|

|

市場調査レポート

商品コード

1406971

日本の植物性タンパク質:市場シェア分析、産業動向と統計、成長予測、2024年~2029年Japan Plant Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の植物性タンパク質:市場シェア分析、産業動向と統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

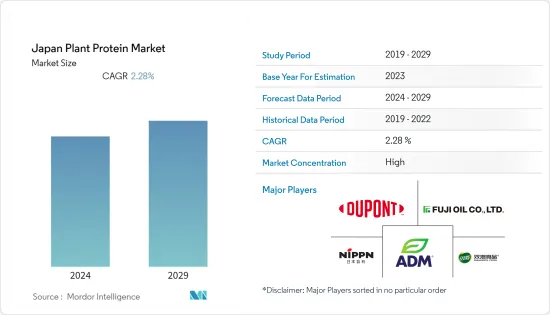

日本の植物性タンパク質市場規模は、2024年の2億9,958万米ドルから、今後数年間でCAGR 2.28%で成長すると予測されます。

主なハイライト

- 日本の植物性タンパク質市場は、持続可能で植物由来の食事に対する消費者の嗜好の変化により、近年大幅な成長を遂げています。環境と健康に対する意識が高まり続ける中、日本の消費者の多くが動物性タンパク質に代わるものを求めており、植物性タンパク質の人気が高まっています。日本の若い世代は持続可能性に関心が高く、新しい食品動向に関心があります。企業は、将来的に高タンパク質が彼らの食生活の主食となるよう、手頃な価格でおいしい製品を提供することで彼らにアピールする必要があります。

- 日本の高齢化のもう一方では、シルバー世代市場が巨大です。例えば、総務省によると、2022年11月、日本の65歳以上の人口は3,650万人近くに上ると推定されています。動物性タンパク質は高齢者にとって消化が難しいため、植物性タンパク質はこの市場で普及するチャンスがあります。

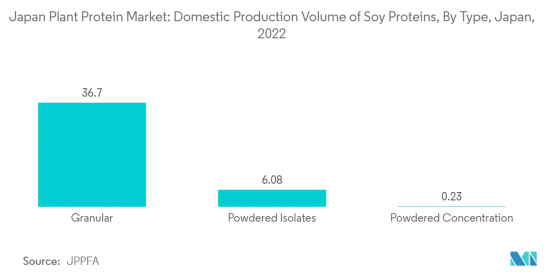

- さらに日本は、代替タンパク質を含む食品技術を推進する政府機関を設立しました。2021年、政府は白書を発表し、代替食肉は食肉よりも生産時に排出される温室効果ガスが少ないため、日本が2050年のネットゼロエミッション目標を達成するためのソリューションとして挙げました。日本貿易振興機構(JETRO)のような経済機関も、国内外の高タンパク質企業と協力して市場拡大に取り組んでいます。また、日本植物蛋白食品協会(JPPFA)によると、2022年の小麦蛋白の国内生産量は約5,700トンでした。日本で加工される小麦グルテンには、主に粒状、粉末状、ペースト状の製品があります。これらは模擬肉の製造に使われることもあるが、日本料理では蒸したり焼いたりした生地ブロックとして最も一般的に見られます。

日本の植物性タンパク質市場動向

大豆タンパク質が最大の市場シェアを占める

- 大豆は何世紀にもわたって日本の伝統的な主食であり、大豆ベースの製品は文化的に受け入れられ、国民に親しまれています。この長年の親しみが、大豆タンパクベースの飲食品を採用するための自然な基盤となっています。さらに、大豆たん白は優れた栄養価を誇っています。人体に必要な9種類の必須アミノ酸をすべて含む完全タンパク質です。

- さらに、飽和脂肪酸が少なく、コレステロールフリーで、ビタミン、ミネラル、食物繊維を豊富に含んでいます。その結果、大豆タンパク質は、栄養価が高くバランスのとれた植物性の代替食品を求める健康志向の消費者にアピールしています。日本における大豆タンパク質の人気は、特定の食事嗜好や食事制限を持つ人々の増加によっても強化されています。

- 菜食主義者、ベジタリアン、乳糖不耐症の人々は、タンパク質やその他の必須栄養素の有効な供給源として大豆ベースの製品をよく利用します。このような消費者層の拡大が、大豆タンパク質製品の需要をさらに押し上げています。例えば、JPPFAによると、2022年の日本の粉末濃縮大豆たん白の国内生産量は約231トンに達しました。

- さらに、健康的で持続可能な食生活を推進する日本政府の取り組みが、大豆たん白を含む植物性たん白の増加に寄与しています。植物性タンパク質分野の研究開発を支援する取り組みや、公的機関に植物性食品を含めることで、消費者と企業の両方が、実行可能で環境に優しい選択肢として大豆タンパク質を受け入れるようになった。

- 植物性食生活への関心の高まりと、従来の食肉生産が環境に与える影響への懸念を受けて、日本の消費者は、動物性製品の味と食感に近い類似肉を求めています。肉の食感を模倣する能力を持つ大豆タンパク質は、こうした植物ベースの肉代替食品の主要成分として機能し、市場での人気を牽引しています。

- 例えば、2021年3月、不二製油グループは酒井幹雄氏を新社長兼CEOに任命しました。酒井幹夫氏は、油脂事業、チョコレート事業と並ぶ第3の事業の柱として成長させるため、植物由来の食品ソリューションを中核コンセプトとして取り組んでいます。植物性フードソリューションとは、植物性タンパク質の原料となる大豆や大豆ミートなどのこと。

消費者のタンパク質リッチ食品への傾斜

- 黄えんどう豆のような原料からの植物性タンパク質の出現は、動物性タンパク質から同様の機能的・栄養的特性を持つ植物性タンパク質への顧客需要の変化を示しています。植物性食生活へのこの漸進的なシフトは、主として、生態系への懸念、健康意識、倫理的または宗教的信条、環境および動物の権利など、さまざまな要因に影響されています。

- さらに、日本では高齢者人口が増加しており、栄養補助食品への需要が高まっています。濃縮大豆蛋白は、栄養補助食品に使用され、余分な粗蛋白質を供給します。2021年の世界銀行のデータによると、日本の人口の29.79%が65歳以上です。また、CargillやRoquetteのような企業は、大豆や小麦に代わる低アレルゲンである植物性タンパク質に投資しています。

- さらに、日本人の肥満、心血管疾患、糖尿病の増加により、消費者は菜食主義を採用するようになった。例えば、World Population Reviewによると、2022年の日本の成人肥満の有病率は21.8%でした。乳タンパク質にアレルギーのある人にとって、植物性タンパク質は代替のタンパク質源となります。例えば、公益財団法人がん対策情報センターによると、2021年の日本における心臓病による死亡者数は約21万4,700人でした。さらに、植物性タンパク質は、キャセロール、チリ、スパゲティ・ソース、ミートシチュー、ミートソースなどの缶詰肉製品において、ひき肉を延長したり完全に置き換えたりするために使用することができます。また、パテやミートボールなどの缶詰製品において、ひき肉を延長するために使用することもできます。膨大な用途と多様な機能性がその使用を後押しし、メーカーが様々な植物タンパク質の使用を増やす原動力となっています。パーソナルケア分野では、加水分解植物タンパク質は膨大な用途があります。上記の全ての要因が、日本の植物蛋白市場を牽引しています。

日本の植物性タンパク質産業の概要

日本の植物蛋白市場は断片化されており、上位5社が参入しています。この市場の主要企業は、Archer Daniels Midland Company、DuPont de Nemours Inc.、不二製油グループ、日本株式会社、Yantai Shuangta Foodです。日本の植物性タンパク質市場の主要企業は、研究開発に投資し、製品ポートフォリオを強化するためにM&Aに参入しています。市場の急速な新興国市場の性質上、新製品のイノベーションは、市場における消費者のニーズの変化を理解するのに役立つため、すべての間で最も一般的に使用される戦略となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 消費者のタンパク質リッチ食品への傾斜

- 植物性タンパク質源に対する嗜好の高まり

- 抑制要因

- 植物性タンパク質に関連するアレルギー

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タンパク質タイプ別

- ヘンプタンパク質

- エンドウ豆タンパク質

- ポテトタンパク質

- 米タンパク質

- 大豆タンパク質

- 小麦タンパク質

- その他の植物性タンパク質

- エンドユーザー別

- 動物飼料

- パーソナルケアと化粧品

- 食品・飲料

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料・ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- サプリメント

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第6章 競合情勢

- Market Positioning Analysis

- 市場シェア分析

- 企業プロファイル

- Archer Daniels Midland Company

- Bunge Limited

- Cargill, Incorporated

- DuPont de Nemours Inc.

- Fuji Oil Group

- Nagata Group Holdings, ltd.

- Nippn Corporation

- Roquette Frere

- Yantai Shuangta Food Co. Ltd

第7章 市場機会と今後の動向

The Japan plant protein market size is expected to grow from USD 299.58 million in 2024 at a CAGR of 2.28% over the upcoming years.

Key Highlights

- The Japan plant protein market has witnessed substantial growth in recent years, largely driven by changing consumer preferences towards sustainable and plant-based diets. As awareness of environmental and health concerns continues to rise, many Japanese consumers are seeking alternatives to animal-based proteins, making plant proteins increasingly popular. Japan's younger generations are more sustainability-minded and interested in new food trends. Companies need to appeal to them with affordable and tasty offerings to ensure that alt proteins become a staple part of their diets in the future.

- On the other end of Japan's aging population, the silver generation market is huge. For instance, according to the Ministry of Internal Affairs and Communications (Japan), in November 2022, close to 36.5 million people in Japan were estimated to be within the age group of 65 and over. Animal proteins are difficult to digest for seniors, so plant-based proteins have an opportunity to become popular in this market.

- Furthermore, Japan has established Government bodies to promote food technology, including alternative proteins. In 2021, the government released a white paper that listed substitute meats as a solution to helping Japan reach 2050 targets for net-zero emissions because they release fewer greenhouse gasses during their production than meat. Economic institutions like the Japan External Trade Organization are also working to collaborate with alt protein companies inside and outside of Japan to help grow the market. Also, in 2022, the domestic production volume of wheat proteins in Japan amounted to around 5.7 thousand tons, according to the Japan Plant Protein Food Association (JPPFA). Wheat gluten processed in Japan includes mainly granular, powdered, and paste-like products. They can be used in the production of mock meat but are most commonly found as steamed or baked dough blocks in Japanese cuisine.

Japan Plant Protein Market Trends

Soy Protein Held the largest Market Share

- Soybeans have been a traditional staple of the Japanese diet for centuries, making soy-based products culturally accepted and familiar to the population. This longstanding familiarity provides a natural foundation for the adoption of soy protein-based foods and beverages. Furthermore, soy protein boasts an impressive nutritional profile. It is a complete protein containing all nine essential amino acids required by the human body.

- Additionally, it is low in saturated fat, cholesterol-free, and a good source of vitamins, minerals, and dietary fiber. As a result, soy protein appeals to health-conscious consumers looking for nutritious and balanced plant-based alternatives. The popularity of soy protein in Japan is also reinforced by the growing number of individuals with specific dietary preferences or restrictions.

- Vegans, vegetarians, and those with lactose intolerance often turn to soy-based products as a viable source of protein and other essential nutrients. This expanding consumer base further drives the demand for soy protein products in the market. For instance, according to the JPPFA, In 2022, the domestic production volume of powdered concentration of soy proteins in Japan amounted to around 231 tons.

- Moreover, the Japanese government's efforts to promote a healthy and sustainable diet have contributed to the rise of plant-based proteins, including soy protein. Initiatives supporting research and development in the plant protein sector and the inclusion of plant-based foods in public institutions have encouraged both consumers and businesses to embrace soy protein as a viable and eco-friendly option.

- In response to the growing interest in plant-based diets and concerns over the environmental impact of conventional meat production, Japanese consumers are seeking meat analogs that closely resemble the taste and texture of animal-based products. Soy protein, with its ability to mimic the texture of meat, serves as a key ingredient in these plant-based meat substitutes, driving their popularity in the market.

- For instance, in March 2021, Fuji Oil Group appointed Mikio Sakai as the new president and CEO. Mikio Sakai is engaged in plant-based food solutions as a core concept to grow a third business pillar, along with the Oil and Fat and Chocolate businesses. Plant-based food solutions include soy meat and soybeans, which are used as raw materials for plant-based proteins.

Consumer Inclination Toward Protein-rich Food

- The emergence of vegetable protein from sources like yellow peas demonstrates a change in customer demand from animal protein to plant protein with similar functional and nutritional characteristics. This incremental shift toward a plant-based diet is primarily influenced by various factors, including ecological concerns, health consciousness, ethical or religious beliefs, and environmental and animal rights.

- Additionally, the old age population in Japan is increasing, due to which their demand for dietary supplements is increasing. Soy protein concentrate is used in dietary supplements to provide extra crude protein. According to World Bank data from 2021, 29.79% of people in Japan are above the age of 65. Also, companies like Cargill and Roquette are investing in plant protein as it is a low-allergenic alternative to soy and wheat.

- Moreover, the rising incidences of obesity, cardiovascular diseases, and diabetes among the Japanese population prompted consumers to adopt vegan diets. For instance, according to the World Population Review, the prevalence of adult obesity was 21.8% in Japan in 2022. For those who are allergic to milk protein, plant protein offers an alternative source of protein. For instance, according to the Center for Cancer Control and Information Services Japan, the total number of deaths caused by heart diseases amounted to approximately 214.7 thousand cases in Japan in 2021. Additionally, plant protein may be used to extend or completely replace ground meat in canned meat products such as casseroles, chili, spaghetti sauces, meat stews, and meat sauces. It can also be used to extend ground meat in canned products such as patties and meatballs. The immense applications and diverse functionalities are boosting their use and driving manufacturers to increase their use of various plant proteins. In the personal care segment, hydrolyzed plant proteins have immense applications. All the above-mentioned factors drive the plan protein market in the country.

Japan Plant Protein Industry Overview

The Japan plant protein market is fragmented, with the top five companies. The major players in this market are Archer Daniels Midland Company, DuPont de Nemours Inc., Fuji Oil Group, Nippon Corporation, and Yantai Shuangta Food Co. Ltd. Key Japanese Plant Protein market players are investing in R&D and entering into mergers and acquisitions to enhance their product portfolios. Owing to the rapidly developing nature of the market, new product innovation has become the most commonly used strategy among all, as it helps in understanding the changing needs of the consumers in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Consumer Inclination Toward Protein-rich Food

- 4.1.2 Growing Inclination Towards Plant-based Protein Sources

- 4.2 Restraints

- 4.2.1 Associated Allergies With Plant Proteins

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 Market Segmentation

- 5.1 By Protein Type

- 5.1.1 Hemp Protein

- 5.1.2 Pea Protein

- 5.1.3 Potato Protein

- 5.1.4 Rice Protein

- 5.1.5 Soy Protein

- 5.1.6 Wheat Protein

- 5.1.7 Other Plant Protein

- 5.2 By End-User

- 5.2.1 Animal Feed

- 5.2.2 Personal Care and Cosmetics

- 5.2.3 Food and Beverages

- 5.2.3.1 Bakery

- 5.2.3.2 Beverages

- 5.2.3.3 Breakfast Cereals

- 5.2.3.4 Condiments/Sauces

- 5.2.3.5 Confectionery

- 5.2.3.6 Dairy and Dairy Alternative Products

- 5.2.3.7 Meat/Poultry/Seafood and Meat Alternative Products

- 5.2.3.8 RTE/RTC Food Products

- 5.2.3.9 Snacks

- 5.2.4 Supplements

- 5.2.4.1 Baby Food and Infant Formula

- 5.2.4.2 Elderly Nutrition and Medical Nutrition

- 5.2.4.3 Sport/Performance Nutrition

6 Competitive Landscape

- 6.1 Market Positioning Analysis

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland Company

- 6.3.2 Bunge Limited

- 6.3.3 Cargill, Incorporated

- 6.3.4 DuPont de Nemours Inc.

- 6.3.5 Fuji Oil Group

- 6.3.6 Nagata Group Holdings, ltd.

- 6.3.7 Nippn Corporation

- 6.3.8 Roquette Frere

- 6.3.9 Yantai Shuangta Food Co. Ltd