|

市場調査レポート

商品コード

1693980

北米のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)North America Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 303 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

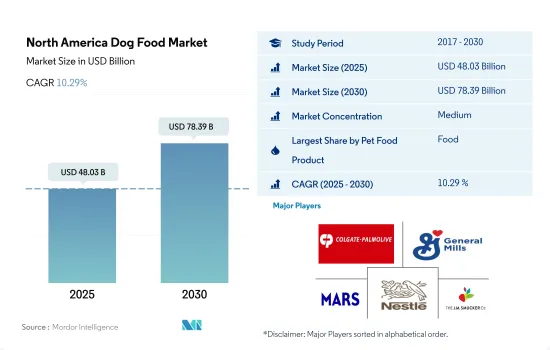

北米のドッグフード市場規模は2025年に480億3,000万米のドルと推定・予測され、2030年には783億9,000万米のドルに達し、予測期間(2025~2030年)のCAGRは10.29%で成長すると予測されます。

動物用飼料が最も急成長しているセグメントであり、予防医療の動向の高まりがその原動力となっています。

- ペットフードが市場を独占し、2022年の市場総額の約68.0%を占めました。これは、ペットフードが、ペットの品種や年齢に関係なく、この地域のほとんどの飼い主の主食となっているためです。ペット数の増加傾向に伴い、同地域のペットフード市場は予測期間中に10.1%のCAGRで推移すると予測されています。

- ペット用スナックは、2022年の総市場額の約15.6%を占めています。一般的に、スナックは他のペット動物に比べて犬に好まれることが多いです。ペットにスナックを与える主要目的は、しつけ、歯の健康維持、ご褒美です。スナック市場は予測期間中にCAGR 10.6%で増加すると予測されています。

- ペット用動物飼料市場は、2022年に市場全体の約13.0%を占めました。これらの食事は、尿路疾患、腎不全、消化過敏症など、ペットの特定の健康状態に対処するために特別に配合されます。また、特定の健康問題の開発を避けるための予防措置としてペットに与えられることもあります。予測期間中、ペットの動物用食事療法のCAGRは12.3%と最も高くなると予想され、こうした特殊な製品に対する需要が高まっていることを示しています。

- ペット用栄養補助食品またはサプリメントは、2022年の市場金額の3.5%を占めています。これらのペット用サプリメントは、全体的な健康と幸福をサポートするためにペットに与えられることが多いです。栄養不足に対処し、関節、皮膚、被毛の健康などの健康上の利点をサポートすることができます。ペット用サプリメントの市場は、予測期間中にCAGR 6.1%で増加すると予測されています。

- ペット数の動向の増加と市販のペットフードが提供する特定の利点が、予測期間中の市場を牽引すると予想されます。

グレインフリー、オーガニック、単一肉源のドッグフード製品に対する需要の高まりが北米市場を牽引している

- 北米のドッグフード市場は、同地域最大のペットフード市場であり、シェア49.5%を占め、2022年には2017年比81.8%増の360億米のドルに達しました。市場金額の増加は、2017~2022年の間に北米諸国全体で犬の飼育数が17.6%増加したことに関連しています。

- 北米では、ペットの飼い主からの高品質なペットフード製品に対する需要の増加と、市販のドッグフード製品の使用率の上昇により、米国がドッグフード市場において最大の国となっています。また、米国は北米のドッグフード市場において最も急成長している国であり、予測期間中のCAGRは10.9%と予想され、次いでメキシコが7.2%で、同地域では自家製フードの使用量が減少し、ペットフード製品のプレミアム化が進んでいます。

- その結果、ペットの親たちの間でプレミアム化が進むにつれて、グレインフリーまたは単一穀物製品、単一肉源製品、持続可能性と気候の回復力に沿った有機と自然食品、植物性タンパク質などの代替タンパク質源を使用したドッグフード製品は、この地域のプレミアムとスーパープレミアムセグメントでより高い需要を持っています。しかし、ペットの健康に対する関心の高まりと動物用飼料を使用することの利点が、動物用飼料セグメントの成長を加速させ、予測期間中のCAGRは12.4%と推定・予測されています。

- 市販のペットフード製品の使用の増加、ペットのプレミアム化の増加、ペットの飼い主の可処分所得の増加に伴う人間化は、北米のドッグフード市場を牽引し、同地域の予測期間中のCAGRは10.4%を記録すると予測されます。

北米のドッグフード市場の動向

動物保護施設からの犬の引き取りの増加と進化するペット生態系が市場の成長を後押ししている

- 北米では犬の飼育が増加傾向にあります。北米では、交友関係の需要が高く、犬が本来持っている飼い主の日課に適応する能力により、犬は他の動物よりも高いシェアを占めています。米国やカナダなどの先進諸国では、ペットとして犬を飼う世帯が増加しているため、この地域ではペットとしての犬の数が増加しています。例えば、2022年には犬を飼う世帯数は6,510万世帯、猫を飼う世帯数は4,650万世帯でした。米国の農村部では、2017年に都市部よりも19%多くペットを飼っていました。

- 小型犬と中型犬の需要が高いです。米国では狭いアパートに住む人々が体重1kgから40kgの犬を飼ったり購入したりしています。2021年には、体重11kg以下の犬が47%を占め、11kgから18kgの犬が31%を占めます。小型犬は大型犬に比べてスペースを必要としないためです。2021年には、犬を家族の一員と考えるペットの親が犬の飼い主の85%を占めます。これは将来的にペットとしての犬の飼育数の増加に役立つと予想されます。

- 動物保護施設は、犬を飼うための主要な獲得チャネルのひとつです。例えば、2020年には、犬の親の38%が動物保護施設から犬を採用したのに対し、42%がペットショップから購入しました。これは、所得水準の上昇と、パンデミックによるロックダウン中の大きなアパートでのコンパニオンとしての犬の需要の高さによる。

- ペットの人間化と進化するペット生態系は、予測期間中にこの地域のペット数増加に役立つと予想される要因です。

プレミアム化の動向と、エコフレンドリーペットケア製品をペットに与えたいという意欲の高まりが、支出率を押し上げています。

- 北米では、ペット支出増加の動向が見られます。ペットへの支出が増加しているのは、米国とカナダでさまざまな種類のペットフードが入手可能になり、プレミアム化が進んでいるためです。北米では、犬の飼い主は愛犬に高級ペットフードを与えることを好み、エコフレンドリーペットケア製品を積極的に採用しています。例えば、2022年には、ペットの親の50%以上が、プレミアム価格を支払うことによって、犬を含むペットにエコフレンドリーペットケア製品を提供することになっており、犬の飼い主の42%がプレミアムペットフードを犬に与えています。

- ペットの親たちの最も高い出費はペットフードとスナックで、これは予測期間中に増加すると予想されます。例えば、ペットフードとスナックは、2022年に犬にかかった費用の25.8%(2,908米のドル)を占めています。これらは最も高いシェアを占めており、ペットの親がペットを家族の一員として扱い、専用のペットフードに対する意識を高めていることから、今後も増加すると予測されています。犬はグルーミング、獣医療的ケア、他の犬との社会化のためのペット・トレーニングなどのサービスを必要とするため、ペットの親は犬を飼い始めた当初により多くの出費を強いられます。例えば、2022年にはグルーミングに70~80米のドルが費やされます。

- カナダでは、ペットの親がペットにギフトやペットグルーミング、ペットボーディング、ドッグウォーカーなどのサービスを提供するケースが増えています。ペットの親がこれらのサービスにかける年間支出は、2018年の2,075米のドルから2021年には2,430米のドルに増加しました。プレミアム化と高品質フードの利点に関する意識の高まりは、この地域におけるペット支出の増加に役立っていると予測される要因です。

北米のドッグフード産業概要

北米のドッグフード市場は適度に統合されており、上位5社で59.04%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、The J. M. Smucker Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The North America Dog Food Market size is estimated at 48.03 billion USD in 2025, and is expected to reach 78.39 billion USD by 2030, growing at a CAGR of 10.29% during the forecast period (2025-2030).

Veterinary diets comprise the fastest-growing segment, driven by the growing trend of preventative care

- Pet food dominated the market and accounted for about 68.0% of the total market value in 2022. This is because pet food is a staple purchase for most pet owners in the region, regardless of their pet breed size or age. With the increasing trend in the pet population, the pet food market in the region is anticipated to register a CAGR of 10.1% during the forecast period.

- Pet treats accounted for about 15.6% of the total market value in 2022. Generally, treats are mostly preferred by dogs compared to other pet animals. The main purpose of feeding the pets with treats is to train them, maintain their dental health, and reward them. The treats market is anticipated to increase at a CAGR of 10.6% during the forecast period.

- The pet veterinary diets market accounted for about 13.0% of the total market value in 2022. These diets are specifically formulated to address certain health conditions in pets, such as urinary tract diseases, renal failure, and digestive sensitivity. They may also be given to pets as a preventative measure to avoid developing certain health issues. During the forecast period, pet veterinary diets are expected to experience the highest CAGR of 12.3%, indicating a growing demand for these specialized products.

- Pet nutraceuticals or supplements accounted for 3.5% of the market value in 2022. These pet supplements are often given to pets to support overall health and well-being. They can address nutritional deficiencies and support health benefits such as joint, skin, and coat health. The market for pet supplements is anticipated to increase at a CAGR of 6.1% during the forecast period.

- The increasing trend in the pet population and the specific benefits offered by commercial pet foods are anticipated to drive the market during the forecast period.

The growing demand for grain-free, organic, and single meat source dog food products is driving the North American market

- The dog food market in North America was the largest pet food market in the region, accounting for a 49.5% share and reaching USD 36 billion in 2022, an increase of 81.8% from 2017. The increase in the market value was associated with the increase in the adoption of dogs across North American countries by 17.6% between 2017 and 2022.

- In North America, the United States was the largest country in terms of the dog food market due to the increase in demand for high-quality pet food products from pet owners and the rising usage of commercial dog food products. The United States is also the fastest-growing country in the North American dog food market, with an anticipated CAGR of 10.9% during the forecast period, followed by Mexico with 7.2%, with a decrease in usage of homemade food and rising premiumization of pet food products in the region.

- Consequently, with the increasing premiumization among pet parents, dog food products with grain-free or single grain products, single meat source products, organic and natural foods in line with sustainability and climate resilience, along with alternate protein sources such as plant-based protein have higher demand in the premium and super-premium segments in the region. However, the rising concerns about pet health and the benefits of using veterinary diets are estimated to boost the veterinary diets segment to grow faster, with a CAGR of 12.4% during the forecast period.

- The increase in the usage of commercial pet food products, increase in pet premiumization, and humanization with higher disposable income of pet owners are expected to drive the North American dog food market to record a CAGR of 10.4% during the forecast period in the region.

North America Dog Food Market Trends

Growing acquisition of dogs from animal shelters and the evolving pet ecosystem are boosting the market's growth

- Dog adoption is on the rise in North America. Dogs have a higher share than other animals in North America due to the high demand for companionship and dogs' inherent ability to adapt to their owner's routines. This has resulted in an increase in the number of dogs as pets in the region, as developed countries, such as the United States and Canada, witnessed increasing households with dogs as pets. For instance, in 2022, the number of households owning a dog was 65.1 million, and number of households owning a cat was 46.5 million. There were 19% more pet owners in the rural areas of the United States than in urban areas in 2017.

- Small dogs and medium-sized dogs are in high demand. People in the United States living in small apartments are adopting and purchasing dogs weighing between 1 kg and 40 kg. In 2021, dogs with a body weight of less than 11 kg accounted for 47%, and dogs weighing between 11 kg and 18 kg accounted for 31% of the dog population, as smaller dogs require less space compared to large dogs. In 2021, pet parents who considered dogs as family members accounted for 85% of dog owners. This is expected to help in the growth of the dog population as pets in the future.

- Animal shelters are among the key acquisition channels for dog adoption. For instance, in 2020, 38% of dog parents adopted a dog from an animal shelter, whereas 42% purchased from a pet store due to a rise in income levels and the high demand for dogs as companions in big apartments during the pandemic lockdowns.

- Pet humanization and the evolving pet ecosystem are the factors anticipated to help in the growth of the pet population in the region during the forecast period.

The growing trend of premiumization and willingness to provide their pets with eco-friendly pet care products driving the expenditure rate

- A trend of increase in pet expenditure is witnessed in North America. The rise in pet expenditure is due to the availability of different types of pet food and growing premiumization in the United States and Canada. In North America, dog owners prefer to provide their dogs with premium pet food and are willing to adopt eco-friendly pet care products. For instance, in 2022, more than 50% of pet parents were to provide their pets, including dogs, with eco-friendly pet care products by paying a premium price, and 42% of dog owners are providing dogs with premium pet food.

- Pet parents' highest expenses are on pet food and treats, which are expected to increase during the forecast period. For instance, pet food and snacks accounted for 25.8% of expenses incurred for dogs in the United States (USD 2,908) in 2022. They have the highest share and are projected to increase because pet parents treat their pets as family members and raise awareness about specialized pet food. Pet parents are required to spend more in the initial days of dogs as dogs require services such as pet grooming, veterinary care, and pet training for socialization with other dogs. For instance, pet parents spent USD 70-80 for a grooming session in 2022.

- In Canada, there has been an increase in pet parents providing their pets with gifts and services such as pet grooming, pet boarding, and dog walkers. The pet parents' annual expenditure on these services increased from USD 2,075 in 2018 to USD 2,430 in 2021 because they treat their dogs as companions and family members or children. Premiumization and rising awareness about the benefits of quality food are factors anticipated to have helped in increasing pet expenditure in the region.

North America Dog Food Industry Overview

The North America Dog Food Market is moderately consolidated, with the top five companies occupying 59.04%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms