|

市場調査レポート

商品コード

1910574

冷凍ベーカリー市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Frozen Bakery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 冷凍ベーカリー市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

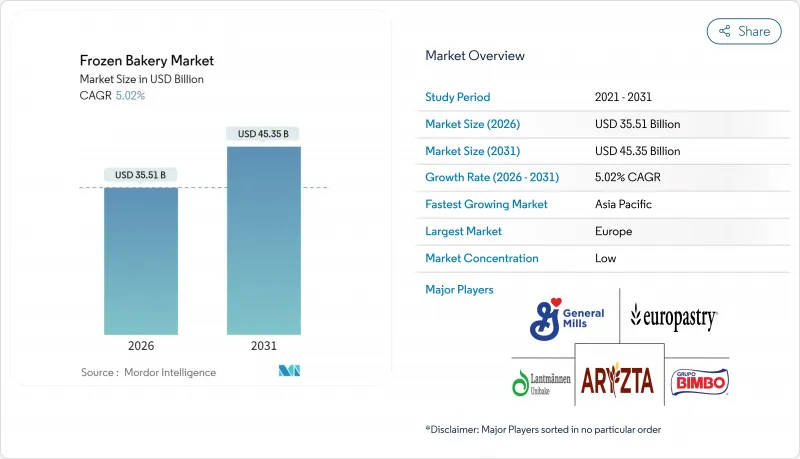

冷凍ベーカリー市場は、2025年に338億1,000万米ドルと評価され、2026年の355億1,000万米ドルから2031年までに453億5,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは5.02%と見込まれています。

現代的なライフスタイルの加速に伴い、消費者は家庭用・外食産業用を問わず、冷凍ベーカリー製品の利便性をますます選択しています。この成長は、コールドチェーンシステムの進歩、革新的な製品開発、調理が容易な食事への需要増加によって支えられています。さらに、エネルギー効率の高い生産技術と改善された電子商取引物流が、業界の長期的な競合力を強化しています。健康志向の高まりにより、グルテンフリー、全粒粉、低脂肪といった健康的な特性を備えた冷凍ベーカリー製品への関心が高まっています。欧州は強力な規制枠組みと職人的な製パンの伝統に支えられ、冷凍ベーカリー市場をリードしています。一方、アジア太平洋地域は急速なインフラ整備と食習慣の変化を背景に、最も速い成長を遂げています。パンが最大の製品カテゴリーである一方、ピザクラストはプレミアム成長セグメントとして台頭しています。市場は主に小売流通が占めておりますが、外食産業の回復により業務用需要も増加傾向にあります。競合激化に伴い、各社はコスト変動リスクの軽減策として、戦略的買収や再生可能エネルギー導入を含むポートフォリオ最適化と持続可能性への取り組みに注力しております。

世界の冷凍ベーカリー市場動向と洞察

手軽な持ち運び用冷凍スナックへの需要

消費者のライフスタイルが移動性や時間制約のある食事解決策へ移行する中、携帯可能な冷凍ベーカリー製品への持続的な需要が高まっています。Conagra Brands社の2024年冷凍食品動向分析によれば、朝食サンドイッチだけで米国市場で23億米ドルの売上を生み出しています。この成長は、移動性と時間節約型食事解決策を求める広範な消費者嗜好と一致しています。健康志向の消費者層は、一口サイズやミニサイズの製品への関心も高めており、これは摂取量の管理への意識の高まりを反映しています。このセグメントの拡大は、エアフライヤーの普及拡大によってさらに後押しされており、多くの冷凍食品パッケージには、食感の質を保ちながら素早く調理できるエアフライヤー用の調理方法が記載されるようになりました。人手不足に対応するため、特にコンビニエンスストアやクイックサービスレストランなどの外食産業では、メニューの多様性を維持するために冷凍スナックの選択肢を取り入れています。食習慣が定食からより頻繁で少量な食事機会へと移行する中、手軽に持ち運べる冷凍スナックへの需要は引き続き高まっています。国際食品情報評議会(IFIC)によれば、2024年には米国消費者の31%が1日2回スナックを摂取していました。こうしたスナック文化と冷凍技術の融合は、伝統的なベーカリー製品と現代の消費パターンを融合させた革新的な形態の創出機会を生み出しています。

ベーカリー製品の簡便な調理法への需要高まり

プロの厨房や小売ベーカリーでは、人手不足の解消と業務効率化のため、冷凍ソリューションの導入が増加しています。この変化により、小規模店舗でも専門的な製パン技術が不要な職人品質の製品を提供できるようになり、様々な小売形態で高品質なベーカリー商品へのアクセスが拡大しています。低温発酵技術の進歩は、発酵準備済み技術(RTD)の革新を促進し、ベーカリーが生産スケジュールを最適化し、発酵期間の延長を通じて風味プロファイルを向上させることを可能にしています。この動向は医療・施設給食サービス分野で加速しており、一貫した品質と食品安全性が求められる環境では、不安定な生鮮生産よりも標準化された冷凍ソリューションが優位です。戦略的環境は垂直統合の機会を浮き彫りにしており、冷凍ベーカリーメーカーは高利益率の小売パートナーシップを確保しつつ、従来型事業に影響を与える熟練職人の不足を緩和できます。さらに冷凍ベーカリー製品の消費拡大は、手間をかけずに高品質製品を入手できる利便性を求める消費者の需要増を反映しています。ドイツ冷凍食品協会によれば、ドイツにおける冷凍ベーカリー製品の消費量は、2023年の107万7,815トンから2024年には110万2,606トンへと増加しました。この市場変革は、主に現代的なライフスタイル、技術進歩、そして変化する消費者の嗜好によって推進されています。

生鮮品への消費者嗜好

職人的な製パンが文化的に重要視され、地元生産を優遇する規制枠組みが存在する欧州市場では、冷凍食品に対する強い抵抗感がみられます。新鮮さをプレミアム品質と結びつける富裕層の消費者が、この嗜好をさらに強化しています。その結果、冷凍ベーカリーメーカーはこうした高付加価値市場セグメントへの参入に困難を抱えています。この課題は価格圧力にも反映されており、消費者は生鮮品よりも冷凍品を選ぶ際に大幅な値引きを要求することが多いのです。こうした要因が利益率を圧迫し、プレミアムポジショニング戦略の妨げとなっています。しかしながら、冷凍技術の進歩と包装の革新により、特に利便性を重視する若い消費者層を中心に、こうした認識は徐々に変化しつつあります。これに対応するため、業界関係者は品質保持技術の透明性を強調する取り組みや、特定の用途における冷凍製品の利点を示す栄養研究などの戦略を実施しています。

セグメント分析

2025年、冷凍ベーカリー市場においてパン製品は41.72%という大きなシェアを占めました。これは小売・外食産業双方での高い認知度と適応性が背景にあります。ランカスター・コロニー社の「ニューヨーク・ベーカリー」ラインなど、プレミアムなグルテンフリー製品の導入は、特に健康志向の消費者層における「より良い代替品」を求めるニーズに応え、同カテゴリーの魅力をさらに高めています。この動向は、冷凍ベーカリー市場における主食としてのパン製品への持続的な需要を裏付けています。同時に、ピザクラストセグメントは主要な促進要因として台頭しており、2026年から2031年にかけて6.28%という高いCAGRを記録しています。この成長は、サステナビリティの潮流に沿ったアップサイクル素材の採用と、外食産業の回復によって推進されています。クイックサービスレストランでは、半焼き済みおよび冷凍からオーブンへ直接調理可能なピザクラストの採用が増加しています。これらは労働力最適化と職人のような質感を実現する二重の利点を提供し、冷凍ピザクラストの市場規模を拡大しています。

ケーキやペイストリーは、季節の祝祭時に特に需要が安定して続いております。一方、朝食用商品(モーニンググッズ)は朝食としての利便性から人気が高まっております。ヴィエノワズリーやデニッシュ製品は、特に顧客に本格的な欧州体験を提供しようとするホテルやカフェにおいて、プレミアム化動向を活かしております。冷凍ベーカリー市場では、2025年1月にフルラニ・フーズ社がコールズ・クオリティ・フーズ社を買収した事例が示す通り、統合が加速しています。この戦略的買収により、フルラニ・フーズ社は冷凍ガーリックブレッド分野における主導的地位を強化しました。製品ポートフォリオの多様化により、同社は規模の経済効果を高めるだけでなく、各カテゴリー間の需要変動の影響を緩和し、より強固な市場基盤を確保しています。

世界の冷凍ベーカリー市場レポートは、製品タイプ(パン、ピザクラスト、ケーキ・ペイストリー、モーニンググッズなど)、形態(調理用、焼成用、発酵用、即食用)、流通チャネル(外食産業向け、小売向け)、地域(北米、南米、欧州、アジア太平洋、中東・アフリカ)別に分類されています。市場予測は、金額(米ドル)および数量(トン)で提供されます。

地域別分析

欧州は2025年に36.20%の市場シェアを占めており、その背景には先進的なコールドチェーンインフラと支援的な規制枠組みがあります。これらの枠組みは冷凍食品のイノベーションを促進しており、2025年に施行されるEUの改訂汚染物質規制も含まれます。同規制は生産の柔軟性を維持しつつ食品安全基準の向上を目指しています。欧州の強い職人的製パンの伝統も、冷凍製品のプレミアムな位置付けに寄与しています。ヴァンデモーテル社などの企業は、イタリアのリッツィ社や北米のバネトンベーカリー社といった戦略的買収を通じて、この優位性を活用し、地理的展開と製品ラインの拡充を図っています。ドイツとフランスは、堅調な外食産業と冷凍便利食品に対する消費者の受容性を背景に、消費動向をリードしています。一方、英国市場は経済的課題にもかかわらず堅調さを維持しています。ISO食品安全基準などの規制枠組みを遵守する欧州メーカーは、国際的な拡大機会を追求する中で競争優位性を獲得しています。

アジア太平洋地域は急速な成長を遂げており、2026年から2031年にかけてCAGR6.44%という最高水準の拡大率を示しています。この成長は、大規模なインフラ投資と消費パターンの変化によって牽引されています。中国では、戦略的な買収を通じて市場成長が加速しています。例えば2024年9月には、モンデリーズ・インターナショナルが冷凍ケーキ・ペイストリー大手メーカーのイーバースを買収し、多国籍企業が中国の長期的な成長可能性に確信を持っていることを示しています。インドでは、コールドチェーンインフラへの投資と、便利な食品ソリューションを好む都市化の動向により市場が拡大しています。タイやインドネシアを含む東南アジア諸国も、可処分所得の増加と西洋的な食習慣の普及を背景に、強い成長可能性を示しています。

北米では、確立された流通網と冷凍便利食品への広範な消費者受容に支えられ、依然として強い市場存在感を維持しています。カナダでは、インフレに牽引された名目二桁成長率により、ベーカリー部門が堅調さを示しています。メキシコは米国市場への近接性と強固な製造能力の恩恵を受けています。グルーポ・ビンボはその好例であり、カリフォルニア州の施設における再生可能エネルギーマイクログリッドなど、広範な事業展開と持続可能性への取り組みを推進しています。南米では、ブラジルとアルゼンチンが都市化と所得増加を原動力に成長機会を牽引しております。2024年9月にグルーポ・ビンボがウィックボールドブランドを買収したことは、同社の多国籍展開戦略を浮き彫りにしております。一方、中東・アフリカ地域では、インフラ整備と食習慣の変化を背景に潜在的可能性が顕在化しつつあります。ただし、コールドチェーンの制約が短期的な成長見通しを依然として抑制しております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 手軽に食べられる冷凍スナックへの需要

- 長期保存性と小売廃棄物の削減

- 便利なベーカリー製品の需要増加

- 新興市場におけるコールドチェーン電子商取引

- 製品革新と品揃え

- 特製パンおよびヴィエノワズリーのプレミアム化

- 市場抑制要因

- 消費者の生鮮製品への嗜好

- 新興市場における冷蔵保管施設の不足

- 伝統的な製法への嗜好

- 小麦粉・エネルギー価格の変動が利益率を圧迫しております

- 消費者行動分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額と数量)

- 製品タイプ別

- パン

- ピザクラスト

- ケーキとペイストリー

- 朝食用商品(ドーナツ、マフィン、クロワッサン)

- ヴィエノワズリーとデニッシュ

- その他の冷凍ベーカリー製品

- 形態別

- 調理準備完了

- 焼成準備完了

- 発酵準備完了

- RTE(レディトゥイート)

- 流通チャネル別

- オントレード(ホレカ)

- オフトレード(小売)

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 専門店

- オンライン小売店

- その他のオフトレードチャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- スウェーデン

- ベルギー

- ポーランド

- オランダ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- シンガポール

- インドネシア

- 韓国

- オーストラリア

- ニュージーランド

- その他アジア太平洋

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Grupo Bimbo SAB de CV

- Aryzta AG

- Lantmannen Unibake International

- Europastry SA

- General Mills Inc.

- Associated British Foods PLC

- Conagra Brands Inc.

- Rich Products Corporation

- Vandemoortele NV

- Dawn Foods Global Inc.

- Tyson Foods Inc.(Sara Lee Frozen Bakery)

- Flowers Foods Inc.

- FGF Brands Inc.

- Alpha Baking Company Inc.

- Sunbulah Group

- Gonnella Frozen Products

- Fuji Baking Co. Ltd.

- Vandemoortele USA LLC

- Rotella's Italian Bakery Inc.

- Europastry USA

- Nestle SA(DiGiorno, Toll House cookie dough)