|

|

市場調査レポート

商品コード

1620024

自動車用LED照明市場- 世界の産業規模、シェア、動向、機会、予測、ポジション別、車種別、アダプティブ照明別、地域別、競合別、2019年~2029年Automotive LED Lighting Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, Segmented By Position, By Vehicle Type, By Adaptive Lighting, By Region & Competition, 2019-2029F |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用LED照明市場- 世界の産業規模、シェア、動向、機会、予測、ポジション別、車種別、アダプティブ照明別、地域別、競合別、2019年~2029年 |

|

出版日: 2024年12月20日

発行: TechSci Research

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

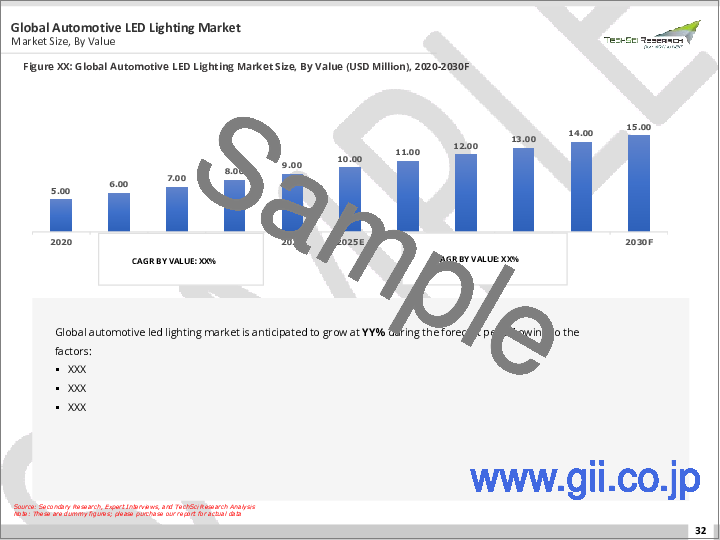

自動車用LED照明の世界市場規模は、2023年に157億米ドルとなり、2029年には219億5,000万米ドルに達すると予測され、2029年までの予測期間のCAGRは5.80%で成長すると予測されています。

自動車用LED照明市場は、技術の進歩、電気自動車(EV)の普及拡大、エネルギー効率の高いソリューションに対する需要の高まりなどを背景に、過去数年間で大幅な成長を遂げてきました。LEDは、その優れたエネルギー効率、長寿命、視認性の向上により、従来のハロゲンライトやキセノンライトに取って代わりつつあり、交通安全の向上に貢献しています。メーカー各社は、アダプティブヘッドライト、マトリックスLEDライト、OLED(有機発光ダイオード)照明といった最先端の自動車用LED技術の開発に多額の投資を行っており、配光制御の向上と車両の美観の向上を実現しています。

| 市場概要 | |

|---|---|

| 予測期間 | 2025-2029 |

| 市場規模:2023年 | 157億米ドル |

| 市場規模:2029年 | 219億5,000万米ドル |

| CAGR:2024年~2029年 | 5.80% |

| 急成長セグメント | フロント・アダプティブ・ライティング |

| 最大市場 | アジア太平洋 |

環境への関心が高まるにつれ、自動車企業は持続可能性を重視するようになり、LED照明ソリューションへのシフトを促しています。LEDは消費電力を大幅に削減できるため、バッテリー寿命の節約が最優先される電気自動車の性能と効率にとって極めて重要です。さらに、自律走行車やコネクテッドカー技術の動向は、高度な照明システムの需要にさらに拍車をかけています。自律走行車は、より良いナビゲーションと周辺環境との相互作用のために洗練された照明システムに依存しており、機能的かつ視覚的に印象的な新しい照明アプリケーションと設計への道を開いています。同市場はまた、スマート照明システムの継続的な進化によってもたらされる様々な機会も提供しています。自動車用LEDをスマートセンサーや制御システムと統合することで、車速、天候、道路の種類に基づいて調整するアダプティブ照明が可能になります。このような技術革新は、性能の向上、エネルギー効率の改善、車両所有者のカスタマイズ性を高める。こうした成長の原動力にもかかわらず、LED技術の初期コストの高さや高度な照明システムの製造の複雑さといった課題も残っています。さらに、車両におけるLED照明の使用を規定する業界標準や規制の開発はまだ進行中であり、世界市場全体で製品を標準化しようとするメーカーにとってハードルとなっています。

主な市場促進要因

エネルギー効率に対する需要の高まり

より安全な照明基準への規制強化

電気自動車と自律走行車の台頭

美的魅力の向上とカスタマイズ

安全機能とADAS(先進運転支援システム)の強化

技術の進歩とコスト効率

主な市場課題

LED技術の初期コストの高さ

技術の複雑さと統合の課題

熱管理と耐久性への懸念

モデル間の標準化と互換性

消費者の認識と教育

主要市場動向

高度な照明機能の採用増加

車内照明と車外照明のLED化

電気自動車と自律走行車の台頭

持続可能性の重視の高まり

カスタマイズとブランド差別化

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 COVID-19が世界の自動車用LED照明市場に与える影響

第5章 世界の自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別(フロント、リア、サイド、インテリア)

- 車種別(乗用車、商用車)

- アダプティブ照明(フロントアダプティブ照明、リアアダプティブ照明、アンビエントアダプティブ照明)

- 地域別

- 企業別(上位5社、その他- 価値別、2023年)

- 世界の自動車用LED照明市場マッピング&機会評価

- ポジション別

- 車種別

- アダプティブ照明

- 地域別

第6章 アジア太平洋の自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別

- 車種別

- アダプティブ照明

- 国別

- アジア太平洋地域:国別分析

- 中国

- インド

- 日本

- インドネシア

- タイ

- 韓国

- オーストラリア

第7章 欧州・CISの自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別

- 車種別

- アダプティブ照明

- 国別

- 欧州・CIS:国別分析

- ドイツ

- スペイン

- フランス

- ロシア

- イタリア

- 英国

- ベルギー

第8章 北米の自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別

- 車種別

- アダプティブ照明

- 国別

- 北米:国別分析

- 米国

- メキシコ

- カナダ

第9章 南米の自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別

- 車種別

- アダプティブ照明

- 国別

- 南米:国別分析

- ブラジル

- コロンビア

- アルゼンチン

第10章 中東・アフリカの自動車用LED照明市場展望

- 市場規模・予測

- 金額別

- 市場シェア・予測

- ポジション別

- 車種別

- アダプティブ照明

- 国別

- 中東・アフリカ:国別分析

- 南アフリカ

- トルコ

- サウジアラビア

- アラブ首長国連邦

第11章 SWOT分析

- 強み

- 弱み

- 機会

- 脅威

第12章 市場力学

- 市場促進要因

- 市場の課題

第13章 市場動向と発展

第14章 競合情勢

- 企業プロファイル(主要10社まで)

- OSRAM GmbH

- HELLA GmbH & Co. KGaA

- Koito Manufacturing Co., Ltd

- Stanley Electric Co., Ltd

- Koninklijke Philips N.V.

- Valeo SA

- Imasen Electric Industrial Co., Ltd.

- Texas Instruments Incorporated

- Nichia Corporation

- General Electric Company

第15章 戦略的提言

- 主要な重点分野

- 対象地域

- ターゲット位置

- 対象車種

第16章 調査会社について・免責事項

Global Automotive LED Lighting Market was valued at USD 15.7 Billion in 2023 and is anticipated to reach USD 21.95 Billion by 2029, growing in the forecast period with a CAGR of 5.80% through 2029. The automotive LED lighting market has witnessed substantial growth over the past few years, driven by advancements in technology, the growing adoption of electric vehicles (EVs), and the increasing demand for energy-efficient solutions. LEDs are rapidly replacing traditional halogen and xenon lights due to their superior energy efficiency, longer lifespan, and ability to provide enhanced visibility, contributing to improved road safety. Manufacturers are investing heavily in the development of cutting-edge automotive LED technologies such as adaptive headlights, matrix LED lights, and OLED (Organic Light Emitting Diode) lighting, which offer better control of light distribution and improved vehicle aesthetics.

| Market Overview | |

|---|---|

| Forecast Period | 2025-2029 |

| Market Size 2023 | USD 15.7 Billion |

| Market Size 2029 | USD 21.95 Billion |

| CAGR 2024-2029 | 5.80% |

| Fastest Growing Segment | Front Adaptive Lighting |

| Largest Market | Asia-Pacific |

As environmental concerns rise, automotive companies are increasingly focusing on sustainability, encouraging the shift towards LED lighting solutions. LEDs consume significantly less power, which is crucial for the performance and efficiency of electric vehicles, where conserving battery life is a top priority. Moreover, the growing trend of autonomous vehicles and connected car technologies is further spurring the demand for advanced lighting systems. Autonomous vehicles rely on sophisticated lighting systems for better navigation and interaction with the surrounding environment, paving the way for new lighting applications and designs that are both functional and visually striking. The market also presents various opportunities driven by the continuous evolution of smart lighting systems. Integration of automotive LEDs with smart sensors and control systems allows for adaptive lighting that adjusts based on vehicle speed, weather conditions, and road types. Such innovations offer better performance, improved energy efficiency, and greater customization for vehicle owners. Despite these growth drivers, challenges like the high initial cost of LED technologies and the complexity of manufacturing advanced lighting systems remain. Furthermore, the development of industry standards and regulations to govern the use of LED lights in vehicles is still a work in progress, presenting hurdles for manufacturers looking to standardize products across the global market.

Key Market Drivers

Rising Demand for Energy Efficiency

Energy efficiency remains a key driver in the automotive LED lighting market. As vehicles, especially electric ones, require energy-efficient components to extend battery life, LEDs have become the go-to choice for automotive lighting. Compared to traditional halogen and xenon lights, LEDs consume less power while providing higher light output and longer lifespan, reducing the frequency of replacements. This energy-saving feature not only enhances vehicle performance but also aligns with global efforts to minimize energy consumption and reduce the overall carbon footprint of the automotive sector. With increasing concerns about environmental sustainability, manufacturers are prioritizing energy-efficient solutions, leading to higher demand for LEDs in the industry.

Regulatory Push for Safer Lighting Standards

Governments across the globe are tightening regulations surrounding road safety, directly impacting the growth of automotive LED lighting. LEDs offer enhanced safety features, such as brighter illumination, which significantly improves visibility at night and in adverse weather conditions. These regulatory pushes encourage automakers to incorporate advanced lighting technologies that meet stricter safety standards. In many cases, LEDs surpass the performance of traditional lighting options by providing more consistent light distribution, which helps in reducing accidents and improving road safety. As safety regulations evolve, LED lighting systems are becoming an essential component of vehicles to ensure compliance and consumer safety.

Rise of Electric and Autonomous Vehicles

The increasing adoption of electric and autonomous vehicles is another driver for the automotive LED lighting market. For electric vehicles (EVs), LEDs are essential because of their low power consumption, helping to preserve battery life while offering high performance. Autonomous vehicles, on the other hand, rely heavily on advanced lighting systems for better communication with their surroundings. Adaptive lighting systems, such as LED matrix headlights, help autonomous vehicles make precise navigation decisions, enabling them to adjust the intensity and direction of the light based on the environment. These vehicles demand precise, customizable, and energy-efficient lighting solutions, all of which are provided by automotive LED technologies.

Improved Aesthetic Appeal and Customization

The aesthetic appeal of LED lights is increasingly influencing consumer demand in the automotive sector. LEDs provide superior flexibility in design, allowing for innovative and visually striking lighting solutions that enhance a vehicle's exterior and interior appeal. Customization options, such as ambient lighting, RGB color controls, and signature lighting designs, are growing trends in the industry, particularly in premium and luxury vehicles. These customizable lighting systems allow car manufacturers to offer unique visual identities for their models. As consumers become more interested in personalized and stylish vehicle designs, the demand for advanced automotive lighting solutions, including LEDs, is expected to increase significantly.

Enhanced Safety Features and Advanced Driver Assistance Systems (ADAS)

The integration of enhanced safety features and Advanced Driver Assistance Systems (ADAS) in modern vehicles is a significant driver for the Global Automotive LED Lighting Market. LED technology allows for advanced lighting configurations, including adaptive lighting systems, matrix beam headlights, and dynamic turn signals. These features enhance visibility, improve road safety, and contribute to accident prevention.

LED headlights, in particular, provide a more natural and effective illumination of the road compared to traditional lighting technologies. Adaptive lighting systems adjust the direction and range of the headlights based on factors such as vehicle speed, steering input, and surrounding conditions, optimizing visibility and reducing glare for both drivers and pedestrians. The ability of LEDs to respond quickly to changing conditions makes them well-suited for incorporation into ADAS, reinforcing their role as a critical driver in the automotive lighting market.

In January 2024, Lumax Auto Technologies Ltd introduced its LED fog lamp projectors in India, designed to enhance road safety during foggy winter weather. The fog lamps offer color temperatures of 5800 Kelvin, 4300 Kelvin, and 3000 Kelvin for improved visibility and feature 80-watt LED chips for bright, energy-efficient performance. With their wide beam and sharp cutoff, these lamps effectively penetrate fog, rain, and dust, improving driver safety in challenging conditions.

Technological Advancements and Cost Efficiency

Continuous technological advancements in LED lighting technology contribute to its adoption in the automotive sector. Ongoing research and development efforts result in improved performance, increased efficiency, and cost reductions in LED manufacturing. As a result, the overall cost of producing LED lighting systems has decreased, making them more competitive and cost-effective for automotive manufacturers.

LEDs also offer a faster response time compared to traditional lighting technologies, providing an added advantage in terms of safety. The evolving landscape of automotive electronics and connectivity features further integrates LED lighting with intelligent systems, creating synergies with in-vehicle technologies. The convergence of LED technology with smart lighting solutions enhances the overall driving experience, making it a driver for the Global Automotive LED Lighting Market.

In April 2024, Aledia announced major advancements in microLED technology, setting new standards for both energy efficiency and color precision. The company achieved a global milestone with its compact microLEDs (less than 1.5µm), reaching an impressive External Quantum Efficiency (EQE) of over 32% and producing 320 milliwatts of visible light per watt of electrical power. These improvements boost energy efficiency and extend battery life, while also providing bright and vivid displays.

Key Market Challenges

Initial High Cost of LED Technology

A primary challenge for the Global Automotive LED Lighting Market is the initial high cost associated with LED technology. While LED lighting solutions offer energy efficiency, longevity, and design flexibility, the upfront cost of implementing LED systems in vehicles remains relatively higher than traditional lighting technologies, such as halogen or incandescent bulbs. The cost disparity poses a challenge for automotive manufacturers, particularly in cost-sensitive segments, as they weigh the benefits of LED technology against the initial investment required for its integration.

Despite advancements that have reduced manufacturing costs, the perception of LEDs as a premium lighting solution can impact consumer acceptance, affecting mass adoption. Striking a balance between affordability and the advantages of LED technology is crucial for market penetration and broader consumer adoption, requiring manufacturers to explore cost-effective production methods and economies of scale.

Technological Complexity and Integration Challenges

The increasing complexity of LED lighting systems presents a significant challenge for the Global Automotive LED Lighting Market. LED technology involves intricate electronics, thermal management systems, and control units to ensure optimal performance and longevity. The integration of advanced features such as adaptive lighting, dynamic turn signals, and matrix beam headlights adds to the complexity, requiring seamless coordination with other vehicle electronics and safety systems.

The incorporation of LED technology into the automotive landscape necessitates expertise in electronics and software integration. This complexity can pose challenges for both original equipment manufacturers (OEMs) and suppliers, especially those transitioning from traditional lighting technologies. Ensuring compatibility with existing vehicle architectures, addressing potential interference issues, and managing the overall integration process without compromising safety or performance are critical considerations in overcoming technological challenges in the adoption of LED lighting systems.

Heat Management and Durability Concerns

Heat management and durability are persistent challenges for the Global Automotive LED Lighting Market. While LEDs are renowned for their energy efficiency, they generate heat during operation, and efficient heat dissipation is crucial to maintaining performance and longevity. The compact spaces within automotive lighting assemblies pose challenges in managing heat effectively, and failure to address heat-related issues can lead to premature LED degradation and reduced lifespan.

External factors such as extreme temperatures, moisture, and vibrations in diverse driving conditions can impact the durability of LED lighting systems. Ensuring the resilience of LEDs to environmental stressors and developing effective heat dissipation solutions are essential for meeting the stringent performance and reliability expectations in the automotive industry. Overcoming heat management and durability concerns is imperative for establishing LED technology as a reliable and durable lighting solution in vehicles.

Standardization and Compatibility Across Models

The lack of standardized regulations and specifications for LED lighting in vehicles poses a challenge for the Global Automotive LED Lighting Market. While there are regulatory standards for basic lighting functions, the diverse range of LED features, designs, and configurations complicates the development of universal standards. This lack of standardization can lead to challenges in ensuring compatibility across different vehicle models and brands.

The absence of standardized testing methods and certification processes for advanced LED features, such as adaptive lighting, makes it challenging for manufacturers to demonstrate compliance with safety and performance standards consistently. Achieving uniformity in LED lighting specifications would facilitate smoother integration across various vehicle platforms, promote interoperability, and enhance consumer confidence in the reliability and safety of LED lighting systems.

Consumer Awareness and Education

Consumer awareness and education present challenges for the Global Automotive LED Lighting Market. While LED technology offers numerous benefits, including energy efficiency, longer lifespan, and enhanced safety features, consumer understanding of these advantages may vary. Some consumers may perceive LEDs primarily as an aesthetic feature rather than recognizing the broader benefits they bring to vehicle performance, efficiency, and safety.

Educating consumers about the advantages of LED lighting, including its impact on fuel efficiency, reduced carbon emissions, and enhanced visibility, is essential for fostering broader adoption. Manufacturers and industry stakeholders face the challenge of effectively communicating the value proposition of LED technology to consumers, dispelling misconceptions, and highlighting the long-term cost savings and environmental benefits associated with LED lighting systems.

Key Market Trends

Increasing Adoption of Advanced Lighting Features

A prominent trend in the Global Automotive LED Lighting Market is the increasing adoption of advanced lighting features in vehicles. Automotive manufacturers are leveraging LED technology to introduce innovative lighting solutions that go beyond traditional illumination. Adaptive lighting systems, matrix beam headlights, and dynamic turn signals are becoming commonplace, enhancing both safety and aesthetics. Adaptive lighting adjusts the direction and range of headlights based on driving conditions, improving visibility without causing glare for oncoming traffic. These advanced features not only contribute to road safety but also cater to consumer preferences for sophisticated and dynamic lighting solutions, driving the demand for LED technology.

As the automotive industry moves toward autonomous driving and connected vehicles, the integration of smart lighting solutions is gaining momentum. Intelligent LED systems can communicate with other vehicles, infrastructure, and sensors, providing enhanced visibility and safety in diverse driving scenarios. The trend toward advanced lighting features reflects the industry's commitment to improving the overall driving experience while meeting evolving safety standards and consumer expectations.

Integration of LEDs in Interior and Exterior Lighting

The integration of LEDs in both interior and exterior automotive lighting is a significant trend shaping the Global Automotive LED Lighting Market. LED technology is not limited to traditional applications such as headlights and taillights; it is increasingly being incorporated into interior lighting, ambient lighting, and other decorative elements. Interior LED lighting allows for customizable cabin illumination, creating a visually appealing and immersive driving environment.

Automakers are leveraging LED technology to enhance the overall aesthetics of vehicles, creating signature lighting designs that distinguish their brands. Exterior lighting, including daytime running lights (DRLs), brake lights, and turn signals, is now predominantly powered by LEDs due to their energy efficiency and design flexibility. This trend reflects the industry's recognition of LED lighting as a versatile solution that contributes to both functional and aesthetic aspects of vehicle design. In June 2021, Hyundai Mobis unveiled a cutting-edge 'lighting grille' technology, which incorporates LED lighting directly into the front grille of a vehicle. This novel design transforms the entire grille into a functional lighting element. The adaptive LED lighting technology featured in this system is highly versatile, supporting a range of functions such as autonomous driving mode, electric vehicle (EV) charging indication, welcome lighting, sound beat displays, and emergency warning signals.

Rise of Electric and Autonomous Vehicles

The rise of electric vehicles (EVs) and the development of autonomous driving technologies are influencing the Global Automotive LED Lighting Market. Electric vehicles, with their emphasis on energy efficiency, align seamlessly with the benefits offered by LED lighting. LED technology, known for its low power consumption, contributes to extending the driving range of electric vehicles while providing bright and efficient lighting solutions.

Autonomous vehicles, with their reliance on sensors and advanced driver assistance systems (ADAS), require sophisticated lighting systems to communicate with pedestrians and other road users. LEDs, with their rapid response time and dynamic control capabilities, play a crucial role in creating intuitive communication through lighting. The trend toward electric and autonomous vehicles is driving the demand for intelligent LED lighting systems that contribute to both safety and the unique requirements of these emerging vehicle technologies.

Growing Emphasis on Sustainability

Sustainability is a growing trend influencing the Global Automotive LED Lighting Market. LED technology inherently aligns with sustainability goals due to its energy efficiency and longer lifespan. As the automotive industry faces increasing pressure to reduce its environmental footprint, LED lighting solutions contribute to energy conservation and overall eco-friendliness. The trend is not only limited to the operational efficiency of LED lights but extends to the materials used in manufacturing.

Manufacturers are exploring sustainable materials for LED components, incorporating recyclable materials and environmentally friendly manufacturing processes. The emphasis on sustainability extends to the end-of-life considerations, promoting recyclability and responsible disposal practices for LED components. As eco-consciousness becomes a defining factor in consumer choices, the automotive industry is leveraging LED technology to demonstrate its commitment to sustainable practices.

Customization and Brand Differentiation

The trend of customization and brand differentiation through LED lighting is gaining prominence in the Global Automotive LED Lighting Market. LED technology allows for a high degree of customization in terms of color, intensity, and sequencing. Automotive manufacturers are capitalizing on this flexibility to create signature lighting designs that align with their brand identities. Customizable ambient lighting in vehicle interiors enables consumers to personalize their driving experiences, contributing to a sense of exclusivity.

Distinctive lighting signatures in headlights and taillights serve as a visual identifier for various automotive brands, enhancing brand recognition and differentiation. This trend is particularly evident in premium and luxury vehicle segments, where unique lighting designs contribute to the overall luxury and sophistication of the vehicle. As consumers increasingly prioritize personalization and brand affinity, LED lighting serves as a powerful tool for automakers to create memorable and recognizable visual identities.

Segmental Insights

Position Insights

The automotive LED lighting market is segmented by position, with key applications in the front, rear, side, and interior of vehicles. Each of these positions serves distinct functional and aesthetic purposes, contributing to the overall performance and design of modern vehicles.

Front lighting plays a critical role in vehicle safety and visibility. LED headlights and daytime running lights (DRLs) are designed to improve driver awareness, road visibility, and to signal the presence of the vehicle to others. In particular, LED headlights offer high-intensity light with reduced glare for other road users, enhancing safety during night-time and adverse weather conditions. The integration of adaptive lighting systems within front lighting is also gaining traction, where headlights adjust automatically based on speed, road curves, and weather, optimizing visibility without impairing other drivers' sightlines.

Rear lighting is another vital component of automotive LED applications. Tail lights, brake lights, and turn signals are now commonly using LED technology, offering enhanced brightness and quicker response times. The use of LEDs in rear lighting improves safety by ensuring other drivers can quickly recognize braking or signaling actions. Moreover, LED tail lights are more durable and consume less power, which makes them ideal for electric vehicles (EVs) where battery efficiency is paramount. Tail light designs are evolving, with automakers utilizing LEDs for innovative designs that add to the aesthetic appeal of the vehicle.

Side lighting focuses on enhancing vehicle visibility from the sides, particularly in low-light environments or while changing lanes. LED side markers or strip lights serve as clear indicators to other drivers, improving the safety of lane changes and maneuvers. These lighting systems also contribute to the vehicle's sleek design, often integrated into door handles, side mirrors, or side skirts to create a modern and stylish look.

Interior lighting has become increasingly important for both functionality and luxury. LED interior lighting is used to enhance the cabin ambiance, with adjustable lighting options that allow passengers to customize the mood of the vehicle. Common applications include dashboard lights, footwell lighting, and overhead lights, all of which benefit from LED technology's efficiency and long lifespan. These lights not only serve practical purposes, such as illuminating the controls and passenger areas but also contribute to the overall interior aesthetic, offering vehicles a more modern and premium feel.

Regional Insights

In 2023, the dominant region in the automotive LED lighting market was the Asia-Pacific, primarily driven by the rapid growth in automotive production, technological advancements, and a strong focus on electric vehicles (EVs). The region is home to major automotive manufacturers, both established and emerging, who are increasingly adopting LED lighting solutions in their vehicle designs. This trend is particularly evident in countries like China, Japan, and South Korea, where there is a high demand for energy-efficient lighting systems due to stringent environmental regulations and consumer preferences for high-performance and low-energy solutions.

The shift towards electric vehicles in Asia-Pacific is one of the key factors fueling the growth of automotive LED lighting. LEDs offer several benefits for electric vehicles, including lower energy consumption and longer lifespans, which are crucial for enhancing the overall performance and range of EVs. As governments in the region implement policies to promote the adoption of electric vehicles, manufacturers are integrating advanced LED lighting systems to align with the growing consumer demand for energy-efficient solutions. These lighting technologies not only contribute to battery life but also improve the aesthetic appeal and functionality of electric cars.

The region's automotive LED market is also benefiting from technological advancements in lighting systems. Innovations such as adaptive headlights, matrix LED lighting, and OLED lighting are gaining popularity, particularly in premium and luxury vehicles. These technologies offer enhanced safety, better light distribution, and improved road visibility, all of which are critical to meeting evolving consumer expectations and regulatory requirements. With the growing integration of connected and autonomous vehicle technologies, the demand for smarter and more dynamic lighting solutions is also on the rise in Asia-Pacific.

Furthermore, the region's large consumer base, particularly in China, has contributed to a significant increase in automotive production, which in turn drives the demand for LED lighting. As the automotive industry continues to expand in this region, the adoption of LED lighting systems across various vehicle segments, from economy cars to high-end models, is expected to grow. This growth is supported by local manufacturers who are focusing on cost-effective, energy-efficient lighting options to cater to a diverse range of consumer needs and preferences. The competitive landscape in Asia-Pacific encourages continual innovation, further propelling the market for automotive LED lighting in the region.

Key Market Players

- OSRAM GmbH

- HELLA GmbH & Co. KGaA

- Koito Manufacturing Co., Ltd

- Stanley Electric Co., Ltd

- Koninklijke Philips N.V.

- Valeo SA

- Imasen Electric Industrial Co., Ltd.

- Texas Instruments Incorporated

- Nichia Corporation

- General Electric Company

Report Scope:

In this report, the Global Automotive LED Lighting Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

Automotive LED Lighting Market, By Position:

- Front

- Rear

- Side

- Interior

Automotive LED Lighting Market, By Vehicle Type:

- Passenger Cars

- Commercial Vehicles

Automotive LED Lighting Market, By Adaptive Lighting:

- Front Adaptive Lighting

- Rear Adaptive Lighting

- Ambient Adaptive Lighting

Automotive LED Lighting Market, By Region:

- Asia-Pacific

- China

- India

- Japan

- Indonesia

- Thailand

- South Korea

- Australia

- Europe & CIS

- Germany

- Spain

- France

- Russia

- Italy

- United Kingdom

- Belgium

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East & Africa

- South Africa

- Turkey

- Saudi Arabia

- UAE

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Global Automotive LED Lighting Market.

Available Customizations:

Global Automotive LED Lighting Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Table of Contents

1. Introduction

- 1.1. Product Overview

- 1.2. Key Highlights of the Report

- 1.3. Market Coverage

- 1.4. Market Segments Covered

- 1.5. Research Tenure Considered

2. Research Methodology

- 2.1. Objective of the Study

- 2.2. Baseline Methodology

- 2.3. Key Industry Partners

- 2.4. Major Association and Secondary Sources

- 2.5. Forecasting Methodology

- 2.6. Data Triangulation & Validation

- 2.7. Assumptions and Limitations

3. Executive Summary

- 3.1. Market Overview

- 3.2. Market Forecast

- 3.3. Key Regions

- 3.4. Key Segments

4. Impact of COVID-19 on Global Automotive LED Lighting Market

5. Global Automotive LED Lighting Market Outlook

- 5.1. Market Size & Forecast

- 5.1.1. By Value

- 5.2. Market Share & Forecast

- 5.2.1. By Position Market Share Analysis (Front, Rear, Side and Interior)

- 5.2.2. By Vehicle Type Market Share Analysis (Passenger Cars, Commercial Vehicles)

- 5.2.3. By Adaptive Lighting Market Share Analysis (Front Adaptive Lighting, Rear Adaptive Lighting and Ambient Adaptive Lighting)

- 5.2.4. By Regional Market Share Analysis

- 5.2.4.1. Asia-Pacific Market Share Analysis

- 5.2.4.2. Europe & CIS Market Share Analysis

- 5.2.4.3. North America Market Share Analysis

- 5.2.4.4. South America Market Share Analysis

- 5.2.4.5. Middle East & Africa Market Share Analysis

- 5.2.5. By Company Market Share Analysis (Top 5 Companies, Others - By Value, 2023)

- 5.3. Global Automotive LED Lighting Market Mapping & Opportunity Assessment

- 5.3.1. By Position Market Mapping & Opportunity Assessment

- 5.3.2. By Vehicle Type Market Mapping & Opportunity Assessment

- 5.3.3. By Adaptive Lighting Market Mapping & Opportunity Assessment

- 5.3.4. By Regional Market Mapping & Opportunity Assessment

6. Asia-Pacific Automotive LED Lighting Market Outlook

- 6.1. Market Size & Forecast

- 6.1.1. By Value

- 6.2. Market Share & Forecast

- 6.2.1. By Position Market Share Analysis

- 6.2.2. By Vehicle Type Market Share Analysis

- 6.2.3. By Adaptive Lighting Market Share Analysis

- 6.2.4. By Country Market Share Analysis

- 6.2.4.1. China Market Share Analysis

- 6.2.4.2. India Market Share Analysis

- 6.2.4.3. Japan Market Share Analysis

- 6.2.4.4. Indonesia Market Share Analysis

- 6.2.4.5. Thailand Market Share Analysis

- 6.2.4.6. South Korea Market Share Analysis

- 6.2.4.7. Australia Market Share Analysis

- 6.3. Asia-Pacific: Country Analysis

- 6.3.1. China Automotive LED Lighting Market Outlook

- 6.3.1.1. Market Size & Forecast

- 6.3.1.1.1. By Value

- 6.3.1.2. Market Share & Forecast

- 6.3.1.2.1. By Position Market Share Analysis

- 6.3.1.2.2. By Vehicle Type Market Share Analysis

- 6.3.1.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.1.1. Market Size & Forecast

- 6.3.2. India Automotive LED Lighting Market Outlook

- 6.3.2.1. Market Size & Forecast

- 6.3.2.1.1. By Value

- 6.3.2.2. Market Share & Forecast

- 6.3.2.2.1. By Position Market Share Analysis

- 6.3.2.2.2. By Vehicle Type Market Share Analysis

- 6.3.2.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.2.1. Market Size & Forecast

- 6.3.3. Japan Automotive LED Lighting Market Outlook

- 6.3.3.1. Market Size & Forecast

- 6.3.3.1.1. By Value

- 6.3.3.2. Market Share & Forecast

- 6.3.3.2.1. By Position Market Share Analysis

- 6.3.3.2.2. By Vehicle Type Market Share Analysis

- 6.3.3.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.3.1. Market Size & Forecast

- 6.3.4. Indonesia Automotive LED Lighting Market Outlook

- 6.3.4.1. Market Size & Forecast

- 6.3.4.1.1. By Value

- 6.3.4.2. Market Share & Forecast

- 6.3.4.2.1. By Position Market Share Analysis

- 6.3.4.2.2. By Vehicle Type Market Share Analysis

- 6.3.4.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.4.1. Market Size & Forecast

- 6.3.5. Thailand Automotive LED Lighting Market Outlook

- 6.3.5.1. Market Size & Forecast

- 6.3.5.1.1. By Value

- 6.3.5.2. Market Share & Forecast

- 6.3.5.2.1. By Position Market Share Analysis

- 6.3.5.2.2. By Vehicle Type Market Share Analysis

- 6.3.5.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.5.1. Market Size & Forecast

- 6.3.6. South Korea Automotive LED Lighting Market Outlook

- 6.3.6.1. Market Size & Forecast

- 6.3.6.1.1. By Value

- 6.3.6.2. Market Share & Forecast

- 6.3.6.2.1. By Position Market Share Analysis

- 6.3.6.2.2. By Vehicle Type Market Share Analysis

- 6.3.6.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.6.1. Market Size & Forecast

- 6.3.7. Australia Automotive LED Lighting Market Outlook

- 6.3.7.1. Market Size & Forecast

- 6.3.7.1.1. By Value

- 6.3.7.2. Market Share & Forecast

- 6.3.7.2.1. By Position Market Share Analysis

- 6.3.7.2.2. By Vehicle Type Market Share Analysis

- 6.3.7.2.3. By Adaptive Lighting Market Share Analysis

- 6.3.7.1. Market Size & Forecast

- 6.3.1. China Automotive LED Lighting Market Outlook

7. Europe & CIS Automotive LED Lighting Market Outlook

- 7.1. Market Size & Forecast

- 7.1.1. By Value

- 7.2. Market Share & Forecast

- 7.2.1. By Position Market Share Analysis

- 7.2.2. By Vehicle Type Market Share Analysis

- 7.2.3. By Adaptive Lighting Market Share Analysis

- 7.2.4. By Country Market Share Analysis

- 7.2.4.1. Germany Market Share Analysis

- 7.2.4.2. Spain Market Share Analysis

- 7.2.4.3. France Market Share Analysis

- 7.2.4.4. Russia Market Share Analysis

- 7.2.4.5. Italy Market Share Analysis

- 7.2.4.6. United Kingdom Market Share Analysis

- 7.2.4.7. Belgium Market Share Analysis

- 7.3. Europe & CIS: Country Analysis

- 7.3.1. Germany Automotive LED Lighting Market Outlook

- 7.3.1.1. Market Size & Forecast

- 7.3.1.1.1. By Value

- 7.3.1.2. Market Share & Forecast

- 7.3.1.2.1. By Position Market Share Analysis

- 7.3.1.2.2. By Vehicle Type Market Share Analysis

- 7.3.1.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.1.1. Market Size & Forecast

- 7.3.2. Spain Automotive LED Lighting Market Outlook

- 7.3.2.1. Market Size & Forecast

- 7.3.2.1.1. By Value

- 7.3.2.2. Market Share & Forecast

- 7.3.2.2.1. By Position Market Share Analysis

- 7.3.2.2.2. By Vehicle Type Market Share Analysis

- 7.3.2.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.2.1. Market Size & Forecast

- 7.3.3. France Automotive LED Lighting Market Outlook

- 7.3.3.1. Market Size & Forecast

- 7.3.3.1.1. By Value

- 7.3.3.2. Market Share & Forecast

- 7.3.3.2.1. By Position Market Share Analysis

- 7.3.3.2.2. By Vehicle Type Market Share Analysis

- 7.3.3.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.3.1. Market Size & Forecast

- 7.3.4. Russia Automotive LED Lighting Market Outlook

- 7.3.4.1. Market Size & Forecast

- 7.3.4.1.1. By Value

- 7.3.4.2. Market Share & Forecast

- 7.3.4.2.1. By Position Market Share Analysis

- 7.3.4.2.2. By Vehicle Type Market Share Analysis

- 7.3.4.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.4.1. Market Size & Forecast

- 7.3.5. Italy Automotive LED Lighting Market Outlook

- 7.3.5.1. Market Size & Forecast

- 7.3.5.1.1. By Value

- 7.3.5.2. Market Share & Forecast

- 7.3.5.2.1. By Position Market Share Analysis

- 7.3.5.2.2. By Vehicle Type Market Share Analysis

- 7.3.5.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.5.1. Market Size & Forecast

- 7.3.6. United Kingdom Automotive LED Lighting Market Outlook

- 7.3.6.1. Market Size & Forecast

- 7.3.6.1.1. By Value

- 7.3.6.2. Market Share & Forecast

- 7.3.6.2.1. By Position Market Share Analysis

- 7.3.6.2.2. By Vehicle Type Market Share Analysis

- 7.3.6.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.6.1. Market Size & Forecast

- 7.3.7. Belgium Automotive LED Lighting Market Outlook

- 7.3.7.1. Market Size & Forecast

- 7.3.7.1.1. By Value

- 7.3.7.2. Market Share & Forecast

- 7.3.7.2.1. By Position Market Share Analysis

- 7.3.7.2.2. By Vehicle Type Market Share Analysis

- 7.3.7.2.3. By Adaptive Lighting Market Share Analysis

- 7.3.7.1. Market Size & Forecast

- 7.3.1. Germany Automotive LED Lighting Market Outlook

8. North America Automotive LED Lighting Market Outlook

- 8.1. Market Size & Forecast

- 8.1.1. By Value

- 8.2. Market Share & Forecast

- 8.2.1. By Position Market Share Analysis

- 8.2.2. By Vehicle Type Market Share Analysis

- 8.2.3. By Adaptive Lighting Market Share Analysis

- 8.2.4. By Country Market Share Analysis

- 8.2.4.1. United States Market Share Analysis

- 8.2.4.2. Mexico Market Share Analysis

- 8.2.4.3. Canada Market Share Analysis

- 8.3. North America: Country Analysis

- 8.3.1. United States Automotive LED Lighting Market Outlook

- 8.3.1.1. Market Size & Forecast

- 8.3.1.1.1. By Value

- 8.3.1.2. Market Share & Forecast

- 8.3.1.2.1. By Position Market Share Analysis

- 8.3.1.2.2. By Vehicle Type Market Share Analysis

- 8.3.1.2.3. By Adaptive Lighting Market Share Analysis

- 8.3.1.1. Market Size & Forecast

- 8.3.2. Mexico Automotive LED Lighting Market Outlook

- 8.3.2.1. Market Size & Forecast

- 8.3.2.1.1. By Value

- 8.3.2.2. Market Share & Forecast

- 8.3.2.2.1. By Position Market Share Analysis

- 8.3.2.2.2. By Vehicle Type Market Share Analysis

- 8.3.2.2.3. By Adaptive Lighting Market Share Analysis

- 8.3.2.1. Market Size & Forecast

- 8.3.3. Canada Automotive LED Lighting Market Outlook

- 8.3.3.1. Market Size & Forecast

- 8.3.3.1.1. By Value

- 8.3.3.2. Market Share & Forecast

- 8.3.3.2.1. By Position Market Share Analysis

- 8.3.3.2.2. By Vehicle Type Market Share Analysis

- 8.3.3.2.3. By Adaptive Lighting Market Share Analysis

- 8.3.3.1. Market Size & Forecast

- 8.3.1. United States Automotive LED Lighting Market Outlook

9. South America Automotive LED Lighting Market Outlook

- 9.1. Market Size & Forecast

- 9.1.1. By Value

- 9.2. Market Share & Forecast

- 9.2.1. By Position Market Share Analysis

- 9.2.2. By Vehicle Type Market Share Analysis

- 9.2.3. By Adaptive Lighting Market Share Analysis

- 9.2.4. By Country Market Share Analysis

- 9.2.4.1. Brazil Market Share Analysis

- 9.2.4.2. Argentina Market Share Analysis

- 9.2.4.3. Colombia Market Share Analysis

- 9.3. South America: Country Analysis

- 9.3.1. Brazil Automotive LED Lighting Market Outlook

- 9.3.1.1. Market Size & Forecast

- 9.3.1.1.1. By Value

- 9.3.1.2. Market Share & Forecast

- 9.3.1.2.1. By Position Market Share Analysis

- 9.3.1.2.2. By Vehicle Type Market Share Analysis

- 9.3.1.2.3. By Adaptive Lighting Market Share Analysis

- 9.3.1.1. Market Size & Forecast

- 9.3.2. Colombia Automotive LED Lighting Market Outlook

- 9.3.2.1. Market Size & Forecast

- 9.3.2.1.1. By Value

- 9.3.2.2. Market Share & Forecast

- 9.3.2.2.1. By Position Market Share Analysis

- 9.3.2.2.2. By Vehicle Type Market Share Analysis

- 9.3.2.2.3. By Adaptive Lighting Market Share Analysis

- 9.3.2.1. Market Size & Forecast

- 9.3.3. Argentina Automotive LED Lighting Market Outlook

- 9.3.3.1. Market Size & Forecast

- 9.3.3.1.1. By Value

- 9.3.3.2. Market Share & Forecast

- 9.3.3.2.1. By Position Market Share Analysis

- 9.3.3.2.2. By Vehicle Type Market Share Analysis

- 9.3.3.2.3. By Adaptive Lighting Market Share Analysis

- 9.3.3.1. Market Size & Forecast

- 9.3.1. Brazil Automotive LED Lighting Market Outlook

10. Middle East & Africa Automotive LED Lighting Market Outlook

- 10.1. Market Size & Forecast

- 10.1.1. By Value

- 10.2. Market Share & Forecast

- 10.2.1. By Position Market Share Analysis

- 10.2.2. By Vehicle Type Market Share Analysis

- 10.2.3. By Adaptive Lighting Market Share Analysis

- 10.2.4. By Country Market Share Analysis

- 10.2.4.1. South Africa Market Share Analysis

- 10.2.4.2. Turkey Market Share Analysis

- 10.2.4.3. Saudi Arabia Market Share Analysis

- 10.2.4.4. UAE Market Share Analysis

- 10.3. Middle East & Africa: Country Analysis

- 10.3.1. South Africa Automotive LED Lighting Market Outlook

- 10.3.1.1. Market Size & Forecast

- 10.3.1.1.1. By Value

- 10.3.1.2. Market Share & Forecast

- 10.3.1.2.1. By Position Market Share Analysis

- 10.3.1.2.2. By Vehicle Type Market Share Analysis

- 10.3.1.2.3. By Adaptive Lighting Market Share Analysis

- 10.3.1.1. Market Size & Forecast

- 10.3.2. Turkey Automotive LED Lighting Market Outlook

- 10.3.2.1. Market Size & Forecast

- 10.3.2.1.1. By Value

- 10.3.2.2. Market Share & Forecast

- 10.3.2.2.1. By Position Market Share Analysis

- 10.3.2.2.2. By Vehicle Type Market Share Analysis

- 10.3.2.2.3. By Adaptive Lighting Market Share Analysis

- 10.3.2.1. Market Size & Forecast

- 10.3.3. Saudi Arabia Automotive LED Lighting Market Outlook

- 10.3.3.1. Market Size & Forecast

- 10.3.3.1.1. By Value

- 10.3.3.2. Market Share & Forecast

- 10.3.3.2.1. By Position Market Share Analysis

- 10.3.3.2.2. By Vehicle Type Market Share Analysis

- 10.3.3.2.3. By Adaptive Lighting Market Share Analysis

- 10.3.3.1. Market Size & Forecast

- 10.3.4. UAE Automotive LED Lighting Market Outlook

- 10.3.4.1. Market Size & Forecast

- 10.3.4.1.1. By Value

- 10.3.4.2. Market Share & Forecast

- 10.3.4.2.1. By Position Market Share Analysis

- 10.3.4.2.2. By Vehicle Type Market Share Analysis

- 10.3.4.2.3. By Adaptive Lighting Market Share Analysis

- 10.3.4.1. Market Size & Forecast

- 10.3.1. South Africa Automotive LED Lighting Market Outlook

11. SWOT Analysis

- 11.1. Strength

- 11.2. Weakness

- 11.3. Opportunities

- 11.4. Threats

12. Market Dynamics

- 12.1. Market Drivers

- 12.2. Market Challenges

13. Market Trends and Developments

14. Competitive Landscape

- 14.1. Company Profiles (Up to 10 Major Companies)

- 14.1.1. OSRAM GmbH

- 14.1.1.1. Company Details

- 14.1.1.2. Key Product Offered

- 14.1.1.3. Financials (As Per Availability)

- 14.1.1.4. Recent Developments

- 14.1.1.5. Key Management Personnel

- 14.1.2. HELLA GmbH & Co. KGaA

- 14.1.2.1. Company Details

- 14.1.2.2. Key Product Offered

- 14.1.2.3. Financials (As Per Availability)

- 14.1.2.4. Recent Developments

- 14.1.2.5. Key Management Personnel

- 14.1.3. Koito Manufacturing Co., Ltd

- 14.1.3.1. Company Details

- 14.1.3.2. Key Product Offered

- 14.1.3.3. Financials (As Per Availability)

- 14.1.3.4. Recent Developments

- 14.1.3.5. Key Management Personnel

- 14.1.4. Stanley Electric Co., Ltd

- 14.1.4.1. Company Details

- 14.1.4.2. Key Product Offered

- 14.1.4.3. Financials (As Per Availability)

- 14.1.4.4. Recent Developments

- 14.1.4.5. Key Management Personnel

- 14.1.5. Koninklijke Philips N.V.

- 14.1.5.1. Company Details

- 14.1.5.2. Key Product Offered

- 14.1.5.3. Financials (As Per Availability)

- 14.1.5.4. Recent Developments

- 14.1.5.5. Key Management Personnel

- 14.1.6. Valeo SA

- 14.1.6.1. Company Details

- 14.1.6.2. Key Product Offered

- 14.1.6.3. Financials (As Per Availability)

- 14.1.6.4. Recent Developments

- 14.1.6.5. Key Management Personnel

- 14.1.7. Imasen Electric Industrial Co., Ltd.

- 14.1.7.1. Company Details

- 14.1.7.2. Key Product Offered

- 14.1.7.3. Financials (As Per Availability)

- 14.1.7.4. Recent Developments

- 14.1.7.5. Key Management Personnel

- 14.1.8. Texas Instruments Incorporated

- 14.1.8.1. Company Details

- 14.1.8.2. Key Product Offered

- 14.1.8.3. Financials (As Per Availability)

- 14.1.8.4. Recent Developments

- 14.1.8.5. Key Management Personnel

- 14.1.9. Nichia Corporation

- 14.1.9.1. Company Details

- 14.1.9.2. Key Product Offered

- 14.1.9.3. Financials (As Per Availability)

- 14.1.9.4. Recent Developments

- 14.1.9.5. Key Management Personnel

- 14.1.10. General Electric Company

- 14.1.10.1. Company Details

- 14.1.10.2. Key Product Offered

- 14.1.10.3. Financials (As Per Availability)

- 14.1.10.4. Recent Developments

- 14.1.10.5. Key Management Personnel

- 14.1.1. OSRAM GmbH

15. Strategic Recommendations

- 15.1. Key Focus Areas

- 15.1.1. Target Regions

- 15.1.2. Target Position

- 15.1.3. Target Vehicle Type