|

市場調査レポート

商品コード

1687230

北米の航空:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の航空:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

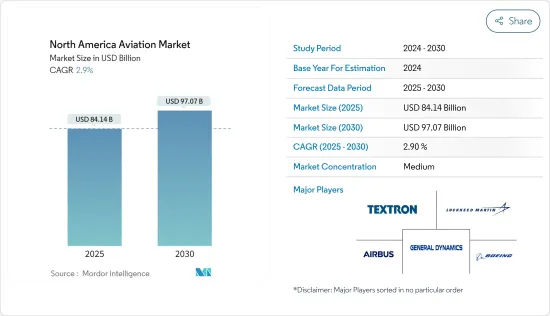

北米の航空市場規模は2025年に841億4,000万米ドルと推定され、市場推定・予測期間中(2025~2030年)のCAGRは2.9%で、2030年には970億7,000万米ドルに達すると予測されます。

格安航空会社(LCC)や超低価格航空会社(ULCC)の増加は、従来の航空会社のビジネスモデルを破壊してきました。これらの航空会社は競合運賃を提供することで、より多くの顧客層を獲得し、より多くの人々にとっての航空旅行の利便性を拡大しています。

様々な航空機メーカーの存在は、北米全体の航空産業の成熟につながりました。防衛産業もまた、ヘリコプターや戦闘機のための先進的な防衛ソリューションや研究開発能力を導入するための政府投資から恩恵を受けています。先進的な戦闘機、輸送機、練習機、ヘリコプターを地域の参入企業から調達することも、市場の成長に大きく貢献しています。燃料価格の上昇に伴い、企業は運航コストの増加を経験することが予想されます。燃料サーチャージは、航空機タイプや燃料価格の変動に応じて、1時間当たり600米ドルから1,000米ドル以上加算されます。このため、企業はコストを消費者に転嫁しなければならず、旅行コストの増加や利益率の低下につながります。こうした要因が市場の成長を妨げています。

さらに、同地域の一般航空市場の成長は、予測期間中、民間空港インフラの改善への注目の高まりと有利な規制変更によって支えられると予想されます。

北米の航空市場の動向

民間航空機セグメントは予測期間中に大幅な成長が見込まれる

予測期間中、北米の航空市場では民間航空機セグメントが大きな成長を遂げる見込みです。旅客機のニーズは主に、国内旅行が増加し続けていることから、この増加を後押ししています。

航空会社の機体拡大、燃費の良い飛行機への要望の高まり、航空旅行の増加、ゼロエミッション2050年目標に向けた産業のシフトが民間航空機の需要を促進しています。2023年8月までに、この地域ではBoeing1,474機、Airbus986機が納入される見込みです。米国は、引き渡し待ちの航空機2,405機の唯一の所有者です。そのため、予測期間中、同国は大きな成長を遂げると予想されます。

American Airlines、Delta Air Lines、United Airlineのような主要企業は、2024年に大幅な航空機納入を予定しており、 Air Canadaのような貨物会社は急速に成長し、航空機を更新しています。2024年1月、Delta Air Linesは、A350-1,000を20機発注することで、燃費の良い新型ワイドボディ機の要件を満たすためにAirbusを選択しました。Delta Air Linesは450機以上のAirbus機を運航しており、200機以上を発注中です。これらの進歩は、予測期間中、民間航空機産業の拡大を促進すると予測されます。

米国は予測期間中に大きな成長を遂げる見込み

米国は世界最大の航空市場のひとつであることから、今後数年間で顕著な拡大が見込まれます。航空旅行のニーズの高まりを受けて、米国の複数の航空会社が機材を強化し、技術的に先進的な航空機を取得しています。2023年6月、United Parcel Serviceは、今後2年以内に55機の航空機を導入し、機材を増強する意向を発表しました。その大半は請負業者が運航する小型フィーダー機で、同社は2023~2025年の間にB777F型機を8機追加導入することも目指しています。

民間航空に加えて、米国は資金の大半を軍事費に充てています。SIPRIによると、米国の軍事費は2023年に約2.3%増加し、総額9,160億米ドルとなり、世界の国防費の37%を占める世界トップの地位を確固たるものにします。米国は今後10年間、防衛産業において一貫した成長を遂げると予測されており、これは旧式の戦闘機をより先進的なバージョンにアップグレードする意図があるためです。米国海兵隊は、AV-8BハリアーIIと旧式のF/A-18ホーネットの後継機として、F-35Bを約340機、F-35Cを約80機取得する計画です。

2024年4月、米国は、MiG-31迎撃機、MiG-27戦闘爆撃機、MiG-29戦闘機、Su-24爆撃機など117機の軍用機を競売で落札したカザフスタンから、81機のソ連時代の戦闘機と爆撃機を購入しました。結論として、予測期間を通じて市場を拡大させると予想されます。

北米の航空産業概要

北米の航空市場には、Boeing、AirbusSE、Lockheed Martin、Textron Inc.、General Dynamics Corporationなどの大手企業が含まれます。これらの大手航空機メーカーの存在により、市場は非常に競争が激しくなっています。さらに、世界中の航空機生産のほとんどがこの地域にあり、製造、販売、サポートの拠点があるため、この地域は国際的な航空宇宙サプライヤーにとっての焦点となっています。

この地域の航空市場を掌握するため、各社は新たなアプローチの導入、オファリングの拡大、労働効率の改善、サプライチェーン・パートナーの獲得、他社との合併、新市場への参入、競合価格の提供など、さまざまな成長戦術を駆使しています。協力と提携は、北米の航空宇宙メーカーが採用する極めて重要な成長戦術です。その多くは、国際的な企業と協力し、新しい技術や製品を生み出すための知識や技術を交換しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 民間航空機

- 旅客機

- 貨物機

- 軍用機

- 戦闘機

- 非戦闘機

- 一般旅客機

- ヘリコプター

- ピストン固定翼機

- ターボプロップ機

- ビジネスジェット機

- 民間航空機

- 地域

- 米国

- カナダ

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Airbus SE

- Lockheed Martin Corporation

- The Boeing Company

- General Dynamics Corporation

- Textron Inc.

- Embraer SA

- Bombardier Inc.

- Pilatus Aircraft Ltd

- Leonardo SpA

- Dassault Aviation SA

- Piper Aircraft Inc.

- Honda Aircraft Company

第7章 市場機会と将来動向市場機会と今後の動向

The North America Aviation Market size is estimated at USD 84.14 billion in 2025, and is expected to reach USD 97.07 billion by 2030, at a CAGR of 2.9% during the forecast period (2025-2030).

An increase in low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs) has disrupted the traditional airline business model. These carriers offer competitive fares, enticing a larger customer base and expanding air travel accessibility to more people.

The presence of various aircraft manufacturers has led to the maturation of the aviation industry across North America. The defense industry has also benefited from government investments in introducing advanced defense solutions and research and development capabilities for helicopters and fighter jets. Procuring advanced fighter jets, transport and trainer aircraft, and helicopters from regional players has also contributed significantly to market growth. With fuel prices increasing, companies are expected to experience increased operating costs. Fuel surcharges add USD 600 to over USD 1,000 per hour, depending on aircraft types and fuel price changes. Due to this, companies have to transfer the costs to the consumers, which increases trip costs or cuts their profit margin. Such factors hamper the market's growth.

Moreover, the growth of the general aviation market in the region is anticipated to be supported by the growing focus on improving private airport infrastructure and favorable regulatory changes during the forecast period.

North American Aviation Market Trends

The Commercial Aircraft Segment is Expected to Witness Significant Growth During the Forecast Period

The commercial aircraft segment is expected to witness significant growth in the North American aviation market during the forecast period. The need for passenger planes mainly fuels this increase as domestic trips continue to rise.

Expansion of airline fleets, rising desire for fuel-efficient planes, growth in air travel, and the industry's shift toward the zero-emission 2050 target are driving the demand for commercial aircraft. By August 2023, 1,474 Boeing and 986 Airbus aircraft were expected to be delivered in the region. The United States is the sole owner of 2,405 aircraft awaiting delivery. Therefore, the country is anticipated to experience significant growth over the forecast period.

Leading airlines like American Airlines, Delta Air Lines, and United Airlines have significant aircraft deliveries scheduled for 2024, and cargo companies like Air Canada are rapidly growing and updating their fleets. In January 2024, Delta Air Lines selected Airbus to fulfill its requirements for new, fuel-efficient widebody aircraft by ordering 20 A350-1000 planes. Delta Air Lines has over 450 Airbus aircraft in operation and more than 200 on order. These advancements are projected to fuel expansion in the commercial aircraft industry over the forecast period.

The United States is Expected to Witness Significant Growth During the Forecast Period

The United States is anticipated to experience notable expansion in the coming years, as it ranks among the biggest aviation markets globally. In response to the growing need for air travel, multiple US airlines are enhancing their fleets and acquiring technologically advanced aircraft. In June 2023, United Parcel Service announced its intention to increase its fleet by incorporating 55 aircraft within the next two years. Most of these will be small feeder planes operated by contractors, and the company also aims to introduce an additional eight B777F aircraft between 2023 and 2025.

In addition to civil aviation, the United States allocates most of its funds to its military. As per the SIPRI, the US military spending rose by around 2.3% in 2023, totaling USD 916 billion, solidifying its position as the top defense spender globally, accounting for 37% of worldwide expenditure. The United States is projected to experience consistent growth in the defense industry in the next ten years, as it intends to upgrade its outdated fighter jets with more advanced versions. The US Marine Corps plans to acquire approximately 340 F-35B and 80 F-35C models to replace the AV-8B Harrier II and old F/A-18 Hornet jets.

In April 2024, the United States bought 81 Soviet-era fighter and bomber planes from Kazakhstan, which sold 117 military aircraft in an auction, including MiG-31 interceptors, MiG-27 fighter bombers, MiG-29 fighters, and Su-24 bombers. In conclusion, these developments are expected to expand the market throughout the forecast period.

North American Aviation Industry Overview

The aviation market in North America includes major companies like The Boeing Company, Airbus SE, Lockheed Martin Corporation, Textron Inc., and General Dynamics Corporation. Due to the existence of these large aircraft manufacturers, the market has become very competitive. Moreover, this area is a focal point for international aerospace suppliers because most of the aircraft production across the world is located here, where they have manufacturing, sales, and support establishments.

To control the aviation market in the region, the companies use various growth tactics, including implementing new approaches, expanding offerings, improving workforce efficiency, acquiring supply chain partners, merging with other companies, entering new markets, and offering competitive prices. Cooperation and alliances are crucial growth tactics that aerospace manufacturers in North America embrace. Many of them work with international companies to exchange knowledge and skills to create new technologies and products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Segmentation

- 5.1 Type

- 5.1.1 Commercial Aircraft

- 5.1.1.1 Passenger Aircraft

- 5.1.1.2 Freighter Aircraft

- 5.1.2 Military Aircraft

- 5.1.2.1 Combat Aircraft

- 5.1.2.2 Non-combat Aircraft

- 5.1.3 General Aviation

- 5.1.3.1 Helicopter

- 5.1.3.2 Piston Fixed-wing Aircraft

- 5.1.3.3 Turboprop Aircraft

- 5.1.3.4 Business Jet

- 5.1.1 Commercial Aircraft

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

6 Competitive Landscape

- 6.1 Vendor Market Share

- 6.2 Company Profile

- 6.2.1 Airbus SE

- 6.2.2 Lockheed Martin Corporation

- 6.2.3 The Boeing Company

- 6.2.4 General Dynamics Corporation

- 6.2.5 Textron Inc.

- 6.2.6 Embraer SA

- 6.2.7 Bombardier Inc.

- 6.2.8 Pilatus Aircraft Ltd

- 6.2.9 Leonardo SpA

- 6.2.10 Dassault Aviation SA

- 6.2.11 Piper Aircraft Inc.

- 6.2.12 Honda Aircraft Company