されます。

- 予測期間中、アジア太平洋のEVバッテリー製造市場では、電気自動車の普及台数の増加により、インドが最も急成長している地域です。

アジア太平洋地域のEVバッテリー製造市場動向

リチウムイオン電池タイプが市場を独占

- リチウムイオン(Li-ion)電池は電気自動車(EV)市場に革命をもたらし、電池製造の技術革新を促進しました。高エネルギー密度、長サイクル寿命、急速充電といったリチウムイオン電池の主な特性により、今日のEVにはリチウムイオン電池が選ばれています。

- さらに、リチウムイオン二次電池は容量重量比が優れているため、他の技術を凌駕しています。リチウムイオン二次電池は代替品よりも高価な傾向があるが、市場の大手企業は研究開発投資を増やし、生産を拡大しているため、競争が激化し、価格引き下げにつながっています。

- EVとバッテリーエネルギー貯蔵システム(BESS)用のバッテリーパックの平均価格が上昇しているにもかかわらず、2023年のバッテリー価格は139米ドル/kWhと、13%の大幅下落が見られました。予測によると、この下落基調は今後も続き、2025年には113米ドル/kWhに達し、2030年にはさらに80米ドル/kWhまで下落すると予想されます。

- アジア太平洋地域では、各国政府が電気自動車(EV)の普及を促進し、リチウムイオン電池の生産拡大を促すための政策やインセンティブを実施しています。これらの政府は、研究開発を優先させることで、コバルトのような高価で希少な材料の代用品として、費用対効果が高く入手しやすい材料を特定しようとしています。この戦略は、製造コストを削減するだけでなく、より持続可能なサプライ・チェーンも確保します。

- 例えば、中国は2024年5月、ハイブリッドモデルを含む電気自動車(EV)用の次世代バッテリー技術の開拓に約60億元(8億4,500万米ドル)を投資することになっています。最先端技術であるASSBは、従来のリチウムイオン電池(LIB)を固体部品で強化します。従来のバッテリーに比べて発火や爆発の危険性が低く、エネルギー密度にも優れています。このような技術革新は、今後数年間で先進的なリチウムイオン電池の需要を押し上げ、同地域のEV用電池製造にプラスの影響を与える見通しです。

- さらに、リチウムイオン電池の需要急増は、ギガファクトリーと呼ばれる大規模生産施設の設立を後押ししています。これらの専門施設は、バッテリーセルを大量生産するように設計されており、電気自動車(EV)からの高まる需要を確実に満たすことができます。この地域の主要企業は、リチウムイオン電池の製造を強化するために複数のプロジェクトを立ち上げています。

- 例えば、BMWは2024年2月、タイのラヨーンに新しいバッテリー工場を建設する計画を発表しました。同社は、タイをアジア太平洋地域におけるEV用バッテリーの主要輸出拠点とし、同地域のリチウムイオン・バッテリー供給をさらに強化することを構想しています。このような取り組みにより、同国の電池生産は今後数年で加速することになります。

- その結果、こうした取り組みがリチウムイオン電池の生産を拡大し、予測期間中にEV用電池の生産能力を大幅に高めることになります。

著しい成長を遂げるインド

- インドの電気自動車(EV)バッテリー製造市場は、同国がより環境に優しいモビリティ・ソリューションを採用するにつれて急速に拡大しています。この成長の原動力となっているのは、政府のイニシアティブ、電気自動車に対する需要の急増、国内外のプレーヤーによる多額の投資です。

- インドがクリーンエネルギーに軸足を移す中、電気自動車への重点投資は多くの企業にとって最重要課題となっています。この地域でのEV販売は急増しています。例えば、国際エネルギー機関(IEA)の報告によると、2023年の電気自動車販売台数は8万2,000台に達し、2022年から70.8%増、2019年からは119倍という驚異的な伸びを示しました。政府が最近、複数のプロジェクトやイニシアチブを開始したことで、EV販売はさらに大きく成長する態勢が整っています。

- インドでは、国内企業や国際企業の双方から、EVバッテリー製造への投資が相次いでいます。これらの投資は、国の電気自動車インフラを強化し、化石燃料への依存を減らし、持続可能な輸送を支持することを目的としています。政府の支援政策と奨励策に後押しされ、インドは世界のEV事情において傑出した地位を築きつつあります。

- 例えば、2024年7月、オラ・エレクトリックは、インドのタミル・ナードゥ州にあるギガファクトリーの第1期に1億米ドルを投資することを発表しました。この施設では、国産のリチウムイオン電池を生産します。同社は来年初めまでに、電気自動車用のバッテリーセルを現在の韓国や中国からの輸入から自社製に切り替える計画です。このような動きは、今後数年間で全国的にバッテリー生産を強化することになります。

- さらに、インド政府は電気自動車(EV)の普及を促進し、現地でのバッテリー製造を活性化させるためのイニシアチブを展開しています。これらの施策には、EV購入者への補助金、メーカーへの減税、充電インフラへの投資強化などが含まれます。

- その一例として、インド政府は2023年に、2030年までに自家用車販売の30%、商用車の70%、二輪車と三輪車の80%をEVにするという野心的な目標を掲げました。さらに政府は、1kWhあたり10,000インドルピー(120米ドル)から15,000インドルピー(180米ドル)までの補助金優遇措置を提供しています。このような取り組みは、EVの生産と需要を押し上げるだけでなく、予測期間中に同地域でのバッテリー製造の必要性を高める。

- その結果、これらのプロジェクトやイニシアティブはEV需要を強化し、ひいては今後数年間のEVバッテリー製造のニーズを大幅に高めることになります。

アジア太平洋地域のEVバッテリー製造業界の概要

アジア太平洋地域のEVバッテリー製造市場は半分断されています。主要企業(順不同)には、BYD Company Ltd、LG Energy Solution、Exide Industries Ltd、EnerSys、Panasonic Holdings Corporationなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電池生産能力増強のための投資

- 電池原材料コストの低下

- 抑制要因

- 従来型自動車の高い信頼性

- 促進要因

- サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリー別

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- その他

- 電池形状別

- 角型

- 袋型

- 円筒形

- 車両別

- 乗用車

- 商用車

- その他

- 推進別

- バッテリー電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

- 地域別

- 中国

- インド

- オーストラリア

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd

- Panasonic Corporation

- LG Energy Solution

- EnerSys

- Exide Industries

- Contemporary Amperex Technology Co. Limited

- Tianjin Lishen Battery Joint-Stock Co., Ltd.

- Samsung SDI

- SK Innovation Co., Ltd.

- Envision AESC

- Gotion High tech Co Ltd

- その他の有名企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

目次

Product Code: 50003738

The Asia Pacific Electric Vehicle Battery Manufacturing Market size is estimated at USD 100.76 billion in 2025, and is expected to reach USD 260.81 billion by 2030, at a CAGR of 20.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising investments to enhance the battery production capacity and the decline in the cost of battery raw materials are expected to drive the demand for electric vehicle battery manufacturing during the forecast period.

- On the other hand, increasing sales of conventional vehicles due to their high reliability is expected to have a negative impact on the EV battery market during the forecast period.

- Nevertheless, the long-term ambitious targets for electric vehicles, such as scaling up production capacity, enhancing technological advancements, and reducing costs, are expected to create significant opportunities for the electric vehicle battery manufacturing market in the near future.

- India is the fastest-growing region in Asia Pacific's electric vehicle battery manufacturing market during the forecast period due to the rising electric vehicle adoption.

Asia Pacific Electric Vehicle Battery Manufacturing Market Trends

Lithium-Ion Battery Type Dominate the Market

- Lithium-ion (Li-ion) batteries have revolutionized the electric vehicle (EV) market, driving innovations in battery production. Their key attributes, such as high energy density, long cycle life, and swift charging, make them the preferred choice for today's EVs.

- Moreover, lithium-ion rechargeable batteries surpass other technologies due to their excellent capacity-to-weight ratio. Although they tend to be more expensive than alternatives, major players in the market are boosting R&D investments and ramping up production, heightening competition and leading to price reductions.

- Despite rising average battery pack prices for EVs and battery energy storage systems (BESS), 2023 witnessed a significant drop in battery prices to USD 139/kWh, a 13% decline. Projections suggest this downward trajectory will persist, with prices anticipated to reach USD 113/kWh by 2025 and further plummet to USD 80/kWh by 2030, driven by relentless technological and manufacturing progress.

- In the Asia Pacific region, governments are implementing policies and incentives to promote electric vehicle (EV) adoption and stimulate Lithium-ion battery production growth. By prioritizing research and development, these governments seek to pinpoint cost-effective and readily available materials as substitutes for more expensive and scarce ones, such as cobalt. This strategy not only curtails manufacturing costs but also ensures a more sustainable supply chain.

- For example, in May 2024, China is set to invest approximately 6 billion yuan (USD 845 million) into pioneering next-generation battery technology for electric vehicles (EVs), encompassing hybrid models. ASSBs, a cutting-edge technology, enhance traditional lithium-ion batteries (LIBs) with solid components. They boast a reduced risk of fire or explosion compared to conventional batteries and offer superior energy density. Such innovations are poised to boost the demand for advanced lithium-ion batteries in the coming years, positively influencing EV battery manufacturing in the region.

- Furthermore, the surging demand for Li-ion batteries has catalyzed the establishment of large-scale production facilities, dubbed Gigafactories. These specialized facilities are engineered to produce battery cells en masse, ensuring they meet the escalating demand from electric vehicles (EVs). Major companies in the region are launching multiple projects to strengthen their lithium-ion battery manufacturing, anticipating a notable uptick in EV battery demand soon.

- For instance, in February 2024, BMW unveiled plans for a new battery factory in Rayong, Thailand, aiming to bolster the nation's battery supply chains. The company envisions Thailand as its primary export hub for EV batteries throughout the Asia Pacific, further strengthening the region's lithium-ion battery supply. Such initiatives are set to accelerate the country's battery production in the upcoming years.

- Consequently, these endeavors are poised to amplify lithium-ion battery production and substantially boost EV battery manufacturing capacity in the forecast period.

India to Witness Significant Growth

- India's electric vehicle (EV) battery manufacturing market is rapidly expanding as the nation embraces greener mobility solutions. This growth is fueled by government initiatives, a surging demand for electric vehicles, and substantial investments from both domestic and international players.

- As India pivots towards clean energy, the emphasis on electric vehicles has become paramount for numerous companies. EV sales in the region have skyrocketed. For instance, the International Energy Agency (IEA) reported that in 2023, electric vehicle sales reached 82,000 units, marking a 70.8% increase from 2022 and a staggering 119-fold jump since 2019. With the government recently launching multiple projects and initiatives, EV sales are poised for further significant growth.

- India has seen a wave of investments in EV battery manufacturing, both from domestic entities and international firms. These investments aim to strengthen the nation's electric vehicle infrastructure, lessen reliance on fossil fuels, and champion sustainable transportation. Bolstered by supportive government policies and incentives, India is carving out a prominent position in the global EV landscape.

- For example, in July 2024, Ola Electric unveiled a USD 100 million investment for the first phase of its gigafactory in Tamil Nadu, India. This facility will produce indigenous lithium-ion batteries. The company plans to transition to its battery cells for its electric vehicles by early next year, moving away from current imports from Korea and China. Such moves are set to ramp up battery production nationwide in the coming years.

- Additionally, the Indian government has rolled out initiatives to promote electric vehicle (EV) adoption and stimulate local battery manufacturing. These measures encompass subsidies for EV purchasers, tax breaks for manufacturers, and bolstered investments in charging infrastructure.

- As an illustration, the Indian government, in 2023, set ambitious targets: by 2030, they aim for EVs to constitute 30% of private car sales, 70% of commercial vehicles, and 80% of two and three-wheelers. Furthermore, the government is offering subsidy incentives ranging from INR 10,000 per kWh (USD 120) to INR 15,000 per kWh (USD 180). Such initiatives are poised to not only boost EV production and demand but also amplify the need for battery manufacturing in the region during the forecast period.

- Consequently, these projects and initiatives are set to bolster EV demand and, in turn, significantly elevate the need for EV battery manufacturing in the coming years.

Asia Pacific Electric Vehicle Battery Manufacturing Industry Overview

Asia Pacific's electric vehicle battery manufacturing market is semi-fragmented. Some of the key players (not in particular order) are BYD Company Ltd, LG Energy Solution, Exide Industries Ltd, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High reliability on Conventional Vehicle

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Australia

- 5.5.4 Malaysia

- 5.5.5 Thailand

- 5.5.6 Indonesia

- 5.5.7 Vietnam

- 5.5.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Panasonic Corporation

- 6.3.3 LG Energy Solution

- 6.3.4 EnerSys

- 6.3.5 Exide Industries

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Tianjin Lishen Battery Joint-Stock Co., Ltd.

- 6.3.8 Samsung SDI

- 6.3.9 SK Innovation Co., Ltd.

- 6.3.10 Envision AESC

- 6.3.11 Gotion High tech Co Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

アジア太平洋地域のEVバッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日