|

市場調査レポート

商品コード

1693564

米国の航空業界:市場シェア分析、産業動向、成長予測(2025年~2030年)US Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の航空業界:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 290 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

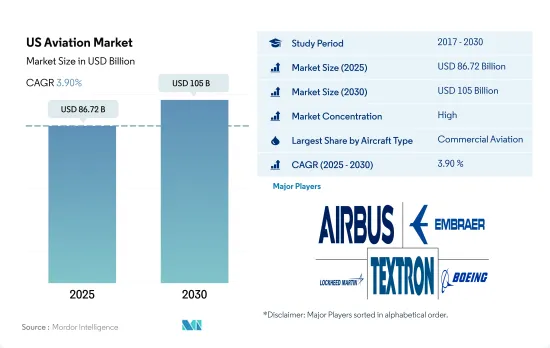

米国の航空市場規模は2025年に867億2,000万米ドルと推定され、2030年には1,050億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.90%で成長すると予測されます。

米国の航空市場で最大の市場シェアを占めると予想される民間航空セグメント

- 米国には、民間航空、軍事航空、一般航空を含む、世界最大かつ最も多様な航空市場があります。民間航空は米国経済において極めて重要な役割を担っており、何百万人もの旅客をつなぎ、膨大な量の貨物を国内外に輸送しています。人口の増加と可処分所得の増加により、米国の航空需要は安定しています。

- eコマースとグローバリゼーションは、航空貨物需要の大幅な成長を促しています。米国の航空会社が2022年に運んだ旅客数は、2021年比で1億9,400万人増加し、前年比30%増となりました。米国の軍事航空産業は、世界で最も技術的に進歩し、潤沢な資金を有する産業のひとつです。優位性を維持するため、米国軍は先進的戦闘機やステルス、自律システムなどの最先端技術の研究開発に継続的に投資しています。

- 2022年には、米国は世界の国防費軍事費の39%を占め、8,770億米ドル(0.7%)増加しました。一般航空は、民間航空、飛行訓練、航空調査、医療搬送など、非商業的な飛行活動を幅広くカバーしています。小型シングルユース機からビジネスジェット機まで、多様な航空機で構成されています。

- 米国の航空市場は、民間航空における安定した需要、軍用航空における継続的な近代化努力、一般航空における多様な活動に牽引され、繁栄を続けています。市場の成長は、技術革新、環境への配慮、消費者の嗜好の進化と絡み合っています。世界の相互関係がますます緊密化する中、米国の航空市場は今後も国の経済と安全保障の重要な柱であり続けると考えられます。

米国の航空市場の動向

制限の緩和と旅客数の増加が航空旅客輸送を促進

- 米国の航空会社の2022年の旅客数は、前年比30%増の1億9,400万人。2022年通年(1月から12月まで)の米国の航空会社の旅客数は8億5,300万人で、2021年の6億5,800万人、2020年の3億8,800万人を上回りました。その結果、米国の航空会社は合計でパンデミック前の92%、国際線では88.9%、国内線では92.45%の水準を回復しました。

- スケジュールによる2023年夏シーズンの計画キャパシティレベルを見ると、米国の航空会社が運航を計画した座席数は2019年夏より約6%多くなりました。パンデミック前の4年前は6億7,390万席だったのに対し、2023年夏は約7億1,560万席が運航予定でした。大手ネットワーク航空会社3社にも変化が見られ、アメリカン航空は2019年比で1.2%増の座席を予定していたが、Delta Air Linesは0.2%減、ユナイテッド航空は3.3%増でした。サウスウエスト航空は2019年に16.4%増の1億4,250万席、スピリット航空は42.8%増の3,540万席を運航する予定でした。

- 旅行需要の落ち込みとそれに伴う大手航空会社の損失により、航空会社は、主にワイドボディ機の納入予定を延期し、いくつかの機種の早期退役を通じて既存の航空機を再編成しました。例えば、2020年、Delta Air Linesは、COVID-19パンデミックによる収益への影響を軽減するため、227機の航空機を退役させました。このような退役延期は航空機OEMの納入スケジュールに影響を与え、2020年と2021年の生産率を下げざるを得なくなりました。

国防支出の増加は、米国が直面する様々な地政学的脅威に起因します。

- 2022年、米国は世界の国防費の39%を占め、軍事費は8,770億米ドル(0.7%)増加しました。2022年、米国は空軍省予算を発表し、そ概要によると、2023年度の予算要求は約1,940億米ドルで、2022年度の要求から202億米ドル(11.7%)増加しました。米国国防総省は、2023年度の取得資金(調達と研究開発・検査・評価(RDT& E))として2,760億米ドルを提案しており、内訳は調達が1,459億米ドル、RDT& Eが1,301億米ドルとなっています。予算で要求された資金は、国家防衛戦略の提言を実施するためのバランスの取れたポートフォリオ・アプローチです。

- 要求額2,760億米ドルのうち、565億米ドル(研究開発費168億米ドル、調達費396億米ドル)は、航空機の研究開発、航空機の取得、初期予備品、航空機支援装備品などの航空機と関連システムに充てられます。最も高額な防衛計画である第5世代F-35統合打撃戦闘機(JSF)は、海軍(F-35C)、海兵隊(F-35B&C)、空軍(F-35A)用の61機に対して110億米ドルの要求があります。2023年度の予算には、24機のF-15EX、79機の兵站支援機、119機の回転翼航空機、12機のUAV/UASの購入も含まれています。

- 米国陸軍の2022年度予算要求は1,730億米ドル、海軍は2,120億米ドル、空軍は2,130億米ドルでした。航空機と関連システム部門には、以下のサブグループが含まれる:戦闘機(230億米ドル)、貨物機(50億米ドル)、支援機(16億米ドル)で、残りはUAS、航空機支援、技術開発、航空機改造の予算です。

米国の航空産業概要

米国の航空市場はかなり統合されており、上位5社で86.35%を占めています。この市場の主要企業は、Airbus SE、Embraer、Lockheed Martin Corporation、Textron Inc.、The Boeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 航空貨物輸送量

- 国内総生産

- 収入旅客キロ(rpk)

- インフレ率

- アクティブフリートデータ

- 国防支出

- 個人富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 航空機タイプ

- 民間航空機

- サブ航空機タイプ別

- 貨物機

- 旅客機

- ボディタイプ別

- ナローボディ機

- ワイドボディ機

- 一般旅客機

- サブ航空機タイプ別

- ビジネスジェット

- ボディタイプ別

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- ピストン固定翼機

- その他

- 軍用機

- サブ航空機タイプ別

- 固定翼機

- ボディタイプ別

- 多用途航空機

- 訓練用航空機

- 輸送機

- その他

- 回転翼機

- ボディタイプ別

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 民間航空機

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Air Tractor Inc.

- Airbus SE

- ATR

- Bombardier Inc.

- Cirrus Design Corporation

- Dassault Aviation

- Embraer

- General Dynamics Corporation

- Honda Motor Co., Ltd.

- Leonardo S.p.A

- Lockheed Martin Corporation

- MD Helicopters LLC.

- Northrop Grumman Corporation

- Pilatus Aircraft Ltd

- Piper Aircraft Inc.

- Robinson Helicopter Company Inc.

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92658

The US Aviation Market size is estimated at 86.72 billion USD in 2025, and is expected to reach 105 billion USD by 2030, growing at a CAGR of 3.90% during the forecast period (2025-2030).

The Commercial Aviation Segment Is Expected To Occupy The Largest Market Share In The Us Aviation Market

- The United States is home to one of the world's largest and most diverse aviation markets, encompassing commercial aviation, military aviation, and general aviation. Commercial aviation plays a pivotal role in the US economy, connecting millions of passengers and transporting vast amounts of cargo across the nation and around the globe. With a growing population and increasing disposable incomes, the demand for air travel in the US remains steady.

- E-commerce and globalization have driven substantial growth in air cargo demand. The US airlines carried 194 million more passengers in 2022 than in 2021, up by 30% Y-o-Y. The US military aviation industry is one of the most technologically advanced and well-funded in the world. To maintain superiority, the US military continuously invests in research and development of advanced fighter jets and cutting-edge technologies, such as stealth and autonomous systems.

- In 2022, the US accounted for 39% of global defense spending military spending, which increased by USD 877 billion in 2022, or 0.7%. General aviation covers a wide range of non-commercial flying activities, including private aviation, flight training, aerial surveys, and medical evacuation. It comprises a diverse fleet of aircraft, from small single-engine planes to business jets.

- The US aviation market continues to thrive, driven by steady demand in commercial aviation, ongoing modernization efforts in military aviation, and the diverse activities of general aviation. The market's growth is intertwined with technological innovations, environmental considerations, and evolving consumer preferences. As the world becomes increasingly interconnected, the US aviation market is likely to remain a critical pillar of the nation's economy and security

US Aviation Market Trends

Ease of restrictions and rising passenger travel are driving air passenger traffic

- US airlines carried 194 million more passengers in 2022 than in 2021, up by 30% Y-o-Y. For the full year 2022, January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. As a result, US carriers recovered 92% of their pre-pandemic levels in total, 88.9% of international traffic, and 92.45% of domestic traffic.

- In terms of the planned capacity levels for the summer 2023 season based on schedules, the number of seats US airlines planned to operate was about 6% higher than during the summer of 2019. About 715.6 million seats were scheduled to operate in the summer of 2023, compared with 673.9 million four years ago, before the pandemic. The big three network carriers saw changes as well, with American Airlines scheduling 1.2% more seats compared to 2019, while Delta Air Lines was down by 0.2%, and United Airlines was up by 3.3%. Southwest Airlines intended to operate 142.5 million seats, up by 16.4% in 2019, and the capacity offered by Spirit Airlines was to be some 42.8% higher with 35.4 million seats.

- The drop in travel demand and the associated losses faced by major airlines have resulted in airlines deferring their expected deliveries, mostly of widebody aircraft, and restructuring their existing fleet through the early retirement of a few aircraft models. For instance, in 2020, Delta Air Lines retired 227 aircraft to reduce the impact of the COVID-19 pandemic on revenue. Such deferrals impacted the delivery schedules of aircraft OEMs and compelled them to reduce their production rates in 2020 and 2021.

The increase in defense spending can be attributed to the various geopolitical threats faced by the US

- In 2022, the US accounted for 39% of global defense spending military spending, which increased by USD 877 billion in 2022, or 0.7%. In 2022, the US released the Department of the Air Force budget, which outlined that for FY 2023, the budget request was approximately USD 194.0 billion, a USD 20.2 billion or 11.7% increase from the FY 2022 request. The US DoD proposed USD 276.0 billion in acquisition funds for FY2023 (Procurement and Research, Development, Test, and Evaluation (RDT&E)), which comprised USD 145.9 billion for Procurement and USD 130.1 billion for RDT&E. The financing requested in the budget is a balanced portfolio approach to implementing the National Defense Strategy recommendations.

- Of the USD 276 billion in the request, USD 56.5 billion (USD 16.8 billion for RDT&E and USD 39.6 billion for Procurement) will finance aircraft and related systems, including money for aircraft R&D, aircraft acquisition, initial spares, and aircraft support equipment. The single most expensive defense program, the fifth generation F-35 Joint Strike Fighter (JSF), has USD 11.0 billion in requests for 61 aircraft for the Navy (F-35C), Marine Corps (F-35B & C), and Air Force (F-35A). Funding for FY 2023 also included the purchase of 24 F-15EX, 79 logistics and support aircraft, 119 rotary wing aircraft, and 12 UAV/UAS.

- The US Army's budget request for FY 2022 was USD 173 billion, the Navy's was USD 212 billion, and the Air Force's request was USD 213 billion. The aircraft and related systems category includes the following subgroups: Combat Aircraft (USD 23.0 billion), Cargo Aircraft (USD 5.0 billion), Support Aircraft (USD 1.6 billion), with the remaining budget for UAS, aircraft support, technology development, and aircraft modifications.

US Aviation Industry Overview

The US Aviation Market is fairly consolidated, with the top five companies occupying 86.35%. The major players in this market are Airbus SE, Embraer, Lockheed Martin Corporation, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Training Aircraft

- 5.1.3.1.1.1.3 Transport Aircraft

- 5.1.3.1.1.1.4 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Air Tractor Inc.

- 6.4.2 Airbus SE

- 6.4.3 ATR

- 6.4.4 Bombardier Inc.

- 6.4.5 Cirrus Design Corporation

- 6.4.6 Dassault Aviation

- 6.4.7 Embraer

- 6.4.8 General Dynamics Corporation

- 6.4.9 Honda Motor Co., Ltd.

- 6.4.10 Leonardo S.p.A

- 6.4.11 Lockheed Martin Corporation

- 6.4.12 MD Helicopters LLC.

- 6.4.13 Northrop Grumman Corporation

- 6.4.14 Pilatus Aircraft Ltd

- 6.4.15 Piper Aircraft Inc.

- 6.4.16 Robinson Helicopter Company Inc.

- 6.4.17 Textron Inc.

- 6.4.18 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms