中東・アフリカの航空:市場シェア分析、産業動向、成長予測(2025年~2030年)

Middle East and Africa Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 282 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693560

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

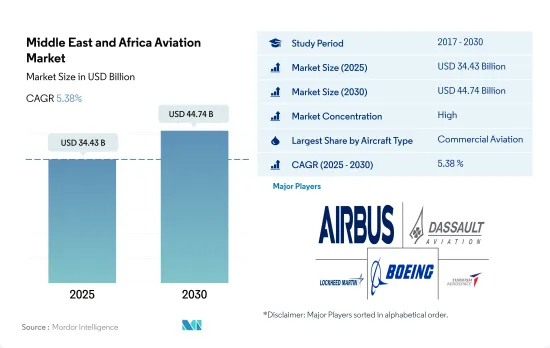

中東・アフリカの航空市場規模は、2025年には344億3,000万米ドルと推定され、2030年には447億4,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.38%で成長します。

民間航空は2023年に70.6%の主要金額シェアを記録

- 中東・アフリカのGDPは2021年比で20%増加し、パンデミック以前の水準と比較すると17%増加したため、中東・アフリカの経済状況は安定しているように見えます。2022年6月現在、同地域の航空部門は1,110万人の雇用と2,760億米ドルのGDPを支えています。

- 予測期間中、民間航空部門はより高い成長率で拡大すると予想されます。中東地域の航空会社は、2022年の需要が2021年比で116.2%増加することを示しました。国際路線と長距離便の再開に伴い、旅客機の需要は予測期間中(2022~2030年)に66%増加すると予測されます。

- かなりの数のHNWIとUHNWIがいるため、中東はビジネス航空部門にとって有利な産業であることが証明されています。2016~2021年にかけて、中東のHNWIは86%増加し、アフリカのそれは19%増加しました。その高い豪華さと快適性から、大きなキャビンと航続距離を持つビジネスジェットは中東で高い需要があります。2022年7月現在、大型ジェット機は中東の50%、アフリカの36%を占めています。

- 中東・アフリカの軍事航空は、トルコ、クウェート、カタール、バーレーンによる様々な航空機調達計画により、今後数年間で成長すると予想されます。アフリカの軍事費は6%増加し、中東では8%増加しました。この地域の国々は、老朽化した軍用機の近代化と次世代航空機の調達に多額の投資を行っているため、固定翼航空機の成長率が高くなる可能性があります。

艦隊のアップグレードと更新プログラムが需要を牽引

- 中東地域は、2022年4月現在、世界の航空旅客輸送量の約6.5%を占めています。中東の航空会社は、2022年4月の需要が2021年4月と比べて265%増加したことを示しました。同様に、アフリカ地域は、2022年4月現在、世界の航空旅客輸送量の約1.9%を占めていました。アフリカ地域の航空会社の2022年4月の需要は、2021年4月と比較して116.2%増加しました。

- 民間航空機セグメントの納入量は、2021年比で2022年に約96%の伸びを示しました。OEMは、生産、サプライチェーンの停止、ロックダウンによる輸送問題、国内と国際路線に影響を与えた旅行制限などの問題を経験しました。予測期間中、中東・アフリカには約1,080機以上の民間航空機が納入される見込みです。

- 一般航空セグメントでは、トルコが中東全体のビジネスジェット機保有台数の約22.3%を占め、ビジネスジェット機の稼動台数でトップの国であり、次いでサウジアラビア、アラブ首長国連邦、イスラエルがそれぞれ約20%、2022年時点の納入台数の12%を占めています。アフリカでは、南アフリカとナイジェリアがそれぞれビジネスジェット機保有台数の25%と23%を占めています。

- 中東地域の国防費は、2022年には約1,840億米ドルとなり、2022年比で3.2%以上減少しました。一方、アフリカでは2022年に約394億米ドルで、2021年から5%以上減少しました。

- 予測期間中、アラブ首長国連邦、サウジアラビア、カタール、トルコなどの中東諸国が航空機のアップグレードのために新型機を調達すると予想されるため、同地域の航空機保有台数は増加する可能性があります。

中東・アフリカの航空市場の動向

アジア市場の再開により、湾岸諸国のハブ空港を経由するトラフィックが増加

- 中東・アフリカの航空会社にとって、航空旅客輸送量の回復は力強いものであり、2023年第1四半期の前年同期比成長率は87.1%と64.6%でした。中東・アフリカでは、2022年の国際線・国内線旅客数は2021年比で15%増加しました。中東でも持続的な回復がみられ、イランとクウェートの旅行者数がそれぞれ26%、4%完全回復に至らなかった以外は、ほとんどの国で回復がみられました。ヨルダン、カタール、サウジアラビア、アラブ首長国連邦は、2019年と比較して力強い成長数を記録しました。

- 2022年第4四半期、エジプトとナイジェリアは旅客輸送量がパンデミック前の水準を20%以上上回りました。カタールの旅客数は同期間に前年同期比で40%近く増加したが、これはアラブ諸国で初めて開催されたワールドカップに参加した旅行者が後押ししました。しかし、南アフリカ、イラン、クウェートの旅客数は、2022年第4四半期の時点で、パンデミック前の水準をまだ10%以上下回っています。

- IATAによると、国際線で世界一利用者の多いハブ空港であるドバイ国際空港(DXB)の2023年第3四半期の旅客数は2,290万人を記録し、四半期ベースで2019年以降最高となり、1年間で約40%増加しました。

- 2022年のロードファクタは、中東・アフリカ系航空会社でそれぞれ77%と80%に達し、2021年のロードファクタと比較して10ポイント以上上昇しました。これらの事実は、COVID-19規制後も旅行の回復が勢いを増していることを示しています。中東の多くの主要国際路線では、すでにCOVID-19以前の水準を上回っています。観光と高い旅行意欲は、中東・アフリカにおける産業の回復を引き続き促進しています。

中東地域の主要軍事大国は国防費を急増させています。

- 中東地域の2022年の国防費は約1,840億米ドルで、2021年に比べて3.2%以上減少しました。一方、アフリカでは2022年に約394億米ドルで、2021年から5%以上減少しました。サウジアラビア、エジプト、カタール、アラブ首長国連邦、アルジェリアといった国々は、2017年から22年にかけて国防支出が多かった地域の主要国です。これらの国々は、固定翼セグメントのマルチロール機や実用機の積極的な調達プログラムを持っています。

- サハラ以南のアフリカの軍事費の合計は、2022年に203億米ドルとなり、2021年比で7.3%、2013年比で18%減少しました。同地域の2大支出国であるナイジェリアと南アフリカが、2022年の軍事費減少を主導しました。2022年、イスラエルの軍事費は2009年以来初めて減少しました。総額234億米ドルは2021年より4.2%減少しました。

- サウジアラビアの軍事費の前年比(YoY)成長率は、2022年には2021年比で16%増となり、2018年以来の前年比増となりました。サウジアラビアの昨年の軍事費は750億米ドルと見積もられていました。この削減は、サウジアラビアがイエメンから軍人を撤収させ始めたという非難と重なりました。しかし、サウジ政府はこの疑惑を否定し、人員は再配置されているだけだと主張しました。2015年以来、サウジアラビアは戦争で荒廃したイエメンに対する軍事作戦で連合国を率いており、戦闘は2022年まで続きました。サウジアラビアの軍事予算はGDPの7.4%と、2022年のウクライナに次いで世界第2位でした。

中東・アフリカの航空産業概要

中東・アフリカの航空市場はかなり統合されており、上位5社で72.57%を占めています。この市場の主要企業は、Airbus SE、Dassault Aviation、Lockheed Martin Corporation、The Boeing Company、Turkish Aerospace Industriesなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 航空貨物輸送量

- 国内総生産

- 収入旅客キロ(rpk)

- インフレ率

- アクティブフリートデータ

- 国防支出

- 個人富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 航空機タイプ

- 民間航空機

- サブ航空機タイプ別

- 貨物機

- 旅客機

- ボディタイプ別

- ナローボディ機

- ワイドボディ機

- 一般旅客機

- サブ航空機タイプ別

- ビジネスジェット

- ボディタイプ別

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- ピストン固定翼機

- その他

- 軍用機

- サブ航空機タイプ別

- 固定翼機

- ボディタイプ別

- 多用途航空機

- 訓練用航空機

- 輸送機

- その他

- 回転翼機

- ボディタイプ別

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 民間航空機

- 国名

- アルジェリア

- エジプト

- カタール

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Dassault Aviation

- Embraer

- General Dynamics Corporation

- Leonardo S.p.A

- Lockheed Martin Corporation

- Pilatus Aircraft Ltd

- The Boeing Company

- Turkish Aerospace Industries

- United Aircraft Corporation

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Middle East and Africa Aviation Market size is estimated at 34.43 billion USD in 2025, and is expected to reach 44.74 billion USD by 2030, growing at a CAGR of 5.38% during the forecast period (2025-2030).

Commercial aviation registered a major value share of 70.6% in 2023

- The economic condition in the Middle East & Africa looks stable as the region's GDP increased by 20% over 2021 and 17% compared to the pre-pandemic levels. As of June 2022, the region's aviation sector supported 11.1 million jobs and USD 276 billion in the GDP.

- During the forecast period, the commercial aviation segment is anticipated to expand with higher growth. The airline companies of the Middle Eastern region witnessed a 116.2% rise in demand in 2022 compared to 2021. With the reopening of international routes and long-haul flights, the demand for passenger aircraft is projected to increase by 66% during the forecast period (2022-2030).

- Due to a significant number of HNWIs and UHNWIs, the Middle East has proven to be a lucrative industry for the business aviation sector. From 2016 to 2021, HNWIs in the Middle East increased by 86%, while those in Africa increased by 19%. Due to their high level of luxury and comfort, business jets with large cabins and extended ranges are in high demand in the Middle East. As of July 2022, large jets accounted for 50% of the Middle Eastern and 36% of the African fleet.

- Military aviation in the Middle East & Africa is expected to grow in the coming years, owing to various aircraft procurement plans by Turkey, Kuwait, Qatar, and Bahrain. Military spending in Africa increased by 6% and by 8% in the Middle East. Fixed-wing aircraft may account for higher growth as countries in the region invest heavily in modernizing their aging military fleets and procuring next-generation aircraft.

Fleet upgradation and replacement programs driving the demand

- The Middle Eastern region had a share of around 6.5% of the global air passenger traffic as of April 2022. The airline companies of the Middle East witnessed a 265% rise in demand in April 2022 compared to April 2021. Similarly, the African region had a share of around 1.9% of the global air passenger traffic as of April 2022. The airline companies of the African region witnessed a 116.2% rise in demand in April 2022 compared to April 2021.

- The deliveries in the commercial aircraft segment witnessed a growth of around 96% in 2022 compared to 2021. The OEMs experienced problems such as a halt in production, supply chain, transportation issues due to lockdowns, and travel restrictions that impacted domestic and international routes. During the forecast period, around 1,080+ commercial aircraft are expected to be delivered to the Middle East & Africa.

- In the general aviation sector, Turkey was the leading country in terms of the active operational fleet of business jets, with around 22.3% of the overall Middle Eastern business jet fleet, followed by Saudi Arabia, the United Arab Emirates, and Israel, with around 20% each and 12% of the deliveries as of 2022. In Africa, South Africa and Nigeria accounted for 25% and 23% of the business jet fleet, respectively.

- Defense expenditures in the Middle Eastern region were around USD 184 billion in 2022, a decline of over 3.2% compared to 2022. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021.

- During the forecast period, the active fleet may increase in the region, as Middle Eastern countries like the UAE, Saudi Arabia, Qatar, and Turkey are expected to procure newer aircraft for fleet upgradation.

Middle East and Africa Aviation Market Trends

The re-opening of Asian markets is boosting traffic through Gulf hubs

- Air passenger traffic recovery has been strong for the African and Middle Eastern carriers, with year-over-year growth of 87.1% and 64.6% in the first quarter of 2023. In the Middle East & Africa, the number of international and domestic travelers increased by 15% in 2022 compared to 2021. The Middle East has also seen sustained recovery, with most countries having rebounded, except for Iran and Kuwait, where traffic was 26% and 4% short of full recovery, respectively. Jordan, Qatar, Saudi Arabia, and the United Arab Emirates posted strong growth numbers compared to 2019.

- In Q4 2022, Egypt and Nigeria witnessed their passenger traffic perform over 20% above pre-pandemic levels. Qatar's traffic increased nearly 40% Y-o-Y over the same period, boosted by travelers attending the first World Cup hosted in the Arab country. However, passenger volumes in South Africa, Iran, and Kuwait are still more than 10% below their pre-pandemic levels as of Q4 2022.

- According to IATA, The world's busiest hub for international traffic, Dubai International Airport (DXB) recorded 22.9 million passengers in the third quarter of 2023, the highest quarterly traffic since 2019, rising by nearly 40% over a year.

- In 2022, load factors reached 77% and 80% for the Middle Eastern & African airlines, respectively, up more than ten percentage points compared to the 2021 load factors. These facts indicate that the travel recovery continues to gather momentum post the COVID-19 restrictions. Many major international route areas within the Middle East are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry's recovery in the Middle East & Africa.

Major military powers in the region have surged their defense expenditure

- Defense expenditures in the Middle Eastern region were around USD 184 billion in 2022, a decline of over 3.2% compared to 2021. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021. Countries such as Saudi Arabia, Egypt, Qatar, United Arab Emirates, and Algeria were the major countries in the region with a high defense expenditure during 2017-22. They have active procurement programs for multi-role and utility aircraft in fixed-wing segments.

- Sub-Saharan Africa's combined military expenditure stood at USD 20.3 billion in 2022, down by 7.3% compared to 2021 and 18% compared to 2013. Nigeria and South Africa, the sub-regions two largest spenders, led the decline in military spending in 2022. In 2022, Israel's military spending fell for the first time since 2009. Its total of USD 23.4 billion was 4.2% lower than in 2021.

- The year-on-year (Y-o-Y) growth in Saudi Arabia's military spending was 16% in 2022 compared to 2021, the first Y-o-Y increase since 2018. Saudi Arabia's military expenditure was estimated at USD 75.0 billion last year. The reduction coincided with accusations that Saudi Arabia had started to remove its military personnel from Yemen. However, the Saudi government denied the allegations and insisted that the personnel were just being redeployed. Since 2015, Saudi Arabia has been leading a coalition in a military campaign against the war-torn nation of Yemen, and the fighting continued into 2022. Saudi Arabia had the second-largest military budget in the world, at 7.4% of GDP, after Ukraine in 2022.

Middle East and Africa Aviation Industry Overview

The Middle East and Africa Aviation Market is fairly consolidated, with the top five companies occupying 72.57%. The major players in this market are Airbus SE, Dassault Aviation, Lockheed Martin Corporation, The Boeing Company and Turkish Aerospace Industries (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Training Aircraft

- 5.1.3.1.1.1.3 Transport Aircraft

- 5.1.3.1.1.1.4 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 South Africa

- 5.2.6 United Arab Emirates

- 5.2.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Dassault Aviation

- 6.4.3 Embraer

- 6.4.4 General Dynamics Corporation

- 6.4.5 Leonardo S.p.A

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Pilatus Aircraft Ltd

- 6.4.8 The Boeing Company

- 6.4.9 Turkish Aerospace Industries

- 6.4.10 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 282 Pages

- 納期

- 2~3営業日