|

市場調査レポート

商品コード

1693997

米国のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)US Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 278 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

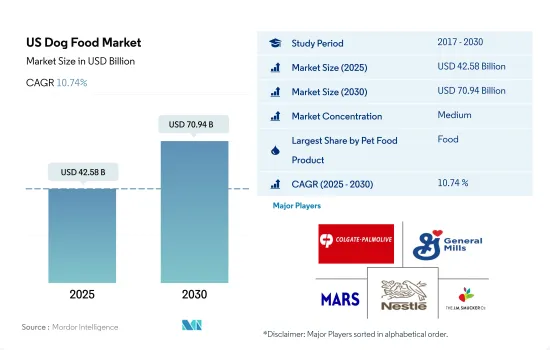

米国のドッグフード市場規模は2025年に425億8,000万米ドルと推定され、2030年には709億4,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.74%で成長する見込みです。

予防医療の動向の高まりが、国内で最も速い速度で動物用飼料セグメントを牽引しています。

- 米国では、ドッグフード市場は2022年に総額314億米ドルに達し、世界最大のドッグフード市場としての地位を確立しました。この成長は、多様な流通チャネルを通じてさまざまな形態のペットフードが入手しやすくなったこと、複数のメリットを提供するペットフードへの需要が高まっていること、消費者が幅広い選択肢を選べるようになったことなど、さまざまな要因によるものです。

- 米国内では、ドッグフード産業は主にペットフードで構成されており、2022年の市場規模は215億米ドルでした。ドライ・ドッグフードがドッグフード市場全体の71.6%を占め、ウェット・ドッグフードが2022年の残りの28.4%を占めます。ドライドッグフードの人気は、ペットにとって多くの利点があること、主流ブランドからニッチブランドまで幅広い選択肢があることに起因しています。

- ドッグフード市場で2番目に大きいセグメントは犬用スナックで、2022年の市場規模は46億米ドルでした。スナックは、しつけ、デンタルケア、ご褒美など、さまざまな目的で犬に好まれています。このセグメントの成長を牽引しているのは、多様な原料の使用と、犬用スナックにビタミン、ミネラル、その他のサプリメントを添加することです。推定・予測期間中のCAGRは11.2%です。

- 動物用飼料市場は、ドッグフード市場の中で最も急成長しているセグメントです。ペットの健康のための予防措置として動物用飼料の利用が増加していることから、予測期間中のCAGRは12.8%と予測され、急速に市場を牽引すると予想されます。

- ペット数の増加と市販ペット用品の採用増加が、予測期間中に市場を牽引すると予測される要因です。

米国のドッグフード市場動向

ペットのエコシステムの進化と、犬を飼うためのさまざまなチャネルの利用可能性の上昇が、同国の市場を牽引しています。

- 米国では2022年にペットとしての犬のシェアが38.6%と高くなったが、これは、人々が犬により安心感を覚え、犬が本来持っている飼い主の日課に適応する能力により、コンパニオンシップの需要が高いためです。そのため、犬をペットとして飼う家庭が増え、犬の飼育数が増加しました。2022年には約6,510万世帯が犬を飼っており、ペットを飼っている世帯の74.9%を占めています。2021年には、犬の飼い主の85%が犬を家族の一員と考えています。米国の農村部ではペットの飼い主が多く、2017年には都市部より19%多くなりました。ワイオミング州、ウェストバージニア州、インディアナ州は犬の飼育数が最も多いです。

- 動物保護施設は犬の養子縁組の重要なチャネルの一つであり、所得水準の上昇と大きなアパートでのコンパニオンとしての犬の需要の高さから、予測期間中にペットショップからの犬の購入の増加が予想されます。2020年には、犬を飼う親の38%が動物保護施設から犬を迎え入れ、42%がペットショップから犬を購入しています。

- ペットグルーミング、ペットボーディング、ドッグウォーキングといったサービスの需要も高いです。例えば、米国のPet Backerは、ペットの親が留守の間、ペットの世話をし、グルーミングサービスも提供しています。

- ペットの人間化傾向の高まりとペット・エコシステムの進化は、同国におけるペット数の増加に貢献すると予想され、その結果、予測期間中にペットフードの需要が増加すると予想されます。

プレミアム化の動向と、愛犬にエコフレンドリーペットケア製品を与えたいという意欲の高まりが、国内の支出率を押し上げています。

- 米国では、ペットオーナーの犬に対する支出は着実に増加し、2019~2022年の間に約24.0%上昇しました。この支出の増加は、愛犬を飼う人の増加、さまざまな種類のドッグフードの幅広い入手可能性、プレミアム化の動向など、複合的な要因によるものです。2022年の犬の飼育世帯数は6,510万世帯で、国内のペット飼育世帯の約74.9%を占めます。

- その他のペット動物と比較すると、ペットオーナーは犬にかける費用が多く、犬1頭あたりの年間平均支出額は猫1頭あたりの年間平均支出額より12.2%高いです。これは、犬の方が猫よりも餌の消費量が多いため、犬の食費に占める割合が大きくなっているためです。さらに、米国では犬の飼育数が猫の飼育数を上回っています。2022年現在、犬のペット数は9,240万匹、猫のペット数は6,470万匹で、犬に比べ猫の飼育数は42.8%少ないです。

- ドッグフードとスナックは、ペット犬の支出全体の40.9%を占めています。過去5年間で、最小限の加工を施したドッグフードの購入が147%増加しており、自然なドッグフード製品への嗜好が高まっていることを示しています。ペットの飼い主は通常、スーパーマーケットやペットショップ、オンライン小売店でペットフードを購入します。最近では、オンラインチャネルを通じたペットフードの販売が大幅に増加しています。パンデミックはオンラインチャネルへのシフトを加速させ、2022年にはペットフードのオンライン販売はペットフード販売全体の23.9%を占めるようになります。この動向は、高品質のペットフードの利点に対する意識の高まりと、ペットフードのプレミアム化が進んでいることに起因しており、今後も同国のペット支出を牽引していくと予想されます。

米国ドッグフード産業概要

米国のドッグフード市場は適度に統合されており、上位5社で58.04%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、The J. M. Smucker Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The US Dog Food Market size is estimated at 42.58 billion USD in 2025, and is expected to reach 70.94 billion USD by 2030, growing at a CAGR of 10.74% during the forecast period (2025-2030).

The growing trend of preventative care is driving the veterinary diets segment at the fastest rate in the country

- In the United States, the dog food market reached a total value of USD 31.4 billion in 2022, establishing itself as the largest dog food market globally. This growth can be attributed to various factors, including the greater availability of pet food in different forms through diverse distribution channels, the growing demand for pet food offering multiple benefits, and the wide range of choices available to consumers.

- Within the United States, the dog food industry is predominantly comprised of pet food, accounting for a market value of USD 21.5 billion in 2022. Dry dog food held the majority share, representing 71.6% of the overall dog food market value, while wet dog food made up the remaining 28.4% in 2022. The popularity of dry dog food can be attributed to its numerous benefits for pets and the wide range of options available in mainstream and niche brands.

- The second-largest segment within the dog food market is dog treats, which had a market value of USD 4.6 billion in 2022. Treats are favored by dogs for various purposes, including training, dental care, and rewards. The growth of this segment is driven by the use of diverse ingredients and the inclusion of added vitamins, minerals, and other supplements in dog treats. It is estimated to register a CAGR of 11.2% during the forecast period.

- The veterinary diets market is the fastest-growing segment within the dog food market. The increasing utilization of veterinary diets as a preventive measure for pet health is anticipated to drive the market at a rapid rate, with a projected CAGR of 12.8% during the forecast period.

- The rising pet population and the increased adoption of commercial pet products are factors anticipated to drive the market during the forecast period.

US Dog Food Market Trends

Evolving pet ecosystem and rising availability of different channels for dog adoption driving the market in the country.

- Dogs as pets had a higher share in the United States in 2022, i.e., 38.6%, due to the high demand for companionship, as people feel more secure with dogs and dogs' inherent ability to adapt to their owner's routines. Thus, more households had dogs as pets, increasing their population. In 2022, around 65.1 million households owned a dog, which accounted for 74.9% of the households owning a pet. In 2021, 85% of dog owners consider dogs as their family members. There were more pet owners in the rural areas of the United States, with 19% more than in urban areas in 2017. The states of Wyoming, West Virginia, and Indiana have the highest population of dogs.

- The animal shelter is one of the key channels for dog adoption, and a rise in the purchase of dogs from pet stores is expected during the forecast period due to a rise in income levels and the high demand for dogs as companions in big apartments. In 2020, 38% of dog parents adopted a dog from an animal shelter, while 42% purchased them from a pet store.

- The demand for services such as pet grooming, pet boarding, and dog walking is high, as pet parents are treating their pets as family members. For instance, Pet Backer in the United States helps pet parents care for their pets when they are away and also provides grooming services.

- The growing trend of pet humanization and the evolving pet ecosystem are anticipated to help increase the pet population in the country, which, in turn, is expected to increase the demand for pet food during the forecast period.

The growing trend of premiumization and willingness to provide their dogs with eco-friendly pet care products driving the expenditure rate in the country

- The expenditure of pet owners on dogs steadily increased in the United States, with a rise of around 24.0% between 2019 and 2022. This increase in spending was due to a combination of factors, including the growing number of people who own pet dogs, the wider availability of different types of dog food, and the trend toward premiumization. In 2022, the number of households with dogs was 65.1 million, representing about 74.9% of households that own pets in the country.

- In comparison to other pet animals, pet owners spend more on their dogs, with the average yearly expenditure per dog being 12.2% higher than the average yearly expenditure per cat. This is because dogs consume more food than cats, leading to a greater share of spending on food for dogs. Additionally, the population of dogs is higher than that of cats in the United States. As of 2022, there were 92.4 million pet dogs and 64.7 million pet cats, representing a 42.8% lower population of cats compared to dogs.

- Pet dog food and treats account for 40.9% of overall pet dog expenditure. Over the last five years, there has been a 147% rise in the purchase of minimally processed dog food, indicating a growing preference for natural dog food products. Pet owners typically buy pet food from supermarkets, pet stores, and online retailers. In recent times, there has been a significant rise in pet food sales through online channels. The pandemic has accelerated the shift toward online channels, with online pet food sales accounting for 23.9% of total pet food sales in 2022. This trend is driven by the growing awareness of the benefits of high-quality pet food and the increasing premiumization of pet food, which is expected to continue driving pet expenditure in the country.

US Dog Food Industry Overview

The US Dog Food Market is moderately consolidated, with the top five companies occupying 58.04%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms