|

市場調査レポート

商品コード

1693972

アジア太平洋のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)Asia-Pacific Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 331 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

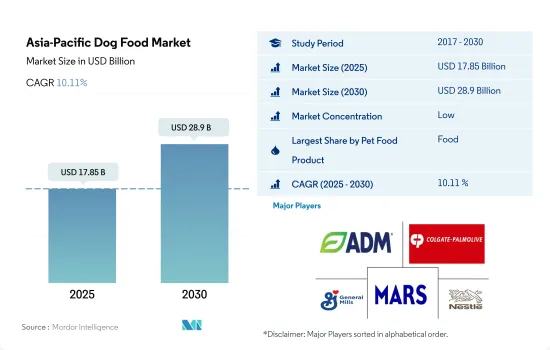

アジア太平洋のドッグフード市場規模は2025年に178億5,000万米ドルと推定され、2030年には289億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.11%で成長すると予測されます。

主食としての一次栄養源であるため、製品タイプではフードセグメントが優位を占める

- アジア太平洋では、市販のペットフードの消費量が多く、人口も多いため、犬がペットフード市場を独占する主要なペットです。2022年には、犬が同地域のペットフード市場の47.7%を占めました。2017~2022年の間に61.9%の大幅な増加があったが、これは犬の飼い主数の増加とこの地域におけるプレミアム製品への需要の増加によるものです。例えば、犬の飼育数は2017年と比較して2022年には16.7%増加しました。中国、日本、オーストラリアはこの地域のペットフード市場の主要国で、2022年には合わせて60%を占めます。

- 2022年の市場規模は92億米ドルで、フードセグメントがドッグフード市場を独占しています。これは、犬種の大小や年齢にかかわらず、同国のほとんどの飼い主にとってフードが主食であるためです。同国のドッグフード市場は、予測期間中にCAGR 9.9%を記録すると予測されています。

- 2022年の市場規模は、スナック部門が270万米ドルで第2位、次いで動物用飼料(14億米ドル)、栄養補助食品/サプリメント(4億9,450万米ドル)です。これは、専用ペットフードがペットの特定の健康状態に対処するのに役立ち、適切な栄養補給を通じて動物の健康をサポートするためです。しかし、スナックは、しつけの際の積極的強化、精神的刺激と娯楽の源、特別な楽しみの提供、親子間の絆の強化などの利点があるため、この地域で最も急成長しているドッグフードセグメントであり、予測期間中、推定・予測CAGRは10.8%です。

- ペット数の増加と幅広い市販ペット用品が提供する様々な利点が、予測期間中の市場を牽引すると予想されます。

中国と日本は、アジア太平洋市場で市販ペットフードの利用増加を記録している主要国です。

- アジア太平洋は世界最大のドッグフード市場の一つであり、ペットの人間化の高まりにより2022年には140億米ドルを占めます。アジア太平洋のドッグフード市場は2017~2022年にかけて61.9%成長したが、これは同地域における業務用ドッグフード製品の利用増加とプレミアム化の進展に沿ったものでした。

- アジア太平洋では、中国が最大のドッグフード市場を占め、2022年には42億米ドルに達しました。同国のシェアが高いのは、犬の飼育数が多く、同年のドッグフードへの支出が多いためです。例えば、同国の犬の飼育数は2022年に地域の犬の飼育数の43.8%を占めました。

- 日本とオーストラリアはアジア太平洋のドッグフード市場の主要国で、2022年の金額ベースでそれぞれ26億米ドルと15億米ドルを占めます。この成長は、プレミアムフードの利用が増加していることと、犬の飼育数が増加していることによる。しかし、フィリピンとインドでは犬の飼育が増加しており、予測期間中にこれらの国々の成長を牽引すると予測され、CAGRはそれぞれ20.9%と17.7%です。

- その他のアジア太平洋の主要ドッグフード市場には、シンガポール、韓国、香港、バングラデシュ、パキスタンが含まれます。その他のアジア太平洋は、2022年にアジア太平洋のドッグフード市場の22.1%を占めました。この地域セグメントは2017~2021年にかけて35.7%成長したが、これは主にペットの人間化の進展と市販ドッグフードの採用増加によるものです。

- したがって、犬の飼育の増加とプレミアム化の高まりがアジア太平洋のドッグフード市場を牽引し、予測期間中にCAGR 9.9%を記録すると予測されます。

アジア太平洋のドッグフード市場の動向

長寿命化とペット生態系の進化が、同地域のペットとしての犬の飼育数の増加に寄与している

- ペット数に占める犬の割合は高く、アジア太平洋のペット数の34.3%を占めます。ペットとして、また同伴者として犬がいる家庭は安心感があるため、犬の飼育数が増加しています。例えば、中国のペットペアレントは、2020年に82.8%を占め、犬を含むペットを家族や幼児として扱っています。また、これらの要因により、2017~2022年の間に、この地域のペットとしての犬の飼育数は16.58%増加しました。犬の採用はパンデミック時に増加したが、犬は寿命が長く、ペットの親との適応能力がもともと高いため、今後も採用が増加すると予想されます。アジア、特に中国で最もよく飼われている犬種は、シベリアンハスキー、チャイニーズフィールドドッグ、プードルです。例えば、2021年、シベリアンハスキーは中国で飼われている犬の16%を占めました。

- 2022年には、中国とインドがアジア太平洋で最も犬の数が多くなりました。これらの国々では、犬の養子率が上昇し、所得水準の上昇と都市化に伴ってペットの人間化が進んだからです。また、ペットフードの入手が容易になり、ペットの飼育が増えたことで、農村部での犬の飼育率にも変化が見られます。さらに、アジア太平洋では、ペットの生態系が進化しているため、犬などのペットを連れて行くことに制限のない場所もあります。例えばインドでは、Head Up For Tailsがペットフードやペットグルーミングなどのサービスを提供するペットショップを展開しています。寿命が延びたことで、ペットの親は犬を家族の一員として扱うようになり、ペット・エコシステムの進化が、この地域におけるペットとしての犬の飼育数の増加に貢献しています。

グレインフリー(穀物不使用)製品や自然派製品など、犬用プレミアム製品への需要の高まりは、ペットへの支出の増加によるものです。

- アジア太平洋では、ペットのヒューマニゼーションが進み、市販のペットフードの需要が増加していること、さまざまな種類のペットフードが入手可能であること、ペットの親がプレミアム価格を支払うことを厭わず、良質なプレミアムペットフードを好むことなどの要因により、ペットへの支出が増加しています。従来から、ペットの犬の数は多く、支出シェアも高く、2022年のペット支出全体の38.1%を占めています。例えば、オーストラリアでは犬が最も人気があり、2022年には約40%の世帯がペットの犬を飼っているため、ドッグフードは同国のペット支出の40%を占めています。

- 中国、インド、オーストラリアなどのアジア諸国では、ペットの親も、ペットのグルーミングや散歩などの付加サービスを提供することで、犬を含むペットの健康に投資しています。さらに、ペット用のスナックや栄養補助食品などの特別な製品を与え、ペットの初期には動物用の良い食事を与えています。例えばインドでは、ペットの親はペディグリーやロイヤルカナンなどのブランドのスナックを犬に与えており、犬の支出(624米ドル)の約65~70%はフードやスナックに、20%はグルーミングやペットのデイケアなどのその他の費用に使われています。

- 市場で入手可能なさまざまな種類のドッグフードに対する意識の高まりは、健康上の懸念、愛犬を家族の一員として扱うこと、プレミアム化の進展といった要因によって、予測期間中に同地域のペット支出を増加させると予想されます。

アジア太平洋のドッグフード産業概要

アジア太平洋のドッグフード市場はセグメント化されており、上位5社で18.10%を占めています。この市場の主要企業は、ADM、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブプロダクト別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブプロダクト別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブプロダクト別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブプロダクト別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Affinity Petcare SA

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- IB Group(Drools Pet Food Pvt. Ltd.)

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Asia-Pacific Dog Food Market size is estimated at 17.85 billion USD in 2025, and is expected to reach 28.9 billion USD by 2030, growing at a CAGR of 10.11% during the forecast period (2025-2030).

The food segment dominated the product types as they are a primary source of nutrition as a staple

- In Asia-Pacific, dogs are the major pets dominating the pet food market due to the higher consumption of commercial pet food and high population. In 2022, dogs held 47.7% of the region's pet food market. There was a significant increase of 61.9% between 2017 and 2022 due to the rising number of dog owners and the increasing demand for premium products in the region. For instance, the dog population grew by 16.7% in 2022 compared to 2017. China, Japan, and Australia are the major countries in the region's pet food market, together accounting for 60% in 2022.

- The food segment dominated the dog food market with a market value of USD 9.2 billion in 2022. This is because food is a staple purchase for most pet owners in the country, regardless of their dog breed size or age. The dog food market in the country is estimated to register a CAGR of 9.9% during the forecast period.

- The treats segment was the second-largest segment, with a market value of USD 2.7 million in 2022, followed by veterinary diets (USD 1.4 billion) and nutraceuticals/supplements (USD 494.5 million). This is because specialized pet foods help address specific health conditions in pets, and they support the well-being of the animals through proper nutrition. However, treats are the fastest-growing dog food segment in the region, with an estimated CAGR of 10.8% during the forecast period due to their advantages, such as positive reinforcement during training sessions, a source of mental stimulation and entertainment, providing special indulgence, and strengthening the bond between the pet and its parent.

- The increasing pet population and the various benefits offered by the wide range of commercial pet products are anticipated to drive the market during the forecast period.

China and Japan are the major countries recording increasing usage of commercial pet foods in the APAC market

- Asia-Pacific is one of the largest dog food markets globally, accounting for USD 14 billion in 2022 due to the rising pet humanization. The Asia-Pacific dog food market grew by 61.9% between 2017 and 2022, which was in line with the increasing usage of commercial dog food products and the growing premiumization in the region.

- In Asia-Pacific, China accounted for the largest dog food market, amounting to USD 4.2 billion in 2022. The higher share of the country was due to its higher dog population and higher expenditure on dog food in the same year. For instance, the country's dog population accounted for 43.8% of the regional dog population in 2022.

- Japan and Australia are the major countries in the Asia-Pacific dog food market, accounting for USD 2.6 billion and USD 1.5 billion, respectively, by value in 2022. This growth can be due to the increasing usage of premium food products and higher dog populations. However, the increasing adoption of dogs in the Philippines and India is estimated to drive the growth of these countries during the forecast period, with CAGRs of 20.9% and 17.7%, respectively.

- The major dog food markets in the Rest of Asia-Pacific include Singapore, South Korea, Hong Kong, Bangladesh, and Pakistan. The Rest of Asia-Pacific accounted for 22.1% of the Asia-Pacific dog food market in 2022. The regional segment grew by 35.7% between 2017 and 2021, mainly due to growing pet humanization and the increasing adoption of commercial dog food.

- Therefore, increasing dog adoption and rising premiumization are projected to drive the Asia-Pacific dog food market to record a CAGR of 9.9% during the forecast period.

Asia-Pacific Dog Food Market Trends

The higher life span and the evolution of the pet ecosystem are helping in the growth of the dog population as pets in the region

- Dogs have a higher share of the pet population, and they account for 34.3% of the pet population in Asia-Pacific. The dog population is higher as people feel more secure in their homes with dogs as pets and companionship. For instance, Pet parents in China treat their pets, including dogs, as their family and child accounted for 82.8% in 2020. These factors also resulted in an increase in the dog population as pets in the region by 16.58% between 2017 and 2022. The adoption of dogs increased during the pandemic, and it is expected that there will be a rise in adoption in the future as dogs have a high life span and an inherent ability to adjust with pet parents. The most common dog breeds adopted in Asia, particularly China, are Siberian Husky, the Chinese field dog, and Poodle. For instance, in 2021, the Siberian Husky accounted for 16% of the dogs adopted in China.

- In 2022, China and India had the highest dog populations in Asia-Pacific as these countries witnessed a rise in the adoption rate of dogs and also a rise in pet humanization with an increase in income levels and urbanization. There is also a shift in the adoption rate of dogs in rural areas with the increased availability of pet food and also increasing adoption of pets. Moreover, there are places in Asia-Pacific without restrictions to take pets, such as dogs, due to the evolving pet ecosystem. For instance, in India, Head Up For Tails has pet stores that offer products and sales of products, such as pet food, pet grooming, and other services. With the higher life span, pet parents treat them as family members, and the evolution of the pet ecosystem is helping to increase the dog population as pets in the region.

Increased demand for premium products for dogs, such as grain-free products and natural products, is due to increasing pet expenditure

- In Asia-Pacific, there has been a rise in pet expenditure because of factors such as an increase in pet humanization, leading to the demand for commercial pet food, availability of different types of pet food, and pet parents' preference for good quality premium pet food as they are willing to pay premium prices. Traditionally, there has been a higher number of pet dogs with a higher expenditure share, accounting for 38.1% of the total pet expenditure in 2022. For instance, in Australia, dog food accounted for 40% of the country's pet expenditure in 2022, as dogs are most popular in Australia, and about 40% of the households had a pet dog in 2022.

- In Asian countries such as China, India, and Australia, pet parents are also investing in the well-being of pets, including dogs, by providing them with additional services such as pet grooming and pet walking. Additionally, they feed their pet dogs with special products such as pet treats and nutraceutical supplements and provide good veterinary diets in their initial days. For instance, in India, pet parents feed their dogs with treats from brands such as Pedigree and Royal Canin, and about 65-70% of the dog expenditure (USD 624) is toward food and treats, whereas 20% is for other expenses such as pet grooming and pet daycare.

- The growing awareness about different types of dog food available in the market for health concerns, treating their dogs as family members, and growing premiumization are the factors expected to help increase pet expenditure in the region during the forecast period.

Asia-Pacific Dog Food Industry Overview

The Asia-Pacific Dog Food Market is fragmented, with the top five companies occupying 18.10%. The major players in this market are ADM, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Philippines

- 5.3.8 Taiwan

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 IB Group (Drools Pet Food Pvt. Ltd.)

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 PLB International

- 6.4.10 Schell & Kampeter Inc. (Diamond Pet Foods)

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms