中国の植物性たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

China Plant Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683500

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

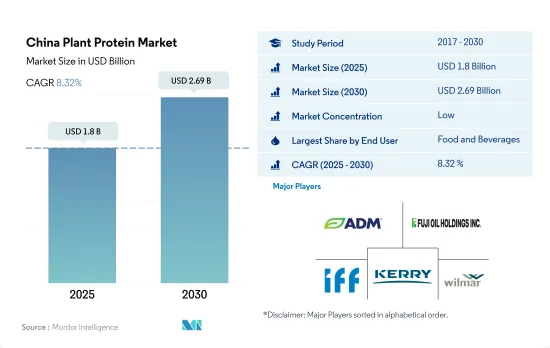

中国の植物性たんぱく質市場規模は2025年に18億米ドルと推定・予測され、2030年には26億9,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは8.32%で成長すると予測されています。

植物性たんぱく質に関連する健康上の利点が、特に動物飼料と飲食料品分野での応用を促進しました。

- 2022年の植物性たんぱく質の用途別セグメントでは、動物飼料が52.51%の主要数量シェアを占め、飲食品セグメントが52.51%の数量シェアで続きます。また、動物飼料は、予測期間(2023-2029年)の金額ベースのCAGRが9.10%で、中国の植物たんぱく質市場で最も急成長しているセグメントになると予測されています。消費者の嗜好がこれらのたんぱく質にシフトしていることが、植物たんぱく質を強化した製品を革新するメーカーに強く影響しています。増大する需要に対応し、顧客の増大するニーズに応えるために、国内では製品の発売が行われています。

- 飲食品セクターにおけるたんぱく質需要は、主にたんぱく質機能に対する需要の増加や高たんぱく質食に対する認識といった要因によって牽引されています。飲食品分野では、国内の消費者の間で菜食主義の傾向が高まっていることから、2020年には食肉代替品サブセグメントが48.4%増、次いで乳製品・乳製品代替品サブセグメントが22.4%増となりました。肉/鶏肉/シーフードおよび肉代替食品サブセグメントは、予測期間中、飲食品セグメントの中で金額ベースで最も速いCAGR 7.07%を記録すると予想されます。

- 中国の植物性たんぱく質市場は、2020年に金額ベースで13.98%の最高の前年比成長率を示しました。COVID-19の大流行により、人々は栄養価の高い菜食主義を選びました。例えば、2020年には2億人以上が菜食主義を実践し、その数は2016年から最も多くなりました。しかし、嗜好が小食にシフトし、伝統的な食事をより健康的で便利な選択肢に置き換えるため、エンドウ豆たんぱく質の売上は2020年に急増しました。

中国の植物性たんぱく質市場の動向

植物性食肉の人気の高まりが消費の増加に寄与する見込み

- グラフにはエンドウ(乾燥)、コメ、大豆、小麦の生産データを含みます。植物性たんぱく質は中国でますます受け入れられつつあります。植物性たんぱく質の認知度は2021年には90%に達します。中国の消費者の50%以上が国内のニュースソースから、48%がソーシャルメディアから植物性たんぱく質の情報を得ています。食肉業界における様々な植物性たんぱく質の使用量は、植物性食肉製品に対する消費者の受け入れが国内で高まっているため、大幅に増加しています。加工肉の頻繁な摂取は、心血管疾患のリスクを増加させ、死亡率を引き起こす可能性があるため、食肉産業における植物性たんぱく質の使用の増加につながります。逆に、全粒穀物、豆類、ナッツ類の摂取量が多ければ、飽和脂肪酸や食事性コレステロールが少ないため、心血管に良い影響を与えます。

- 中国のエンドウ豆プロテイン事業も、主に世界の食品セクターにおけるたんぱく質需要の高まりに後押しされ、活況を呈しています。中国の一人当たりエンドウ豆消費量は、2017年の60.3gから2022年には68.9gに増加します。しかし、欧州連合や米国とは異なり、中国におけるエンドウ豆たんぱく質の応用分野は限られています。ヘルスケア食品産業が中国におけるエンドウたんぱく質の大半を消費しているが、食品加工産業における用途はまだ研究開発段階にあります。

- 飼料価格の上昇、貿易摩擦、COVID-19の発生が2021年の国際貿易に不確実性をもたらしているため、中国の大手養豚業者および飼料原料生産業者は、大豆粕への依存度を下げるために大豆粕をあまり使用していないです。中国最大の飼料原料生産者であるニューホープ六和は、2021年4月末現在、農場の飼料に10%の大豆ミールを使用している(2019年は13.2%、2020年は12.5%)。

中国は世界トップの小麦生産国になると推定される

- グラフは、エンドウ豆(乾燥)、米、大豆、小麦などの植物性たんぱく質源を考慮したものです。中国は世界最大の小麦生産国で、2,400万haの面積で年間約1億2,600万トンを生産しています。小麦は中国の黄河流域と淮河流域で広く栽培されており、トウモロコシと輪作しています。長江流域とその周辺では、コメとの輪作がより一般的です。

- また、中国は世界有数のコメ生産国であり、今後も世界の生産量を独占する可能性があります。中国は2025年までに世界トップの小麦生産国となり、主食用穀物をほぼ自給するようになると推定されています。米国農務省外務局(FAS)は、中国の小麦生産量は2021年から2022年にかけて1億3,600万トンに達すると見積もっていたが、小麦生産量は1.6%増の1億3,359万トンに達しました。中国統計局は、全国でより多くの高品質小麦が作付けされたと発表しました。米の生産には政府の政策が重要な役割を果たしています。国内市場の自由化と、生産性投資(研究開発、灌漑の拡大、その他のインフラ整備など)による自給米政策が行われてきました。これらは今後も、コメ分野における中国の主要な国策であり続けるかもしれないです。

- オーツ麦は穀物の中で生産量第10位にランクされ、中国の18の省・地域で栽培されている重要な飼料作物です。アベナの野生種や栽培種はいくつか存在するが、主要な2種は6倍体の籾殻付きオート麦と裸麦(Avena sativa L.)です。中国は世界有数のオート麦生産国で、年間収穫面積は35万ヘクタール、収穫量は46万5千トン、平均収穫量は1ヘクタール当たり1.33トンです。

中国の植物性たんぱく質業界の概要

中国の植物性たんぱく質市場は細分化されており、上位5社で14.67%を占めています。この市場の主要企業は以下の通りです。Archer Daniels Midland Company, Fuji Oil Group, International Flavors & Fragrances Inc., Kerry Group PLC and Wilmar International Ltd(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- プロテインタイプ

- ヘンプたんぱく質

- エンドウ豆たんぱく質

- ポテトたんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Archer Daniels Midland Company

- Foodchem International Corporation

- Fuji Oil Group

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- Roquette Freres

- Shandong Jianyuan Bioengineering Co. Ltd

- Shandong Qufeng Food Technology Co. Ltd

- Shandong Yuwang Industrial Co. Ltd

- Wilmar International Ltd

- Wuxi Jinnong Biotechnology Co. Ltd

- Yantai Shuangta Food Co. Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The China Plant Protein Market size is estimated at 1.8 billion USD in 2025, and is expected to reach 2.69 billion USD by 2030, growing at a CAGR of 8.32% during the forecast period (2025-2030).

Heath benefits associated with plant protein drove the application especially in animal feed and F&B sector

- Animal feed was the leading segment, by application, for plant protein in the region, accounting for a major volume share of 52.51%, followed by the food and beverages segment, with a 52.51% volume share, in 2022. Animal feed is also projected to be the fastest-growing segment in the Chinese plant proteins market, with a CAGR of 9.10% by value during the forecast period (2023-2029). Consumer preferences shifting toward these proteins strongly influences manufacturers to innovate products enriched with plant proteins. Product launches have been taking place in the country to cater to the growing demand and meet the increasing needs of customers.

- The demand for proteins in the food and beverage sector is mainly driven by factors such as increasing demand for protein functions and awareness of high-protein diets. In the food and beverage segment, the meat alternative products sub-segment grew by 48.4%, followed by the dairy and dairy alternatives sub-segment (22.4%) in 2020 due to the rising trend of veganism among consumers in the country. The meat/poultry/seafood and meat alternatives sub-segment is expected to register the fastest CAGR of 7.07% within the food and beverage segment, by value, during the forecast period.

- The Chinese plant proteins market witnessed the highest Y-o-Y growth rate of 13.98% by value in 2020. Due to the COVID-19 pandemic, people opted for vegan diets with high nutrition. For instance, more than 200 million people followed a vegan diet in 2020, the highest number from 2016. However, the sales of pea proteins spiked in 2020 due to preferences shifting toward smaller meals and substituting traditional diets with healthier and more convenient options.

China Plant Protein Market Trends

The growing popularity of plant-based meat is expected to contribute to an increase in consumption

- Peas (dry), rice, soybeans, and wheat production data are included in the graph. Plant-based proteins are increasingly gaining acceptance in China. The awareness of plant-based protein reached 90% in 2021. More than 50% of Chinese consumers get plant-based protein information from domestic news sources, and 48% get it from social media. The usage of various plant proteins in the meat industry is increasing substantially due to the country's rising consumer acceptance of plant-based meat products. Frequent consumption of processed meat can increase the risk of cardiovascular diseases and cause mortality, thus leading to the growth of the use of plant proteins in the meat industry. On the contrary, a higher intake of whole grains, legumes, and nuts is associated with cardiovascular benefits as they have less saturated fatty acids and dietary cholesterol.

- China's pea protein business is also booming, primarily fueled by the rising demand for protein in the global food sector. The per capita consumption of peas in China increased from 60.3 g in 2017 to 68.9 g in 2022. However, unlike in the European Union and the United States, the application sectors of pea protein in China are limited. The healthcare food industry consumes the majority of pea protein in China, while applications in the food processing industry are still in the R&D stage.

- Due to rising feed prices, trade tensions, and the COVID-19 outbreak raising uncertainty for international trade in 2021, China's leading hog and feedstock producers used lesser soybean meal to decrease the country's reliance on the crop. The largest producer of feedstock in China, New Hope Liuhe, used 10% soybean meal in farm feed as of the end of April 2021, as opposed to 13.2% in 2019 and 12.5% in 2020.

China is estimated to become the world's top wheat producer

- The graph considers plant protein sources such as peas (dry), rice, soybeans, and wheat. China is the world's largest wheat producer, producing around 126 million metric tons per year on an area of 24 million ha. Wheat is cultivated extensively in the Yellow River and Huai River Valleys of China, rotating with maize. It is more commonly rotated with rice along and around the Yangtze River Valley.

- China is also one of the major rice producers in the world and may continue to dominate global production. China is estimated to become the world's top wheat producer and almost self-sufficient in staple grains by 2025. The US Department of Agriculture's Foreign Services (FAS) estimated that China's wheat production would reach 136 million metric ton during 2021-2022, but wheat production grew by 1.6% to reach 133.59 million metric ton. The China Statistics Bureau stated that more high-quality wheat had been planted nationwide. Government policy plays a vital role in rice production. Domestic market liberalization and self-sufficient rice policies through productivity investments (e.g., R&D, irrigation expansion, and other infrastructure) have been. They may continue to be China's major national policies in the rice sector.

- Oats rank 10th among cereals in terms of production, and they are an important fodder crop in the nation, grown in 18 provinces and regions in China. Although several wild and cultivated Avena species exist, the two major types are hexaploid hulled and naked oats (Avena sativa L.). China is one of the major oat-producing countries in the world, with an annual harvested area of 350,000 ha, 465,000 tons, and an average yield of 1.33 tons per ha.

China Plant Protein Industry Overview

The China Plant Protein Market is fragmented, with the top five companies occupying 14.67%. The major players in this market are Archer Daniels Midland Company, Fuji Oil Group, International Flavors & Fragrances Inc., Kerry Group PLC and Wilmar International Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 China

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Hemp Protein

- 4.1.2 Pea Protein

- 4.1.3 Potato Protein

- 4.1.4 Rice Protein

- 4.1.5 Soy Protein

- 4.1.6 Wheat Protein

- 4.1.7 Other Plant Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Foodchem International Corporation

- 5.4.3 Fuji Oil Group

- 5.4.4 International Flavors & Fragrances Inc.

- 5.4.5 Kerry Group PLC

- 5.4.6 Roquette Freres

- 5.4.7 Shandong Jianyuan Bioengineering Co. Ltd

- 5.4.8 Shandong Qufeng Food Technology Co. Ltd

- 5.4.9 Shandong Yuwang Industrial Co. Ltd

- 5.4.10 Wilmar International Ltd

- 5.4.11 Wuxi Jinnong Biotechnology Co. Ltd

- 5.4.12 Yantai Shuangta Food Co. Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日