イタリアのEVバッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年)

Italy Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636452

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

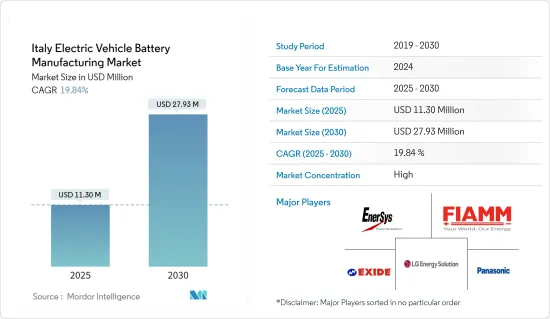

イタリアのEVバッテリー製造の市場規模は2025年に1,130万米ドルと推定され、予測期間(2025-2030年)のCAGRは19.84%で、2030年には2,793万米ドルに達すると予測されます。

主なハイライト

- 中期的には、電池生産能力増強のための投資の増加と原料電池材料のコスト低下が、予測期間中の電気自動車用電池製造需要を牽引すると予想されます。

- 一方、原材料の埋蔵量不足は電気自動車用電池製造市場の成長を大幅に抑制する可能性があります。

- とはいえ、生産能力の拡大、技術進歩の強化、コスト削減といった電気自動車の長期的な野心的目標は、近い将来、電気自動車バッテリー製造市場に大きな機会を生み出すと予想されます。

イタリアのEVバッテリー製造市場動向

リチウムイオン電池タイプが市場を独占

- リチウムイオン(Li-ion)電池は電気自動車(EV)市場に革命をもたらし、電池製造の技術革新を促進しました。高エネルギー密度、長サイクル寿命、急速充電といったリチウムイオン電池の主な特性により、今日のEVにはリチウムイオン電池が選ばれています。

- さらに、リチウムイオン二次電池は容量重量比が優れているため、他の技術を凌駕しています。リチウムイオン二次電池は代替品よりも高価な傾向があるが、市場の大手企業は研究開発投資を増やし、生産を拡大し、競争を激化させて価格を押し下げています。

- EVとバッテリーエネルギー貯蔵システム(BESS)用のバッテリーパックの平均価格は上昇しているが、2023年には大幅に下落し、13%減の139米ドル/kWhとなった。予測によれば、この下落基調は今後も続き、2025年には113米ドル/kWhに達し、2030年にはさらに80米ドル/kWhまで下落すると予想されます。

- 世界的に、各国政府は電気自動車(EV)の普及を加速させ、リチウムイオン電池の生産を拡大するための政策やインセンティブを打ち出しています。戦略的な動きとして、大手国際企業は、特に電気自動車(EV)用リチウムイオン電池の生産を拡大するため、現地企業に多額の投資を行っています。

- 例えば、2024年2月、オートモーティブ・セルズ・カンパニーは、フランス、ドイツ、イタリアに3つのリチウムイオン電池ギガファクトリーを設立するため、47億米ドルの資金を獲得しました。Stellantis、Mercedes-Benz、Saft(TotalEnergiesの子会社)などの業界大手が支援するこのベンチャーは、近い将来、先進的なリチウムイオン電池の需要を高め、その結果、この地域のEV電池製造を強化する態勢を整えています。

- さらに、各国政府は電気自動車(EV)の普及を促進し、リチウムイオン電池産業を発展させるための政策やインセンティブを推進しています。研究開発に重点を置き、これらの政府は、高コストで入手可能性が限られていることで知られるコバルトのような材料に代わる、費用対効果の高い代替材料の発見を目指しています。この戦略的な軸足は、生産コストを削減するだけでなく、持続可能なサプライチェーンを強化します。

- その一例として、2024年7月、ポスコN.EX.Tハブは、全固体電池用に調整された機能性バインダー(PVA-g-PAA)を備えた画期的な負極保護層を発表しました。この革新的な機能により、リチウムの均一な析出が保証され、リチウムの使用量が大幅に削減されるとともに、バッテリーの寿命とエネルギー密度が向上します。このような画期的な技術は、今後数年間で、国内でのバッテリー生産を加速させると思われます。

- その結果、こうした取り組みやプロジェクトがリチウムイオン電池の生産を後押しし、予測期間中にEV用電池の生産能力を著しく向上させることになると思われます。

乗用車セグメントが著しい成長を遂げる

- イタリアの自動車部門は、世界の持続可能性の推進と二酸化炭素排出量削減への取り組みによって、電気自動車(EV)への決定的な転換を図っています。この変革の重要な要素は、電気自動車用バッテリーの生産と改良への注力の強化です。この変化は、イタリアの乗用車市場力学を変化させているだけでなく、業界のさまざまな側面にも影響を及ぼしています。

- さらに、イタリアがクリーンエネルギーを採用するにつれ、電気自動車への移行は多くの企業にとって中心的なテーマとなっています。イタリアでのEV販売は劇的に急増しています。例えば、国際エネルギー機関(IEA)の報告によると、2023年の電気自動車販売台数は13万6,000台で、2022年から19.3%増加し、2019年からは6.8倍という驚異的な伸びを示しました。この勢いとカナダ政府の最近の取り組みに後押しされ、EVの販売台数はさらに増加する見通しで、EV用バッテリーの生産需要が急増していることを示しています。

- 大気汚染に対処し化石燃料への依存を減らすため、イタリアは電気自動車(EV)の導入を精力的に推進しており、この推進はより幅広い乗用車にも及んでいます。政府の多面的な戦略には、財政的な優遇措置、インフラの強化、国民の意識向上キャンペーンなどが含まれ、これらすべてがこの移行を促進するように設計されています。

- そのコミットメントの証として、イタリアは2024年2月、9億5,000万ユーロ(約10億米ドル)という多額の補助金を割り当てた。この資金は、よりクリーンな自動車、特に電気自動車(EV)へのシフトを加速させ、自動車部門を若返らせることを目的としています。具体的には、ローマの戦略には、最大13,750ユーロ(1万5,042米ドル)の手厚い補助金が含まれており、主に低所得者に恩恵があります。この補助金は、35,000ユーロ(3万8,290米ドル)を上限とする新車の完全電気自動車を購入するためのものです。このような措置により、同地域では乗用車の需要が拡大し、予測期間中に電池製造のニーズが高まることが予想されます。

- さらにイタリアでは、大手自動車メーカーが最先端のプラグイン・ハイブリッド電気自動車(PHEV)を導入しています。この動向は、電気自動車と従来型エンジンの利点を融合させ、消費者の要望と地域の規制の両方に対応しようとするメーカーの、PHEVに向けた業界全体の動きを反映しています。

- 例えば、ステランティスは2024年5月、イタリアのミラフィオーリ工場で生産予定の小型電気自動車「500e」のハイブリッド・バージョンを発売する計画を発表しました。500eはすでにイタリアのトリノで生産されています。このような戦略的作戦は、この地域におけるハイブリッド乗用車の普及を促進し、当面のバッテリー製造需要を牽引することになると思われます。

- その結果、こうした取り組みやプロジェクトがEV需要を強化し、今後数年間でEVバッテリー製造のニーズを大幅に高めると予想されます。

イタリアのEVバッテリー製造産業の概要

イタリアのEVバッテリー製造市場は半固体化しています。主要企業(順不同)には、パナソニックホールディングス、Exide Industries Ltd、EnerSys、FIAMM Energy Technology SpA、LG Chem Ltdなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電池生産能力増強のための投資

- 電池原材料コストの低下

- 抑制要因

- 原材料の埋蔵量不足

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリー別

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- その他

- 電池形状別

- 角型

- 袋型

- 円筒形

- 車両別

- 乗用車

- 商用車

- その他

- 推進別

- バッテリー電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- FIAMM Energy Technology SpA

- Panasonic Corporation

- LG Chem Ltd

- EnerSys

- Saft Groupe SA

- FAAM(Fabbrica Accumulatori Motocarri Montenero)

- Exide Industries Ltd

- STMicroelectronics N.V

- MIDAC SpA

- Gotion High tech Co Ltd

- List of Other Prominent Companies

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

目次

Product Code: 50003719

The Italy Electric Vehicle Battery Manufacturing Market size is estimated at USD 11.30 million in 2025, and is expected to reach USD 27.93 million by 2030, at a CAGR of 19.84% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising investments to enhance the battery production capacity and the decline in the cost of raw battery materials are expected to drive the demand for electric vehicle battery manufacturing during the forecast period.

- On the other hand, the lack of raw material reserves can significantly restrain the growth of the electric vehicle battery manufacturing market.

- Nevertheless, the long-term ambitious targets for electric vehicles like scaling up production capacity, enhancing technological advancements, and reducing costs are expected to create significant opportunities for the electric vehicle battery manufacturing market in the near future.

Italy Electric Vehicle Battery Manufacturing Market Trends

Lithium-Ion Battery Type Dominate the Market

- Lithium-ion (Li-ion) batteries have revolutionized the electric vehicle (EV) market, driving innovations in battery production. Their key attributes-high energy density, long cycle life, and swift charging-make them the preferred choice for today's EVs.

- Moreover, lithium-ion rechargeable batteries surpass other technologies due to their excellent capacity-to-weight ratio. Although they tend to be more expensive than alternatives, leading players in the market are boosting R&D investments and ramping up production, heightening competition, and pushing prices down.

- Despite rising average battery pack prices for EVs and battery energy storage systems (BESS), 2023 witnessed a significant dip, with prices falling to USD 139/kWh-a 13% decrease. Projections suggest this downward trajectory will persist, with prices anticipated to reach USD 113/kWh by 2025 and further decline to USD 80/kWh by 2030, driven by relentless technological and manufacturing progress.

- Globally, governments are rolling out policies and incentives to accelerate the adoption of electric vehicles (EVs) and expand Lithium-ion battery production. In a strategic move, major international firms are channeling significant investments into local companies to boost lithium-ion battery production, particularly for electric vehicles (EVs).

- For example, in February 2024, the Automotive Cells Company clinched a USD 4.7 billion funding to set up three lithium-ion battery gigafactories in France, Germany, and Italy. This venture, backed by industry giants like Stellantis, Mercedes-Benz, and Saft (a TotalEnergies subsidiary), is poised to elevate the demand for advanced lithium-ion batteries in the near future, subsequently bolstering EV battery manufacturing in the region.

- Additionally, governments nationwide are pushing policies and incentives to accelerate electric vehicle (EV) adoption and advance the Lithium-ion battery industry. With a focus on R&D, these governments aim to discover cost-effective substitutes for materials like cobalt, known for their high cost and limited availability. This strategic pivot not only reduces production expenses but also strengthens a sustainable supply chain.

- As an illustration, in July 2024, the POSCO N.EX.T Hub introduced a groundbreaking anode protection layer, equipped with a functional binder (PVA-g-PAA), tailored for all-solid-state batteries. This innovative feature guarantees even lithium deposition, significantly curtailing lithium usage, while enhancing battery lifespan and energy density. Such breakthroughs are set to expedite battery production in the country in the forthcoming years.

- Consequently, these initiatives and projects are poised to boost lithium-ion battery production and markedly elevate EV battery manufacturing capacity during the forecast period.

Passengers Cars Segment to Witness Significant Growth

- Italy's automotive sector is making a decisive shift towards electric vehicles (EVs), driven by a global push for sustainability and a commitment to reducing carbon emissions. A key element of this transformation is the intensified focus on the production and refinement of electric vehicle batteries. This shift is not only altering the dynamics of Italy's passenger car market but also influencing various facets of the industry.

- Moreover, as Italy embraces clean energy, the transition to electric vehicles has become a central theme for numerous companies. EV sales in Italy have surged dramatically. For instance, in 2023, the International Energy Agency (IEA) reported 136,000 electric vehicles sold, marking a 19.3% increase from 2022 and a staggering 6.8-fold rise since 2019. With this momentum and buoyed by recent Canadian government initiatives, EV sales are poised to climb further, signaling a booming demand for EV battery production.

- In a bid to tackle air pollution and reduce reliance on fossil fuels, Italy is vigorously promoting the adoption of electric vehicles (EVs), extending this push to encompass a broader range of passenger cars. The government's multifaceted strategy includes financial incentives, infrastructure enhancements, and public awareness campaigns, all designed to facilitate this transition.

- As a testament to its commitment, in February 2024, Italy allocated a significant 950 million euros (about USD 1 billion) in subsidies. This funding aims to accelerate the shift to cleaner vehicles, especially electric cars (EVs), and rejuvenate the automotive sector. Specifically, Rome's strategy includes generous subsidies of up to 13,750 euros (USD 15,042), predominantly benefiting low-income individuals. This financial boost is intended for purchasing new, fully electric vehicles, capped at a price of 35,000 euros (USD 38,290). Such measures are poised to amplify the demand for passenger cars in the region and subsequently heighten the need for battery manufacturing during the forecast period.

- In addition, leading automotive manufacturers are introducing state-of-the-art plug-in hybrid electric vehicles (PHEVs) in Italy. This trend reflects a wider industry movement towards PHEVs, as manufacturers seek to merge the benefits of electric and conventional engines, catering to both consumer desires and regional regulations.

- For example, in May 2024, Stellantis announced its plan to launch a hybrid version of its 500e compact electric car, with production slated at its Mirafiori facility in Italy. The 500e is already in production in Turin, Italy. Such strategic maneuvers are set to boost the uptake of hybrid passenger vehicles in the region and drive the demand for battery manufacturing in the foreseeable future.

- Consequently, these initiatives and projects are anticipated to bolster EV demand and substantially elevate the need for EV battery manufacturing in the coming years.

Italy Electric Vehicle Battery Manufacturing Industry Overview

Italy's electric vehicle battery manufacturing market is semi-consolidated. Some of the key players (not in particular order) are Panasonic Holdings Corporation, Exide Industries Ltd, EnerSys, FIAMM Energy Technology SpA, and LG Chem Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FIAMM Energy Technology SpA

- 6.3.2 Panasonic Corporation

- 6.3.3 LG Chem Ltd

- 6.3.4 EnerSys

- 6.3.5 Saft Groupe SA

- 6.3.6 FAAM (Fabbrica Accumulatori Motocarri Montenero)

- 6.3.7 Exide Industries Ltd

- 6.3.8 STMicroelectronics N.V

- 6.3.9 MIDAC SpA

- 6.3.10 Gotion High tech Co Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

イタリアのEVバッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日