|

市場調査レポート

商品コード

1693736

米国の飼料用酵素:市場シェア分析、産業動向、成長予測(2025~2030年)United States Feed Enzymes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の飼料用酵素:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 183 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

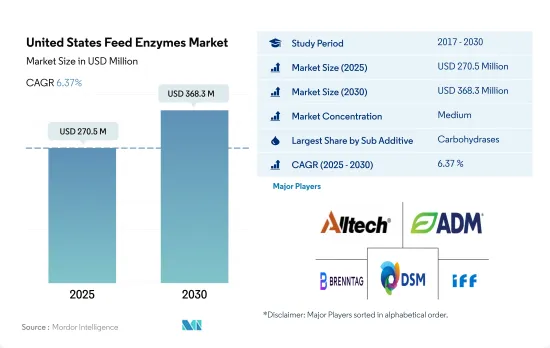

米国の飼料用酵素市場規模は2025年に2億7,050万米ドルと推定され、2030年には3億6,830万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.37%で成長すると予測されます。

- 2022年には、米国が北米の飼料用酵素市場で最大のシェアを占め、市場全体の70%を占めました。米国の飼料酵素市場規模は2億米ドルで、飼料添加物市場全体の3.8%に寄与しています。米国における飼料酵素の市場規模は、反芻動物や家禽鳥類の飼料生産量の増加により、2020年には2019年比で19.7%の大幅な伸びを示しました。

- すべての飼料酵素の中で、米国ではカーボヒドラーゼが47.6%の最大市場シェアを占め、フィターゼとその他の酵素がそれぞれ33%と19.5%のシェアで続きました。動物飼料に炭水化物分解酵素を使用すると、穀物からの栄養素の吸収が向上し、飼料コストの削減につながります。家禽、反芻動物、豚が炭水化物分解酵素セグメントで最大の動物タイプで、それぞれ41%、37%、19%の市場シェアを占めています。

- 飼料用炭水化物分解酵素セグメントは、炭水化物分解酵素を含む動物飼料の割合が高く、炭水化物分解酵素の使用量と需要が多いことから、予測期間中に成長し、CAGR 6.4%を記録すると予想されます。炭水化物分解酵素やフィターゼを含むほとんどの飼料用酵素は自然には合成できないため、すべての動物タイプの飼料を通じて1種類以上の酵素を供給する必要があります。

- 飼料酵素の需要は、動物の全体的な健康状態を改善し、家畜の病気を減らし、動物飼料の安定性と一貫性を高めるのに役立つため、増加しています。したがって、米国の飼料酵素市場は予測期間中に成長し、CAGR 6.3%を記録すると予想されます。

米国の飼料用酵素市場の動向

米国の養鶏産業は最大の商業食品産業の1つであり、肉類と卵の消費の増加が養鶏生産を増加させています。

- 米国の鶏肉産業は、業務用食品産業における鶏卵と鶏肉の需要の増加と輸出の増加により繁栄しています。同国は世界有数の鶏卵生産・輸出国であり、2020年の鶏卵輸出総額は2019年比9.3%増の35億卵、輸出額は2.4%増の1億8,900万米ドルに達します。

- 米国における鶏肉の消費は、良好な価格、高タンパク質食への意識の高まり、鶏肉の需要増加により改善しました。その結果、2022年の家禽の頭数は2021年に比べて1,760万羽増加しました。狭いスペースと異なる環境で鶏を飼育することで、鶏肉生産は牛肉や豚肉よりも実現可能で安価になり、飼育面積が限られた畜産農業従事者が養鶏場に投資するようになりました。

- しかし、米国の輸入シェアは2021年の26%から2031年には24%に減少すると予想されており、これが鶏肉飼料市場の成長に影響を与える可能性があります。2018~2019年にかけての豚インフルエンザと中国との貿易紛争は、畜産農業従事者が飼育増加に消極的であったため、歴史的期間中の家禽の個体数が安定する一因となりました。

- これらの課題にもかかわらず、肉と卵の消費の増加、輸出の増加、家禽の人口増加は、予測期間中の米国の飼料酵素市場の成長を促進すると予想されます。

多数の養殖場と飼料工場の存在が養殖用飼料生産の増加に貢献

- 米国における養殖用飼料生産は、合計6,232に上る多数の飼料工場の存在により、2022年には2017年比で4.1%増加しました。水産物の一人当たり消費量は2018年の21.88kgから2022年には22.26kgに増加しました。

- 様々な水産養殖飼料の中で、魚が主要なシェアを占め、2022年には83.2%を占めます。これは、人間の食事における魚の利点に対する意識の高まり、国際市場における高い需要、小売セクタの拡大、国内に多数の養魚場が存在するためです。養魚場の大半はオハイオ州にあり、最も消費されている魚はナマズで、これはペレット飼料をポンドの魚に変える能力があるためです。

- エビは2022年の養殖飼料市場の7.5%を占め、水産物需要の高まりと高タンパク質含量のため、他の最も消費される水生動物です。しかし、同国はエビを他国に依存しているため、調査期間中の成長に影響を与えました。二枚貝はメイン料理として人気があるため、COVID-19パンデミックの後、レストランからの需要が増加しています。飼料工場の数が多く、水産養殖の飼料生産量の増加に伴って魚介類の需要が高まっていることが、予測期間中の米国の飼料添加物市場の成長を促進すると予想されます。

米国の飼料用酵素産業概要

米国の飼料用酵素市場は適度に統合されており、上位5社で58.99%を占めています。この市場の主要企業は、Alltech、Inc.、Archer Daniel Midland Co.、Brenntag SE、DSM Nutritional Products AG、IFF(Danisco Animal Nutrition)などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- 魚類

- その他の養殖種

- 家禽類

- サブ動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adisseo

- Alltech, Inc.

- Archer Daniel Midland Co.

- BASF SE

- Brenntag SE

- Cargill Inc.

- DSM Nutritional Products AG

- Elanco Animal Health Inc.

- IFF(Danisco Animal Nutrition)

- Novus International, Inc.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

The United States Feed Enzymes Market size is estimated at 270.5 million USD in 2025, and is expected to reach 368.3 million USD by 2030, growing at a CAGR of 6.37% during the forecast period (2025-2030).

- In 2022, the United States held the largest share of the North American feed enzymes market, accounting for 70% of the total market. The feed enzymes market in the United States was valued at USD 0.2 billion, contributing 3.8% to the total feed additives market. The market value of feed enzymes in the United States witnessed a significant increase of 19.7% in 2020 compared to 2019, owing to the rise in feed production for ruminants and poultry birds.

- Of all the feed enzymes, carbohydrases occupied the largest market share of 47.6% in the United States, followed by phytases and other enzymes with a share of 33% and 19.5%, respectively. The use of carbohydrases in animal feed improves the absorption of nutrients from cereals, leading to reduced feed costs. Poultry birds, ruminants, and swine were the largest animal types in the carbohydrases segment, accounting for 41%, 37%, and 19% market shares, respectively.

- The feed carbohydrases segment is expected to grow and register a CAGR of 6.4% during the forecast period, owing to the high usage and demand for carbohydrases as a significant proportion of animal feed comprising carbohydrases. Most feed enzymes, including carbohydrases and phytases, cannot be synthesized naturally, and therefore, one or more enzymes should be supplied through the animal feed for all animal types.

- The demand for feed enzymes is increasing as it helps improve the overall health of animals, reduce livestock diseases, and enhance the stability and consistency of animal feed. Hence, the US feed enzymes market is expected to grow and register a CAGR of 6.3% during the forecast period.

United States Feed Enzymes Market Trends

The United States poultry industry is one of the largest commercial food industry and increased consumption of meats and eggs is increasing the poultry production

- The poultry industry in the United States is thriving due to the increasing demand for eggs and poultry meat in the commercial food industry and rising exports. The country is one of the largest egg producers and exporters in the world, with the total egg exports increasing by 9.3% to reach 3.5 billion eggs in 2020 compared to 2019 and the value of export growing by 2.4% to reach USD 189 million.

- The consumption of poultry meat in the United States improved due to favorable prices, a rise in awareness of a high-protein diet, and increasing demand for poultry meat. As a result, the poultry birds' headcount increased by 17.6 million in 2022 compared to 2021. Raising chickens in small spaces and different environments makes poultry production more feasible and less expensive than beef and pork, attracting animal farmers with limited rearing areas to invest in poultry farms.

- However, the share of the United States is expected to decrease from 26% in 2021 to 24% in 2031 in terms of imports, which may affect the growth of the poultry feed market. Swine flu and trade disputes with China between 2018 and 2019 contributed to the steady population of poultry during the historical period, as animal farmers were reluctant to increase rearing.

- Despite these challenges, the increasing consumption of meat and eggs, rising export, and the growing population of poultry are expected to drive the growth of the US feed enzymes market in the United States during the forecast period.

Presence of a large number of fish farms and feed mills is contributing to increasing feed production for aquaculture

- Aquaculture feed production in the United States increased by 4.1% in 2022 compared to 2017 due to the presence of a large number of feed mills in the country, which totaled 6,232. The per capita consumption of seafood increased from 21.88 kg in 2018 to 22.26 kg in 2022.

- Among the various aquaculture feed, fish holds a major share, accounting for 83.2% in 2022 due to the increasing awareness of the benefits of fish in the human diet, high demand in the international market, expansion of the retail sector, and the presence of a large number of fish farms in the country. The majority of fish farms are located in Ohio, and the most consumed fish is catfish, as it has the ability to convert pellet feed into pounds of fish.

- Shrimp accounted for 7.5% of the aquaculture feed market in 2022, as it is the other most consumed aquatic animal due to the rise in demand for seafood and its high protein content. However, the country depends on other countries for shrimp, which affected its growth during the study period. Other aquatic species witnessed high growth in demand, as the demand for bivalves from restaurants has increased after the COVID-19 pandemic due to their popularity as a main cuisine. The high number of feed mills and rising demand for fish and seafood with increasing feed production of aquaculture are expected to drive the growth of the feed additives market in the United States during the forecast period.

United States Feed Enzymes Industry Overview

The United States Feed Enzymes Market is moderately consolidated, with the top five companies occupying 58.99%. The major players in this market are Alltech, Inc., Archer Daniel Midland Co., Brenntag SE, DSM Nutritional Products AG and IFF(Danisco Animal Nutrition) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Carbohydrases

- 5.1.2 Phytases

- 5.1.3 Other Enzymes

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 fish

- 5.2.1.1.4 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 Archer Daniel Midland Co.

- 6.4.4 BASF SE

- 6.4.5 Brenntag SE

- 6.4.6 Cargill Inc.

- 6.4.7 DSM Nutritional Products AG

- 6.4.8 Elanco Animal Health Inc.

- 6.4.9 IFF(Danisco Animal Nutrition)

- 6.4.10 Novus International, Inc.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms