英国の植物性タンパク質:市場シェア分析、産業動向、成長予測(2025~2030年)

United Kingdom Plant Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 214 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690990

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

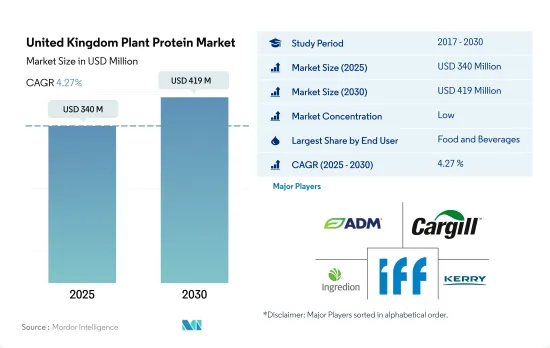

英国の植物性タンパク質市場規模は、2025年には3億4,000万米ドルと推定され、2030年には4億1,900万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4.27%で成長すると予測されます。

などがあります。

全国的な菜食主義の高まりが、特に動物飼料とF&Bセグメントでの植物性タンパク質の応用を促進しました。

- F&Bセグメントの需要が高いのは、国内で菜食主義が台頭する中、肉や乳製品の代替品への需要が高まっているためです。従って、このセグメントは予測期間中、数量ベースでCAGR 4.59%を記録すると予想されます。2021年1月、欧州では約50万人(うち12万5,000人は英国を拠点とする)がヴィーガンフードのみを食べるというヴィーガンの誓いを立て、2020年から10万人増加し、2019年の約2倍となりました。2019年の同国のヴィーガン人口は60万人で、英国人口の1.16%を占めました。

- サプリメントセグメントは、予測期間中に最速のCAGR 7.67%を記録すると予測されています。このセグメントは大豆タンパク質の用途が主要原動力となっており、2020年には40.4%のシェアを占めます。また、予測期間中のCAGRは8.83%で、このセグメントで最も急成長しているタンパク質タイプになると予測されています。消費者は、パフォーマンスを向上させ、より健康的でサステイナブルライフスタイルを手に入れるため、ヴィーガンのスポーツ栄養製品にシフトしています。英国では、2021年のスポーツ栄養ユーザーの62%が、植物性タンパク質を使用したスポーツ栄養製品はより健康的であると考えています。

- 植物性タンパク質は動物飼料産業で大きなシェアを占めており、予測期間には金額ベースで2.61%の成長を記録すると予測されています。英国の飼料産業は、トウモロコシ、大豆、菜種の年間必要量の70%以上を輸入しています。同国の大豆の少なくとも90%は家畜に給餌され、年間食用に使われるのはせいぜい10%です。大豆タンパク質は主に家畜、特に牛肉、鶏肉、卵、酪農に与えられています。

英国の植物性タンパク質市場動向

植物性タンパク質消費の成長は、原料セグメントにおける主要企業のビジネス機会を促進します。

- 健康な成人の推奨タンパク質摂取量は0.83g/kg/dです。60歳以下の成人の平均タンパク質摂取量は0.83~2.2g/kg/dです。成人女性の1日平均タンパク質摂取量は74g、成人男性は100gです。ミレニアル世代とZ世代が、特に植物ベースの食事とサプリメントの需要拡大を牽引しています。これは主に、植物性タンパク質が、動物性タンパク質の代わりとなる必須アミノ酸をすべて含む唯一の供給源に急速になりつつあるためです。タンパク質セグメントの出現は、動物性タンパク質への依存に伴う環境への影響を削減できる可能性があります。

- 植物性食品のトップユーザーは、肉の摂取を控えた方が健康にも環境にも良いと考える若年層と都市部の顧客です。英国では来年、肉食をやめるか、ベジタリアンまたはヴィーガン食を採用する人が増えると予想されます。英国政府は、消費者の健康的なライフスタイルと食生活を推進しています。これは、オーガニックで純度が高く、健康に良いとされる大豆タンパク材料にとって機会となります。大豆タンパク質の一人当たりの消費量は、2016~2022年にかけて4.6%増加しました。

- 英国では、2019~2020年にかけての一人当たりの一週間平均米消費量は111グラムでした。米には、チアミン、リボフラビン、ナイアシン、ビタミンE、亜鉛、カリウム、鉄、食物繊維などの必須栄養素が含まれています。英国国民の平均的な年間米消費量は約5.6kgで、購入量の80%を白米が占めています。民族人口の拡大と食生活の多様化により、英国の米消費量は大幅に増加すると予想されます。

英国は小麦とエンドウ豆の生産能力強化に力を入れている

- グラフは、英国で生産されるドライエンドウ、米、小麦、大豆などの原料の生産データです。同国は小麦とエンドウ豆の主要生産国です。2021年の小麦の生産量は、定期的な降雨と温暖な気候に助けられ、約1,400万トンに達しました。同様に、前年の秋の作付け条件がかなり良好だったため、2020年の小麦の収量が向上し、大麦のような春作物よりも冬小麦の作付けが促進されました。エンドウ豆の生産に関しては、同国は90%を自給しています。

- 同国の恵まれない環境とそれに伴う収穫の問題は、大豆生産を制限しています。しかし、食品・飼料セグメントからの需要の高まりが農業従事者の関心を刺激し、英国におけるこの作物のポテンシャルを大幅に高めています。2021年には、作付可能面積が0.5%増の610万ヘクタールとなり、大豆生産を後押しします。

- 消費者が植物性食品、特に肉や乳製品の通路にある代替タンパク質を購入するケースが増加しています。特に肉代替食品の売上は、嗜好の向上と製品の入手しやすさが追い風となり、過去2年間で60%も急増しました。現在、英国では成人の14%(720万人)が肉を食べない食生活を送っています。2022年にはさらに880万人が肉を食べない食生活を送る予定だ(過去4年間で最高の数字)。その結果、英国の適切な気候条件に合わせて大豆種の生産が増加しています。2022年6月までの12ヵ月間の大豆輸入量は約68万8,000トンとなり、前年のデータを上回りました。

英国の植物性タンパク質産業概要

英国の植物性タンパク質市場は細分化されており、上位5社で37.46%を占めています。この市場の主要企業は、Archer Daniels Midland Company、Cargill Incorporated、Ingredion Incorporated、International Flavors & Fragrances Inc.、Kerry Group PLCなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タンパク質タイプ

- ヘンプ・タンパク質

- エンドウ豆タンパク質

- ポテト・タンパク質

- 米タンパク質

- 大豆タンパク質

- 小麦タンパク質

- その他の植物性タンパク質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A. Costantino & C. SpA

- Archer Daniels Midland Company

- Cargill Incorporated

- Ingredion Incorporated

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- Lantmannen

- Roquette Frere

- Tereos SCA

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The United Kingdom Plant Protein Market size is estimated at 340 million USD in 2025, and is expected to reach 419 million USD by 2030, growing at a CAGR of 4.27% during the forecast period (2025-2030).

Rising veganism across the country drove the application of plant protein especially in animal feed and F&B segments

- The high demand for the F&B sector is attributable to the growing demand for meat and dairy alternatives amid the rising veganism in the country. Thus, the segment is anticipated to register a CAGR of 4.59% by volume during the forecast period. In January 2021, around 500,000 people in Europe, of whom 125,000 are based in the United Kingdom, took the Vegan Pledge to eat only vegan food, which was up by 100,000 from 2020 and almost double the number of people who signed up in 2019. In 2019, there were 600,000 vegans in the country, which accounted for 1.16% of the British population.

- The supplements segment is projected to register the fastest CAGR of 7.67% during the forecast period. This segment is majorly driven by applications of soy protein, with a share of 40.4% in 2020. It is also anticipated to be the fastest-growing protein type in the segment, with a CAGR of 8.83% during the forecast period. Consumers are shifting toward vegan sports nutrition products to improve performance and have healthier, more sustainable lifestyles. In the United Kingdom, 62% of sports nutrition users in 2021 believed that sports nutrition products made with plant proteins are healthier.

- Plant proteins hold a significant share of the animal feed industry, projected to register a growth of 2.61%, by value, in the forecast period. The UK feed industry imports more than 70% of its maize, soy, and rapeseed requirements annually. At least 90% of soy in the country is fed to animals, and, at most, 10% is used for food yearly. Soy protein is majorly fed to livestock, especially beef, chicken, egg, and dairy production.

United Kingdom Plant Protein Market Trends

The growth of plant protein consumption fuels opportunities for key players in the ingredients segment

- The recommended intake of proteins for adults in good health is 0.83 g/kg/d. The average intake of protein consumption ranges from 0.83 to 2.2 g/kg/d for an adult under 60 years of age. The average daily intake of proteins for adult women is 74 g, and for adult men, it is 100 g. Millennials and Gen Z are particularly driving the growing demand for plant-based diets and supplements. This is primarily because plant-based proteins are rapidly becoming the only source of all the essential amino acids that can replace animal protein. The protein segment's emergence can potentially reduce the environmental impact associated with the country's reliance on animal protein.

- The top users of plant-based foods are young and urban customers who believe consuming less meat is better for their health and the environment. An increasing number of people in the United Kingdom are expected to give up meat or adopt a vegetarian or vegan diet in the coming year. The UK government promotes a healthy lifestyle and diet among its consumers. This offers an opportunity for the soy protein ingredient, which is considered organic, pure, and healthful. The per capita consumption of soy protein favorably increased by 4.6% in 2022 from 2016.

- In the United Kingdom, the average amount of rice consumed per person per week from 2019 to 2020 was 111 grams. Rice contains essential nutrients such as thiamine, riboflavin, niacin, vitamin E, zinc, potassium, iron, and fiber. The average British citizen consumes about 5.6 kg of rice annually, with white rice accounting for 80% of purchases. Due to the country's expanding ethnic population and increased dietary variety, rice consumption in the United Kingdom is anticipated to increase significantly.

The United Kingdom is concentrating on enhancing its wheat and pea production capabilities

- The graph depicts the production data for raw materials such as dry peas, rice, wheat, and soya beans produced in the United Kingdom. The country is the key producer of wheat and peas. In 2021, the volume of wheat produced reached approximately 14 million metric ton, aided by regular rainfall and the temperate climate. Similarly, the fall planting conditions of the previous year were considerably better, resulting in a better wheat yield in 2020, thereby encouraging further winter wheat planting over spring crops like barley. In terms of pea production, the country is 90% self-sufficient.

- The country's unfavorable environment and concomitant harvesting issues restrict soy production. However, the rising demand from the food and animal feed sectors has piqued the interest of farmers, significantly increasing the crop's potential in the United Kingdom. In 2021, the total croppable area increased by 0.5% to 6.1 million hectares, boosting soy production.

- In increasing numbers, consumers purchase plant-based foods, especially protein alternatives in the meat and dairy aisles. Sales of meat alternatives, in particular, have jumped by 60% over the past two years, driven by better tastes and the wider availability of products. Currently, 14% of adults in the United Kingdom (7.2 million) follow a meat-free diet. A further 8.8 million people planned to go meat-free in 2022 (the highest figure in four years). As a result, the production of soy species is increasing in line with the adequate climate conditions in the United Kingdom. In the 12 months ending June 2022, soybean imports amounted to about 688 thousand metric tons, higher than the previous year's data.

United Kingdom Plant Protein Industry Overview

The United Kingdom Plant Protein Market is fragmented, with the top five companies occupying 37.46%. The major players in this market are Archer Daniels Midland Company, Cargill Incorporated, Ingredion Incorporated, International Flavors & Fragrances Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Hemp Protein

- 4.1.2 Pea Protein

- 4.1.3 Potato Protein

- 4.1.4 Rice Protein

- 4.1.5 Soy Protein

- 4.1.6 Wheat Protein

- 4.1.7 Other Plant Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Cargill Incorporated

- 5.4.4 Ingredion Incorporated

- 5.4.5 International Flavors & Fragrances Inc.

- 5.4.6 Kerry Group PLC

- 5.4.7 Lantmannen

- 5.4.8 Roquette Frere

- 5.4.9 Tereos SCA

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 214 Pages

- 納期

- 2~3営業日