インドの電気自動車用電池製造:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

India Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636466

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

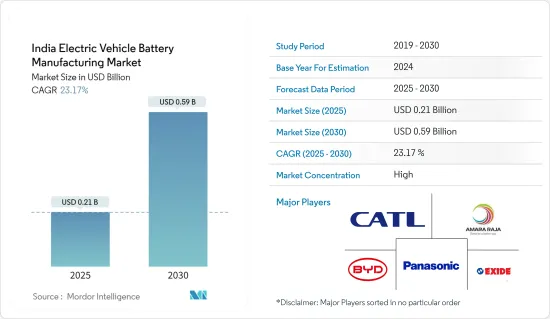

インドの電気自動車用電池製造市場規模は2025年に2億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは23.17%で、2030年には5億9,000万米ドルに達すると予測されます。

主要ハイライト

- 長期的には、電池生産能力増強のための投資や電池原料コストの低下といった要因が、予測期間中のインドの電気自動車用電池製造市場の最も大きな促進要因のひとつになると予想されます。

- 一方、原料サプライチェーンに関連する課題は、予測期間中の市場成長の妨げになると予想されます。

- 電気自動車の長期的な野心的目標は、将来的に市場に機会をもたらすと期待されています。

インドの電気自動車用電池製造市場動向

リチウムイオン電池タイプが市場を独占

- インドの電気自動車(EV)用電池製造市場は、主にリチウムイオン(Li-ion)電池の優位性によって大幅な成長が見込まれています。リチウムイオン電池は、エネルギー密度が高く、ライフサイクルが長く、性能が高いことで知られており、信頼性が高く効率的な自動車を提供することに重点を置くEVメーカーにとって最適な選択肢となっています。

- EVの普及を促進し、EV用電池の現地生産を活性化するため、インド政府は一連のイニシアチブを展開しています。ハイブリッド車・電気自動車の迅速な導入と製造(FAME)スキームは、EVメーカーと購入者の双方に金銭的インセンティブを記載しています。これを補完するPLI(Production Linked Incentive)スキームは、先進化学セル(ACC)蓄電池を対象としており、国内で強固な製造エコシステムを育成することを目指しています。

- インドのEV推進は、二酸化炭素排出の抑制とサステイナブルエネルギーの導入という、より広範な取り組みと共鳴しています。政府の厳しい排出規制と施策は、内燃機関から電気自動車への移行を提唱しています。世界最大の潜在的EV市場であるインドでは、都市化、燃料価格の高騰、環境意識の高まりを背景に、EV需要が急増しています。こうした需要の高まりは、国産電池の必要性を強調し、市場を前進させる。

- 2024年7月、蓄電池大手のExide Industriesは、ベンガルールに建設中の野心的な12ギガワット級リチウムイオン電池製造工場の第1段階が会計年度末までに完成する予定であると発表しました。一方、コルカタに拠点を置くExideの子会社、Exide Energy Solutions(EESL)は、リチウムイオン電池製造プロジェクトの仕上げに近づいています。EESLは、インドのEV市場の急速な拡大を認識し、自動車大手の現代自動車と起亜自動車と拘束力のない覚書(MOU)を締結し、戦略的協力関係を結んでいます。

- EVの普及を促進するため、全国的な充電インフラの開発に大規模な投資が行われています。急増するインフラは、電気自動車の普及を支えるだけでなく、国産電池の需要を高めます。インド企業は研究開発への投資を拡大しており、電池技術の改良とコスト削減を目指しています。国際的な技術プロバイダーや研究機関との提携は、電池製造におけるイノベーションの起爆剤となっています。

- 2024年7月、LICOはバンガロールに最新鋭の施設を建設し、インド最大級のリチウムイオン電池リサイクル工場として事業拡大を発表しました。2024年10月までに操業を開始するLICOの施設は、2026年までに年間2万5,000トンの意欲的な処理能力を目指します。戦略的には、輸送リスクとコストを軽減するため、ハブ・アンド・スポーク型の操業モデルを採用し、地域的な処理を重視します。EVの普及が加速する中、インドは使用済み電池を効率的に管理し、将来に備えたインフラを確保するための準備を進めています。

- インドのリチウムイオン電池(LiB)製造セクターは上昇基調にあり、大手企業は急成長するEV市場に対応するため、新たな設備への戦略的投資を行っています。PLIスキームの下、Ola Electric、Reliance、Rajesh Exportといった産業大手は、セル製造のための優遇措置を確保し、2024年の生産を予定しています。さらに、多くの企業がLiB電池工場を計画的に拡大し、国内外市場に対応できる体制を整えつつあります。

- こうした開発により、この地域はEV用電池の生産が急増し、それに伴ってリチウムイオン電池の需要も今後数年で増加する展望です。

電池生産能力増強のための投資

- インドでは、電気自動車(EV)の需要急増に対応するため、電池製造能力を増強しています。先進化学セル(ACC)蓄電池の生産連動型奨励金(PLI)制度のような取り組みを通じて、政府は投資を呼び込み、現地生産を強化しようとしています。この戦略的な動きは、輸入依存を抑制し、強固な国内電池製造環境を育成するために極めて重要です。

- 急成長するEV市場に対応するため、新しい電池生産工場がインド全土に出現しています。Exide Industries、Amara Raja、Tata Chemicalsといった産業大手は、最先端設備への投資を進めています。これらの工場は、国内需要を満たし、技術革新を促進し、雇用を創出する上で重要な役割を果たしており、インドのEV電池製造セクターの成長を後押ししています。

- 電池製造の野心を強化するため、インドは、最高級リチウムイオン電池の製造に不可欠なスラリーミキサーを含む先進設備の入札を実施しています。これらの入札は、効率と生産量を向上させる最先端技術を対象としています。製造プロセスを近代化することで、インドのEV用電池生産の競合ベンチマーキングと品質を向上させ、世界のベンチマークに合わせることを目指しています。

- 例えば、2024年7月には、電動二輪車とスマートモビリティのセグメントで著名な台湾のAhamani EV Technologyが、インドのEV事情に多額の投資を行う予定です。同社は、インドにメガワット規模の電池製造ユニットを設立する計画で、インドの大手自動車関連企業との戦略的技術移転提携を模索しています。すでに3~4社の大手EV企業と交渉が進んでいます。政府の支援施策や、環境に優しい輸送手段に対する消費者の需要の急増によって、インドでは電動モビリティが重視されるようになっています。現地に建設予定の電池施設は、EVバリューチェーンにおけるインドの自給率向上を目指すだけでなく、雇用創出と経済活性化を約束するものでもあります。

- インド政府は、税制優遇措置、メーカーや消費者に対する補助金、充電インフラへの投資など、さまざまな取り組みを通じてEVセクターを積極的に支援しています。これらの施策は、EVの購入しやすさと利便性を向上させ、普及率を高め、ひいては電池材料の需要を押し上げることを目的としています。電池技術の革新も市場力学に影響を与えています。例えば、BYDはリン酸鉄リチウム(LFP)電池のような新しい電池化学を開拓しており、安全でコスト効率が高い一方で、従来のリチウムイオン電池に比べてエネルギー密度はわずかに低いです。このようなブレークスルーは、EVをより多くの人々が利用できるようにする上で重要な役割を担っています。

- 2024年8月、Amara Raja Advanced Cell Technologies(ARACT)は、インドにおけるEV技術の推進を目指し、Piaggio Vehicles Private Limitedと覚書を交わしました。この提携は、Piaggioの電動三輪車と今後発売される二輪車に合わせたリチウムイオンセル、電池パック、充電器の製造と供給を中心に行われます。

- インドは世界の動向に合わせて、2029年までに電気自動車(EV)の野心的な販売目標を掲げています。政府は、インドのEVへの意欲を高めるため、国内生産、特に電池生産を重視しています。30@30」構想やその他の大胆な予測のもと、インドでは2023年に42.5GWhの累積電池容量が必要とされ、2029年には577.8GWhに急増する見込みです。この急増は、インドの年間電池必要量が世界の生産量の17%から26%を占める可能性があることを意味します。さらに、こうした需要に応えるだけでなく、コストを引き下げてEVの市場競合を高めるためにも、生産の拡大が不可欠です。確固たる国内生産基盤を確立することは、日本にとって大きな経済的メリットをもたらします。

- 結論として、こうした取り組みと投資により、インドの電池生産能力は大幅に強化されることになります。

インドの電気自動車用電池製造産業概要

インドの電気自動車用電池製造市場は半集中型です。この市場の主要企業(順不同)には、BYD、Contemporary Amperex Technology Co.Ltd.、Panasonic Corporation、Exide Industries、Amara Raja Batteries Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電池生産能力増強のための投資

- 電池原料コストの低下

- 抑制要因

- 原料の埋蔵量不足

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池

- リチウムイオン

- 鉛-酸

- ニッケル水素電池

- その他

- 電池形態

- 角型

- 袋型

- 円筒形

- 車両

- 乗用車

- 商用車

- その他

- 推進

- 電池電気自動車

- ハイブリッドの電気自動車

- プラグインハイブリッドの電気自動車

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- Amara Raja Batteries Ltd.

- Tata Chemicals

- HBL Power Systems Ltd.

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

目次

Product Code: 50003733

The India Electric Vehicle Battery Manufacturing Market size is estimated at USD 0.21 billion in 2025, and is expected to reach USD 0.59 billion by 2030, at a CAGR of 23.17% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as Investments to enhance battery production capacity and the decline in the cost of battery raw materials are expected to be among the most significant drivers for the India Electric Vehicle Battery Manufacturing Market during the forecast period.

- On the other hand, challenges associated with the raw material supply chain are expected to hinder market growth during the forecast period.

- Nevertheless, long-term ambitious targets for electric vehicles are expected to create opportunities for the market in the future.

India Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Type to Dominate the Market

- India's electric vehicle (EV) battery manufacturing market is set for substantial growth, primarily fueled by the supremacy of lithium-ion (Li-ion) batteries. Li-ion batteries, known for their superior energy density, extended life cycles, and enhanced performance, have become the go-to choice for EV manufacturers focused on delivering reliable and efficient vehicles.

- To bolster EV adoption and stimulate local EV battery manufacturing, the Indian government has rolled out a series of initiatives. The Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme offers financial incentives to both EV manufacturers and buyers. Complementing this, the Production Linked Incentive (PLI) scheme targets advanced chemistry cell (ACC) battery storage, aiming to cultivate a robust manufacturing ecosystem within the country.

- India's push for EVs resonates with its broader commitment to curbing carbon emissions and embracing sustainable energy. The government's stringent emission norms and policies advocate a transition from internal combustion engines to electric vehicles. As the world's largest potential EV market, India's demand for EVs is surging, driven by urbanization, escalating fuel prices, and heightened environmental consciousness. This burgeoning demand underscores the necessity for domestically produced batteries, propelling the market forward.

- In July 2024, Exide Industries, a leading storage battery firm, announced that the first phase of its ambitious 12-gigawatt lithium-ion cell manufacturing plant in Bengaluru is on track for completion by the financial year's end. Meanwhile, Exide's Kolkata-based subsidiary, Exide Energy Solutions (EESL), is nearing the finish line with its lithium-ion cell manufacturing project. Recognizing the rapid expansion of India's EV market, EESL has inked a non-binding memorandum of understanding (MOU) with automotive giants Hyundai Motor and Kia Corporation, signaling a strategic collaboration.

- Massive investments are being funneled into the development of charging infrastructure nationwide, a move that bolsters EV adoption. This burgeoning infrastructure not only supports the widespread use of electric vehicles but also amplifies the demand for locally produced batteries. Indian firms are ramping up investments in research and development, aiming to refine battery technologies and curtail costs. Collaborations with international tech providers and research institutions are catalyzing innovations in battery manufacturing.

- In July 2024, LICO announced its operational expansion with a state-of-the-art facility in Bangalore, poised to be one of India's largest lithium-ion battery recyclers. Set to commence operations by October 2024, LICO's facility aims for an ambitious processing capacity of 25,000 tonnes annually by 2026. Strategically, the plant will emphasize regional processing to mitigate transportation risks and costs, adopting a hub-and-spoke operational model. As EV adoption accelerates, India is gearing up to efficiently manage end-of-life batteries, ensuring a future-ready infrastructure.

- India's Lithium-ion Battery (LiB) manufacturing sector is on an upward trajectory, with major players making strategic investments in new facilities to cater to the burgeoning EV market. Under the PLI scheme, industry stalwarts like Ola Electric, Reliance, and Rajesh Export have secured incentives for cell manufacturing, with production slated for 2024. In addition, numerous companies are methodically scaling up their LiB battery plants, positioning themselves to cater to both domestic and international markets.

- Given these developments, the region is poised for a surge in EV battery production, with a corresponding uptick in demand for lithium-ion batteries in the coming years.

Investments to Enhance the Battery Production Capacity

- India is ramping up its battery manufacturing capabilities to satisfy the surging demand for electric vehicles (EVs). Through initiatives like the Production Linked Incentive (PLI) scheme for advanced chemistry cell (ACC) battery storage, the government seeks to draw in investments and bolster local production. This strategic move is pivotal for curbing import reliance and nurturing a robust domestic battery manufacturing landscape.

- New battery production plants are emerging across India, catering to the burgeoning EV market. Industry giants such as Exide Industries, Amara Raja, and Tata Chemicals are channeling investments into cutting-edge facilities. These plants play a crucial role in satiating domestic demand, spurring innovation, and generating employment, thus propelling the growth of India's EV battery manufacturing sector.

- To bolster its battery manufacturing ambitions, India is issuing tenders for advanced equipment, including slurry mixers, vital for producing top-tier lithium-ion batteries. These tenders target state-of-the-art technology to boost efficiency and output. By modernizing its manufacturing processes, India aims to elevate the competitiveness and quality of its EV battery production, aligning it with global benchmarks.

- For example, in July 2024, Ahamani EV Technology Co., Ltd., a prominent Taiwanese player in electric two-wheelers and smart mobility, is set to make a substantial investment in India's EV landscape. The firm plans to set up a megawatt-scale battery manufacturing unit in India and is on the lookout for strategic technology transfer collaborations with major Indian automotive entities. Talks are already in progress with 3-4 leading EV firms. Given India's heightened emphasis on electric mobility, bolstered by supportive government policies and a surge in consumer demand for eco-friendly transport, Ahamani sees a golden opportunity. The envisioned local battery facility not only aims to bolster India's self-sufficiency in the EV value chain but also promises job creation and economic stimulation.

- India's government is actively backing the EV sector through a range of initiatives, including tax breaks, subsidies for manufacturers and consumers alike, and investments in charging infrastructure. These measures aim to enhance the affordability and convenience of EVs, driving up adoption rates and, in turn, boosting the demand for battery materials. Battery technology innovations are also influencing the market dynamics. For instance, BYD is pioneering new battery chemistries, like lithium iron phosphate (LFP) batteries, which, while being safer and more cost-effective, have a marginally lower energy density compared to conventional lithium-ion batteries. Such breakthroughs are instrumental in making EVs more accessible to the broader public.

- In August 2024, Amara Raja Advanced Cell Technologies (ARACT) inked a Memorandum of Understanding (MoU) with Piaggio Vehicles Private Limited, aiming to propel EV technology in India. This collaboration centers on crafting and supplying lithium-ion cells, battery packs, and chargers tailored for Piaggio's electric three-wheelers and upcoming two-wheelers.

- India is setting its sights on ambitious electric vehicle (EV) sales targets by 2029, in line with global trends. The government is emphasizing domestic manufacturing, especially in battery production, to fuel India's EV aspirations. Under the "30@30" initiative and other bold projections, India needed a cumulative battery capacity of 42.5 GWh in 2023, with expectations to skyrocket to 577.8 GWh by 2029. This surge means India's annual battery requirements could represent 17% to 26% of global production. Moreover, ramping up production is crucial not only to meet these demands but also to drive down costs, enhancing the market competitiveness of EVs. Establishing a solid domestic manufacturing foundation promises substantial economic advantages for the country.

- In conclusion, these initiatives and investments are set to significantly bolster India's battery production capabilities.

India Electric Vehicle Battery Manufacturing Industry Overview

The India Electric Vehicle Battery Manufacturing Market is semi-concentrated. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Limited, Panasonic Corporation, Exide Industries, and Amara Raja Batteries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 GS Yuasa Corporation

- 6.3.5 LG Chem Ltd

- 6.3.6 Exide Industries

- 6.3.7 Panasonic Corporation

- 6.3.8 Amara Raja Batteries Ltd.

- 6.3.9 Tata Chemicals

- 6.3.10 HBL Power Systems Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

インドの電気自動車用電池製造:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日