南米のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 283 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693989

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

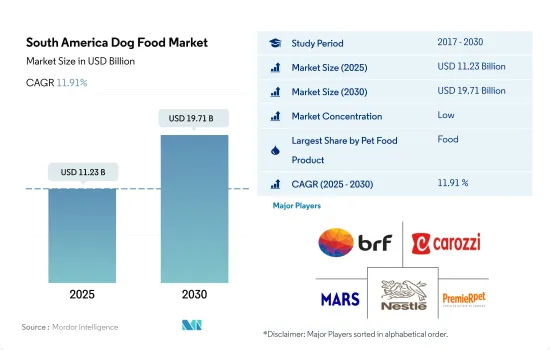

南米のドッグフード市場規模は2025年に112億3,000万米のドルと推定され、2030年には197億1,000万米のドルに達すると予測され、予測期間(2025~2030年)のCAGRは11.91%で成長する見込みです。

腎臓、尿路、糖尿病などの疾病の増加により、動物用飼料が最も急成長しています。

- 南米では、一人当たりの消費量が多く人口が多いため、犬がペットフード市場全体を支配する主要なペットです。したがって、2022年には、犬がこの地域のペットフード市場の68.8%を占め、同期間に犬の飼育数が12.7%増加したため、2017~2022年の間に83.9%増加しました。

- 2022年には、ペットフード部門が地域のドッグフード市場で最大の部門となり、市場規模は60億3,830万米のドルとなりました。これは、犬にとって主食となるペットフードを定期的に与えることで、日々の栄養要求を満たすためです。さらに、ドライペットフードがウェットペットフードよりも優勢であり、給餌の利便性、費用対効果、高い保存期間、栄養バランスにより、2022年には75.3%のシェアを占めました。

- 2022年の市場規模は、スナック部門が10億4,180万米のドルで第2位、次いで動物用飼料(7億150万米のドル)、栄養補助食品/サプリメント(1億9,920万米のドル)でした。スナックセグメントは、訓練セッション中の積極的強化、精神的刺激と娯楽の源、特別な楽しみの提供、ペットと親の絆の強化などの利点により、2017~2022年の間に79.2%成長しました。

- しかし、動物用飼料市場は予測期間中に15.6%という最も速いCAGRで推移すると予測されています。これは、犬の予防医療への積極的なアプローチとして動物用食餌の採用が増加していること、腎臓、尿路、糖尿病などの疾病の発生率が増加していることによる。

- 人口の増加、予防的アプローチに対する意識の高まり、ペットの人間化の進展、製品タイプの優位性などが、予測期間中にCAGR 12.3%で市場を牽引すると予想される要因です。

ブラジルは高度に確立された流通網を通じて南米のドッグフード市場を独占

- 2022年、南米は世界のドッグフード市場において最大市場のひとつに浮上し、市場規模は約79億7,000万米のドルに達しました。南米ではペットの飼育率が高いため、ブラジルとアルゼンチンがドッグフード市場に大きく貢献しています。南米のドッグフード市場は、2017~2022年にかけて84.9%成長したが、これはペットの飼育率の増加、犬の健康とウェルネスに対する意識の高まり、ペットの人間化傾向の高まりが背景にあります。

- ブラジルが南米のドッグフード市場を独占し、2022年の市場規模は55億3,000万米のドルでした。これは主に、同年590万人に達した同国のペット犬の飼育数の多さによるものです。可処分所得の増加、人口動態の変化、消費者の嗜好の進化も、世界市場におけるブラジルの存在感を高めています。

- アルゼンチンは、南米最大のペット愛好国のひとつです。ペットの主要選択肢は犬で、2022年には同国のペット数の36.4%を占めます。この犬の飼育数の多さが同国のドッグフード市場の成長に寄与しており、同年の市場規模は8億80万米のドルに達しました。

- その他の南米セグメントには、チリ、パラグアイ、ベネズエラなどの国が含まれます。これらの国では、ペットとして犬を飼う人が増えているため、ドッグフード製品に対する需要が高まっています。その他の南米のドッグフード市場は2022年に16億4,000万米のドルと評価されました。この市場を牽引しているのは、ペットの人間化の進展、可処分所得の増加、市販ペットフードへの顧客嗜好の変化です。

- 南米における犬の飼育数の増加、可処分所得の増加、ペットの飼育が、予測期間中の市場成長を促進すると予想されます。

南米のドッグフード市場動向

犬は南米で最も人気があり、重宝されているペットであり、ペット総飼育数の29.8%を占める

- 南米では、2022年にペットの犬の飼育数がペット総飼育数の約29.8%を占めました。南米の多くの国々で犬の飼育が増加しています。欧州諸国とは異なり、南米では猫よりも犬が好まれ、この地域の多くの文化で高く評価されており、多くの家庭が犬を家族の一員と考えています。その結果、愛犬の飼育数は年々着実に増加しています。

- 2019~2022年の間に、南米の犬の飼育数は約6.0%増加します。これはCOVID-19パンデミックの影響によるものと考えられます。ロックダウン規制により人々が家で過ごす時間が長くなったため、この地域全体でペット犬の所有が急増しました。

- 2022年現在、南米におけるペット犬のシェアはブラジルが過半数を占め、総飼育数の約60.4%を占めています。ブラジルの愛犬の飼育数は約5,970万頭で、米国に次いで世界第2位です。また、ブラジルの小型犬の数は世界一で、体重20ポンド(約1.5kg)以下の犬が全体の55.0%を占めています。

- 多くの南米諸国では、フード、玩具、グルーミング用品など、飼い主のニーズに応える身近な店があります。ペットショップや動物病院も普及し、飼い主が愛犬に適切なケアを提供しやすくなっています。この地域では、犬のヒューマニゼーション(人間化)の動きが活発化しています。Carnaval do Cao」(犬のカーニバル)のように、コンテストや音楽パフォーマンス、さまざまなコスチュームのドッグショーなど、多くのイベントが開催されています。こうした動向により、予測期間中、同地域での犬の飼育率は全体的に高まると予想されます。

高所得者とプレミアム化により、この地域で最もペットへの支出が多いのはブラジル

- 南米におけるペット犬への支出は着実に増加しており、2019~2022年にかけて約21.0%増加しました。この増加は主に、同地域全体でのペット飼育数の増加によるものです。例えば、ブラジルでペット犬を所有する世帯数は約6.5%増加し、アルゼンチンでは2016~2020年の間に約6.9%増加しました。さらに、同地域のペットオーナーはペットの人間化にますます重点を置くようになっており、高所得のペットオーナーは天然成分の使用や製品のプレミアム化を通じて売上成長を促進しています。例えば、ブラジルのプレミアムドライ・ドッグフードの小売販売額は、2016年の3億3,570万米のドルから2022年には7億4,810万米のドルに増加し、CAGRは14.7%となりました。

- しかし、この地域全体が不況に見舞われているため、価格に対する感度がドッグフードブランドを選択する際の重要な要素となっています。例えばアルゼンチンでは、ペットの飼い主は出費を管理するために、頻繁にブランドを変更したり、最も手頃な価格の選択肢を選んだりしています。2020年の売上高で最も多かったのは「エコノミー」フードブランドで、ドライドッグフードの総売上高の49.9%を占めました。この動向は、費用対効果の高いドッグフードを好む傾向が強いことを示しています。

- ペットショップ、動物病院、スーパーマーケットなどのオフラインの小売チャネルは、この地域でペットフード製品を購入するための好ましい流通チャネルです。しかし、COVID-19の大流行中、ペットフードの流通におけるeコマースのシェアは、2022年時点で13.2%に達しました。プレミアムペットフードの消費量の増加と、健康的で栄養価の高いペットフードの利点に関する意識の高まりが、この地域におけるペット支出の増加に貢献しました。

南米のドッグフード産業概要

南米のドッグフード市場はセグメント化されており、上位5社で26.56%を占めています。この市場の主要企業は、BRF Global、Empresas Carozzi SA、Mars Incorporated、Nestle(Purina)、PremieRpetです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- BRF Global

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Empresas Carozzi SA

- FARMINA PET FOODS

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PremieRpet

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001471

The South America Dog Food Market size is estimated at 11.23 billion USD in 2025, and is expected to reach 19.71 billion USD by 2030, growing at a CAGR of 11.91% during the forecast period (2025-2030).

Veterinary diets are the fastest-growing segment, driven by increasing incidence of diseases such as renal, urinary tract, and diabetes

- In South America, dogs are the major pets dominating the overall pet food market due to the higher per capita consumption and high population. Therefore, in 2022, dogs held 68.8% of the region's pet food market, which increased by 83.9% between 2017 and 2022 due to an increase in the dog population by 12.7% during the same period.

- In 2022, the pet food segment was the largest segment of the regional dog food market, with a market value of USD 6,038.3 million. It is due to the regular feeding of pet food to meet their daily nutritional requirements, which act as a staple food for dogs. Moreover, dry pet food dominated over wet pet food as it accounted for a 75.3% share in 2022 due to its convenience to feed, cost-effectiveness, high shelf life, and nutritional balance.

- The treats segment was the second-largest segment, with a market value of USD 1,041.8 million in 2022, followed by veterinary diets (USD 701.5 million) and nutraceuticals/supplements (USD 199.2 million). The treats segment grew by 79.2% between 2017 and 2022 due to their advantages, such as positive reinforcement during training sessions, source of mental stimulation and entertainment, providing special indulgence, and strengthening the bond between the pet and its parent.

- However, the veterinary diets market is projected to register the fastest CAGR of 15.6% during the forecast period. It is due to the growing adoption of veterinary diets as a proactive approach to preventive care for dogs and the increasing incidence of diseases such as renal, urinary tract, and diabetes.

- The increase in population, increased awareness of preventive approaches, rise in pet humanization, and advantages of product types are the factors expected to drive the market with a CAGR of 12.3% during the forecast period.

Brazil dominated the South American dog food market through a highly established distribution network

- In 2022, South America emerged as one of the largest markets in the global dog food market, with a market value of around USD 7.97 billion. Brazil and Argentina are the major contributors to the dog food market in South America due to the high pet ownership rates in these countries. The South American dog food market grew by 84.9% from 2017 to 2022, driven by the increasing adoption of pets, the growing awareness of dog health and wellness, and the rising trend of pet humanization.

- Brazil dominated the South American dog food market, with a market value of USD 5.53 billion in 2022. This was mainly due to the country's significant pet dog population, which reached 5.9 million in the same year. Growing disposable incomes, changing demographic patterns, and evolving consumer preferences have also contributed to Brazil's strong presence in the global market.

- Argentina is one of the biggest pet-loving countries in South America. Dogs are the primary choice of pets, accounting for 36.4% of the pet population of the country in 2022. This significant dog population has contributed to the growth of the dog food market in the country, which reached a market value of USD 800.8 million in the same year.

- The Rest of South America segment includes countries like Chile, Paraguay, and Venezuela. There is a rising demand for dog food products in these countries as more people adopt dogs as pets. The dog food market in the Rest of South America was valued at USD 1.64 billion in 2022. It is driven by the increased humanization of pets, higher disposable incomes, and a shift in customer preferences toward commercial pet food.

- The growing dog population, increased disposable income, and pet adoption in South America are expected to fuel the growth of the market during the forecast period.

South America Dog Food Market Trends

Dogs are the most popular and valued pets in South America, accounting for 29.8% of the total pet population

- In South America, the pet dog population accounted for about 29.8% of the total pet population in 2022. Dog ownership has been increasing across many South American countries. Unlike European countries, South Americans prefer dogs to cats and are highly valued in many cultures across the region, with many families considering them as part of their family. As a result, the pet dog population has been steadily increasing over the years.

- Between 2019 and 2022, the dog population in South America increased by about 6.0%. This could be attributed to the impact of the COVID-19 pandemic. With people spending more time at home due to lockdown restrictions, there was a surge in the ownership of pet dogs throughout the region.

- As of 2022, Brazil held the majority share of pet dogs in South America, accounting for about 60.4% of the total population. Brazil ranked second in the world in terms of the pet dog population, with around 59.7 million pet dogs, only behind the United States. In addition, Brazil has the largest number of small dogs worldwide, accounting for 55.0% of all pet dogs weighing less than 20 lbs.

- In many South American countries, there are accessible stores that cater to the needs of pet owners, including food, toys, and grooming products. Pet stores and veterinary clinics are also becoming more widespread, making it easier for pet owners to provide proper care for their dogs. There is an increasing trend of dog humanization in the region. There are many events, like "Carnaval do Cao" or "Carnival of Dogs," that feature plenty of contests, musical performances, and dog shows with a variety of costumes. These trends are anticipated to increase overall dog ownership in the region during the forecast period.

Brazil stands out with the highest pet expenditure in the region due to higher-income individuals and premiumization

- The expenditure on pet dogs in South America has been on a steady increase, which increased by about 21.0% between 2019 and 2022. This increase is mainly due to the increase in pet ownership across the region. For instance, the number of households owning a pet dog in Brazil increased by about 6.5%, while in Argentina, it increased by about 6.9% between 2016 and 2020. Additionally, pet owners in the region are increasingly focused on pet humanization, and higher-income pet owners are driving sales growth through the use of natural ingredients and product premiumization. For instance, the retail sales value of premium dry dog food in Brazil saw a rise from USD 335.7 million in 2016 to USD 748.1 million in 2022, with a CAGR of 14.7%, reflecting the escalating demand for premium dog products.

- However, with an economic downturn prevailing across the region, price sensitivity has become a crucial factor in choosing dog food brands. In Argentina, for instance, pet owners frequently switch brands or opt for the most affordable options to manage their expenses. The largest portion of sales in 2020 belonged to 'Economy' food brands, which accounted for 49.9% of the total dry dog food sales value. This trend indicates the leading preference for cost-effective dog food options.

- Offline retail channels such as pet shops, vet clinics, and supermarkets are the preferred distribution channels for purchasing pet food products in the region. However, during the COVID-19 pandemic, e-commerce's share in the distribution of pet food reached 13.2% as of 2022. The higher consumption of premium pet food and growing awareness about the benefits of healthy, nutritious pet food helped in increasing pet expenditure in the region.

South America Dog Food Industry Overview

The South America Dog Food Market is fragmented, with the top five companies occupying 26.56%. The major players in this market are BRF Global, Empresas Carozzi SA, Mars Incorporated, Nestle (Purina) and PremieRpet (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 BRF Global

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 Empresas Carozzi SA

- 6.4.6 FARMINA PET FOODS

- 6.4.7 General Mills Inc.

- 6.4.8 Mars Incorporated

- 6.4.9 Nestle (Purina)

- 6.4.10 PremieRpet

- 6.4.11 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 283 Pages

- 納期

- 2~3営業日