ASEAN諸国のEV用バッテリー製造装置:市場シェア分析、産業動向、成長予測(2025年~2030年)

ASEAN Countries Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636439

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

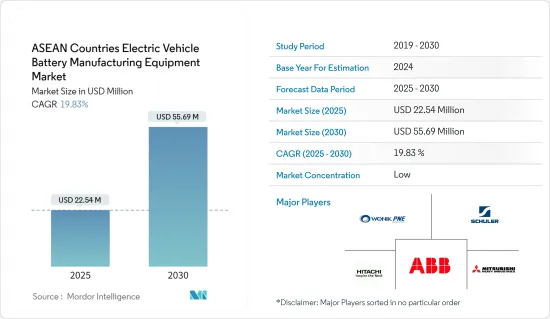

ASEAN諸国のEV用バッテリー製造装置の市場規模は、2025年に2,254万米ドルと推定され、予測期間(2025-2030年)のCAGRは19.83%で、2030年には5,569万米ドルに達すると予測されます。

主なハイライト

- 中期的には、電池製造に向けた政府の政策や投資、電池原料(特にリチウムイオン)のコスト低下が予測期間の市場を牽引するとみられます。

- 一方、初期投資コストの高さが今後の市場の足かせになると予想されます。

- とはいえ、これらの国々では電気自動車の長期的な野心的目標が掲げられており、予測期間中に大きなビジネスチャンスが生まれると予想されます。

- タイは、同国におけるEV用バッテリー製造への投資の増加により、大きく成長すると予想されます。

ASEAN諸国のEV用バッテリー製造装置市場動向

リチウムイオンバッテリーセグメントが大きく成長する見込み

- リチウムイオンバッテリー製造装置には、リチウムイオンバッテリーの製造に特化した専用の機械や工具が含まれます。近年、ASEAN諸国では、電気自動車(EV)用のリチウムイオンバッテリーの生産が急増しています。これは、EV需要の増加、政府の支援政策、世界・サプライ・チェーンにおける同地域の極めて重要な役割が拍車をかけています。このような製造の増加に伴い、リチウムイオンバッテリー製造装置に対するニーズも高まっています。

- さらに、国内製造設備の進歩は、これらの国々でリチウムイオンバッテリーの価格を引き下げる上で重要な役割を果たしています。EV需要の拡大に伴い、規模の経済が生産コストの削減につながった。その結果、リチウムイオンバッテリー価格の下落に伴い、企業はEV用電池生産への投資を拡大しており、同地域における関連製造装置の需要をさらに促進しています。

- 2023年のリチウムイオンバッテリーパック価格は前年比14%下落し、139米ドル/kWhに落ち着いた。この価格下落にとどまらず、タイ、インドネシア、ベトナム、マレーシアのような国々では、個人用・商用EVの導入が急増しています。この勢いは、輸入への依存を減らし、国内のEV部門を強化することを目的として、リチウムイオンバッテリーの国内生産に拍車をかけ、電池製造装置の需要を増幅させています。

- 例えば、中国の著名な世界的リチウム電池メーカーであるEVEエナジー社は、2023年8月、マレーシアのケダ州クリムに4億2,200万米ドルを初期投資して新工場を着工しました。このような戦略的投資により、EV用リチウムイオンバッテリーの生産が拡大し、製造装置の需要も高まっています。

- 価格低下とEV用リチウムイオンバッテリー生産への投資の急増を考えると、この分野は今後数年でかなりのシェアを占めるようになると思われます。

著しい成長が期待されるタイ

- タイの電気自動車(EV)用リチウムイオンバッテリー製造装置市場は、EV用リチウムイオンバッテリーの生産に有利な環境を背景に、大幅な成長が見込まれています。政府の後押しもあり、タイはEV生産の地域的なハブとして浮上しています。政府は、税制優遇措置や補助金でEVメーカーや電池メーカーを誘致し、2030年までに自動車生産台数の30%をEVにするという野心的な目標を掲げています。

- さらに、特に中国の電池メーカーがタイでEV用電池の新工場に熱心に投資しています。こうした投資の急増は、同国におけるEV用電池の生産に不可欠な設備の需要を押し上げることになります。

- 例えば、中国の著名な電池メーカーであるSVOLTエナジーは2024年3月、タイのチョンブリ県に位置するシーラチャの最新鋭施設でEV用電池パックの量産を開始しました。この施設は、年間約6万個のモジュールとパックの生産能力を備えています。

- タイでは電気自動車の普及が加速しており、企業は現地製造拠点への投資を拡大しています。タイ自動車研究所のデータはこの動向を浮き彫りにしています。2023年、タイの電気自動車登録台数は17万2,540台に急増し、前年の8万4,570台から顕著に増加しました。このようなEV普及の大幅な増加は、EV製造装置のニーズの拡大を裏付けています。

- タイでは、タイランド4.0や東部経済回廊(EEC)といった政府のイニシアチブにより、EV用バッテリー製造装置の見通しは楽観的なままです。これらのイニシアチブは、減税や規制の簡素化など魅力的なインセンティブを提供することで、タイをEVやバッテリーを含むハイテク分野における地域のフロントランナーとしての地位に押し上げることを目的としています。

- 政府の揺るぎない支援とEVの加速度的な普及を考えると、タイは今後数年で顕著な成長を遂げると思われます。

ASEAN諸国のEV用バッテリー製造装置産業の概要

ASEAN諸国のEV用バッテリー製造装置市場は半分断されています。同市場の主要企業(順不同)には、WONIK PNE、Schuler AG、日立製作所、ABB Ltd.、三菱重工業などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電池製造に向けた政府の政策と投資

- 電池原材料コストの低下

- 抑制要因

- 初期投資コストの高さ

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- プロセス別

- 混合

- コーティング

- カレンダー

- スリット・電極加工

- その他のプロセス

- バッテリー別

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- その他のバッテリー

- 地域別

- ASEAN諸国

- インドネシア

- マレーシア

- フィリピン

- シンガポール

- タイ

- ベトナム

- その他のASEAN諸国

- ASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- WONIK PNE CO., LTD.

- Schuler AG

- Hitachi Ltd

- ABB Ltd.

- Mitsubishi Heavy Industries, Ltd

- Sovema Group

- Daiichi Jitsugyo Thailand Co Ltd

- Yokogawa India Ltd.

- その他の有名企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

目次

Product Code: 50003706

The ASEAN Countries Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 22.54 million in 2025, and is expected to reach USD 55.69 million by 2030, at a CAGR of 19.83% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, government policies and investments towards battery manufacturing, and a decline in the cost of battery raw materials, especially lithium-ion, are expected to drive the market in the forecast period.

- On the other hand, high initial investment costs are expected to hamper the market in the future.

- Nevertheless, long-term ambitious targets for electric vehicles in these countries are expected to create a significant opportunity in the forecast period.

- Thailand is expected to grow significantly owing to the increasing investment in EV battery manufacturing in the country.

ASEAN Countries Electric Vehicle Battery Manufacturing Equipment Market Trends

Lithium-ion Battery Segment is Expected to Grow Significantly

- Lithium-ion battery manufacturing equipment includes specialized machines and tools tailored for producing lithium-ion batteries. In recent years, ASEAN countries have seen a surge in lithium-ion battery production for electric vehicles (EVs), spurred by rising EV demand, supportive government policies, and the region's pivotal role in global supply chains. With this uptick in manufacturing, the need for lithium-ion battery production equipment is set to rise.

- Moreover, advancements in domestic manufacturing equipment have played a crucial role in driving down lithium-ion battery prices across these nations. As EV demand escalates, achieving economies of scale has led to reduced production costs. Consequently, with falling lithium-ion battery prices, companies are ramping up investments in EV battery production, further fueling the demand for associated manufacturing equipment in the region.

- In 2023, lithium-ion battery pack prices plummeted by 14% from the prior year, settling at USD139/kWh. Beyond this price dip, countries like Thailand, Indonesia, Vietnam, and Malaysia are experiencing a surge in both personal and commercial EV adoption. This momentum has spurred local lithium-ion battery production, aiming to lessen import reliance and bolster domestic EV sectors, thereby amplifying the demand for battery manufacturing equipment.

- For example, in August 2023, EVE Energy Co. Ltd., a prominent global lithium battery manufacturer from China, broke ground on a new facility in Kulim, Kedah, Malaysia, with an initial investment of USD 422 million. Such strategic investments are poised to elevate lithium-ion battery production for EVs, subsequently driving up the demand for manufacturing equipment.

- Given the declining prices and surging investments in EV lithium-ion battery production, this segment is poised to command a substantial share in the coming years.

Thailand is Expected to Grow Significantly

- Thailand's electric vehicle (EV) battery manufacturing equipment market is poised for substantial growth, bolstered by a favorable environment for EV battery production. With government backing, Thailand has emerged as a regional hub for EV production. The government is luring EV manufacturers and battery producers with tax incentives and subsidies, setting an ambitious goal to have 30% of its automotive output as EVs by 2030.

- Furthermore, a growing number of battery manufacturers, especially from China, are keenly investing in new facilities for EV batteries in Thailand. This surge in investments is set to boost the demand for equipment essential for EV battery production in the country.

- For example, in March 2024, SVOLT Energy, a prominent Chinese battery manufacturer, kicked off mass production of EV battery packs at its state-of-the-art facility in Si Racha, located in Chonburi province, Thailand. This facility is equipped with an impressive annual production capacity of around 60,000 modules and packs.

- As the adoption of electric vehicles continues to surge in Thailand, companies are amplifying their investments in local manufacturing hubs, consequently spurring demand for manufacturing equipment. Data from the Thailand Automotive Institute highlights this trend: in 2023, registered electric vehicles in Thailand surged to 172,540 units, a notable increase from the previous year's 84,570. Such a significant uptick in EV adoption underscores the expanding need for EV manufacturing equipment.

- Looking ahead, the outlook for EV battery manufacturing equipment in Thailand remains optimistic, due to government initiatives like Thailand 4.0 and the Eastern Economic Corridor (EEC). These initiatives are designed to elevate Thailand's status as a regional frontrunner in high-tech sectors, including EVs and batteries, by providing attractive incentives such as tax breaks and simplified regulations.

- Given the government's unwavering support and the accelerating adoption of EVs, Thailand is set for notable growth in the coming years.

ASEAN Countries Electric Vehicle Battery Manufacturing Equipment Industry Overview

The ASEAN country's electric vehicle battery manufacturing equipment market is semi-fragmented. Some of the major players in the market (in no particular order) include WONIK PNE CO., LTD., Schuler AG, Hitachi Ltd, ABB Ltd., and Mitsubishi Heavy Industries, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High initial investment costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendering

- 5.1.4 Slitting and Electrode Making

- 5.1.5 Other Process

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-Acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.2.4 Other Batteries

- 5.3 Geography

- 5.3.1 ASEAN Countries

- 5.3.1.1 Indonesia

- 5.3.1.2 Malaysia

- 5.3.1.3 Philippines

- 5.3.1.4 Singapore

- 5.3.1.5 Thailand

- 5.3.1.6 Vietnam

- 5.3.1.7 Rest of ASEAN Counties

- 5.3.1 ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 WONIK PNE CO., LTD.

- 6.3.2 Schuler AG

- 6.3.3 Hitachi Ltd

- 6.3.4 ABB Ltd.

- 6.3.5 Mitsubishi Heavy Industries, Ltd

- 6.3.6 Sovema Group

- 6.3.7 Daiichi Jitsugyo Thailand Co Ltd

- 6.3.8 Yokogawa India Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

ASEAN諸国のEV用バッテリー製造装置:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日