|

市場調査レポート

商品コード

1690919

インドの航空・防衛・宇宙:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Aviation, Defense, And Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの航空・防衛・宇宙:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

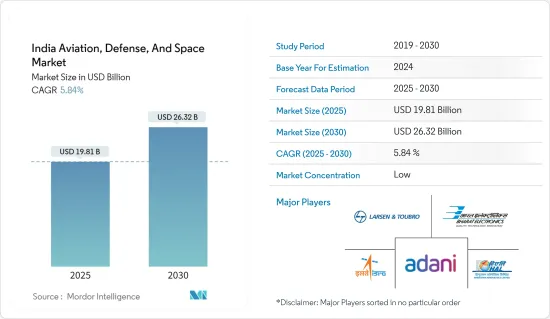

インドの航空・防衛・宇宙の市場規模は2025年に198億1,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5.84%で、2030年には263億2,000万米ドルに達すると予測されます。

航空旅客のニーズを満たすための商用航空機の取得増加、商用航空事業の増加、商用空港建設数の増加が、予測期間中の市場を牽引すると予想されます。また、インドの国防予算の増加、同国の国防能力を向上させるための先端兵装の取得増加、宇宙開発計画の増加、国産防衛製造に対する政府支援の増加が、今後数年間の市場を押し上げると予想されます。

一方、国内における規制の増加は、長期的には市場の成長を妨げると予想されます。さらに、空港の建設や設計、軍事訓練、監視、宇宙ミッションの精度向上など、人工知能などの先端技術の利用が拡大していることから、さまざまな市場機会の成長が見込まれています。

インドの航空・防衛・宇宙市場の動向

著しい成長を見せる民間航空部門

- 近年、インドの航空部門は目覚ましい成長を遂げ、世界第3位の地位を固めています。この急成長を後押ししているのは、主に旅行意欲の高まりを伴う人口の増加です。その結果、空の旅をより充実したものにするため、最新の航空機に対する需要が急増しています。これを受けて、インドの民間航空会社数社は、最新鋭機の導入に多額の投資を行っています。

- 例えば、2023年9月、エア・インディアはHSBCとのファイナンス・リースを通じ、同社初のA350-900を確保しました。エア・インディアは合計6機のA350-900を発注しました。5機は2024年3月までに引き渡される予定でした。さらに、インドでは新しい空港の建設数が顕著に増加しています。年間航空旅客数の増加に伴い、インドの既存空港は混雑やボトルネックに悩まされており、新空港の開発が急増しています。例えば、アヨーディヤのマリヤダ・プルショッタム・シュリ・ラーム国際空港は2023年12月に開港しました。このようなインフラストラクチャーの進歩は、今後数年間の同部門の成長を後押しするものと思われます。

武器・軍需分野が市場を独占

- インドは、特に中国との国境紛争の激化を背景に、国防費を大幅に増強しています。このため、インド国防軍は先進的な兵器や弾薬の獲得を優先し、その能力を強化しています。同時に、多くの企業がインドの防衛部門と提携し、軍の進化する要求に応えるために研究投資を増やしています。例えば、2023年9月、インド陸軍は、600億米ドルという高額を投じて、国内企業が独占的に開発・製造する次世代砲の計画を発表しました。これらの新しい曳光弾銃システムは、軽量で適応性が高く、最先端技術を誇ると宣伝されています。

- インドはまた、先進的な155ミリ砲弾薬の製造拠点としての世界の役割も狙っています。この野心を裏付けるように、2023年2月、国防省は国内メーカー5社に契約を発注しました。これらの契約は、39口径、45口径、52口径にまたがる陸軍の既存の155mm砲用の155mm末端誘導弾(TGM)約2,000発の納入を伴うものです。国産兵器の生産が増加し、国防支出が堅調に推移していることから、この部門は当面大きな成長を遂げる可能性があります。

インドの航空・防衛・宇宙産業の概要

インドの航空・防衛・宇宙市場は断片化されており、様々なプレーヤーが市場を独占しています。主な市場プレイヤーには、Hindustan Aeronautics Limited(HAL)、Bharat Electronics Limited(BEL)、Indian Space Research Organisation(ISRO)、Larsen &Toubro Limited、Adani Groupなどがあります。

いくつかの市場プレーヤーは、長期的に国の防衛能力を強化するために、インド政府と合弁事業を形成しています。このような協力関係は、インドの防衛力を強化するだけでなく、地域プレーヤーの市場プレゼンスも強化します。さらに、特にジェット推進システムや国産兵器、民間航空機、宇宙部品の生産などの分野で提携が盛んになり、新たな機会が生まれています。この動向は、今後数年間で大幅な成長を促進するものと思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 空軍別

- 戦闘機・非戦闘機(固定翼・ヘリコプター)・UAV

- 兵器・軍需品

- MRO

- 陸軍別

- 装甲車、ヘリコプター、UAV

- 兵器・軍需品

- MRO

- 海軍

- 艦艇、戦闘機、非戦闘機、UAV

- 兵器・軍需品

- MRO

- 宇宙

- 人工衛星

- ロケット・ローバー

- 民間航空

- 民間航空機

- ビジネスジェット

- MRO

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Hindustan Aeronautics Limited(HAL)

- Indian Ordnance Factories

- Bharat Electronics Limited(BEL)

- Goa Shipyard Limited

- Hinduja Group

- Kalyani Steels Ltd(KSL)

- Tata Sons Private Limited

- Larsen & Toubro Limited

- Mahindra & Mahindra Limited

- Mistral Solutions Pvt. Ltd

- Adani Group

- Indian Space Research Organisation(ISRO)

第7章 市場機会と今後の動向

The India Aviation, Defense, And Space Market size is estimated at USD 19.81 billion in 2025, and is expected to reach USD 26.32 billion by 2030, at a CAGR of 5.84% during the forecast period (2025-2030).

The growing acquisition of commercial aircraft to meet the needs of air passengers, increasing commercial aviation operations, and the growth in the number of commercial airport constructions are anticipated to drive the market during the forecast period. In addition, the growth in India's defense budget, increasing acquisition of advanced armaments to improve the country's defense capabilities, growth in the number of space programs, and increasing governmental support for indigenous defense manufacturing are expected to boost the market in the coming years.

On the other hand, growth in regulations within the country is expected to hamper the market's growth in the long run. Furthermore, the growing use of advanced technologies such as artificial intelligence for airport construction and design, military training, surveillance, and improving accuracy for space missions, amongst others, is anticipated to lead to growth in various market opportunities.

India Aviation, Defense, and Space Market Trends

Civil Aviation Segment to Showcase Remarkable Growth

- In recent years, the Indian aviation sector has experienced remarkable growth in operations, solidifying its position as the world's third-largest. An increasing population with a growing appetite for travel primarily fuels this surge. Consequently, there has been a surge in demand for modern aircraft to enhance the flying experience. In response, several commercial airlines in India are investing substantially in acquiring cutting-edge aircraft.

- For example, in September 2023, Air India secured its first A350-900 through a finance lease with HSBC. Air India placed orders for a total of six A350-900s. Five units were scheduled for delivery by March 2024. Furthermore, India has seen a notable rise in the number of new airport constructions. With a rising number of air passengers annually, existing airports in India are grappling with congestion and bottlenecks, prompting a surge in new airport developments. For instance, the Maryada Purushottam Shri Ram International Airport in Ayodhya was inaugurated in December 2023. Such infrastructural strides are poised to bolster the sector's growth in the coming years.

The Weapons and Munitions Segment Dominates the Market

- India has significantly boosted its defense spending, driven by escalating border disputes, notably with China. This has prompted the Indian defense forces to prioritize acquiring advanced weaponry and ammunition, bolstering their capabilities. Simultaneously, numerous companies have partnered with India's defense sector, increasing their research investments to meet the military's evolving demands. For instance, in September 2023, the Indian Army announced plans for next-gen guns to be exclusively developed and manufactured by domestic firms with a hefty price tag of USD 60 billion. These new towed gun systems are touted to be lighter and more adaptable, boasting cutting-edge technology.

- India is also eyeing a global role as a manufacturing hub for advanced 155 mm artillery ammunition, a caliber favored by more than 75 armies worldwide. Underscoring this ambition, in February 2023, the Ministry of Defense awarded contracts to five domestic manufacturers. These contracts entail delivering around two thousand 155 mm terminally guided munitions (TGMs) for the Army's existing 155 mm guns, spanning 39, 45, and 52 calibers. With the uptick in indigenous weapon production and robust defense spending, this sector is primed for significant growth in the foreseeable future.

India Aviation, Defense, and Space Industry Overview

The Indian aviation, defense, and space market is fragmented, with various players dominating it. Some of the major market players are Hindustan Aeronautics Limited (HAL), Bharat Electronics Limited (BEL), Indian Space Research Organisation (ISRO), Larsen & Toubro Limited, and Adani Group.

Several market players are forming joint ventures with the Indian government to bolster the nation's defense capabilities in the long term. These collaborations not only enhance India's defense but also strengthen the market presence of regional players. In addition, new opportunities emerge as partnerships flourish, especially in sectors such as jet propulsion systems and the production of indigenous weapons, commercial aircraft, and space components. This trend is poised to drive substantial growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Air Force

- 5.1.1 Combat and Non-combat Aircraft (Fixed Wing and Helicopter) and UAVs

- 5.1.2 Weapons and Munitions

- 5.1.3 MRO

- 5.2 By Army

- 5.2.1 Armored Vehicles, Helicopters, and UAVs

- 5.2.2 Weapons and Munitions

- 5.2.3 MRO

- 5.3 By Navy

- 5.3.1 Naval Vessels, Combat and Non-combat Aircraft, and UAVs

- 5.3.2 Weapons and Munitions

- 5.3.3 MRO

- 5.4 By Space

- 5.4.1 Satellite

- 5.4.2 Launch Vehicles and Rovers

- 5.5 By Civil Aviation

- 5.5.1 Commercial Aircraft

- 5.5.2 Business Jet

- 5.5.3 MRO

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Hindustan Aeronautics Limited (HAL)

- 6.2.2 Indian Ordnance Factories

- 6.2.3 Bharat Electronics Limited (BEL)

- 6.2.4 Goa Shipyard Limited

- 6.2.5 Hinduja Group

- 6.2.6 Kalyani Steels Ltd (KSL)

- 6.2.7 Tata Sons Private Limited

- 6.2.8 Larsen & Toubro Limited

- 6.2.9 Mahindra & Mahindra Limited

- 6.2.10 Mistral Solutions Pvt. Ltd

- 6.2.11 Adani Group

- 6.2.12 Indian Space Research Organisation (ISRO)