|

市場調査レポート

商品コード

1693545

フランスの航空:市場シェア分析、産業動向、成長予測(2025年~2030年)France Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの航空:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 244 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

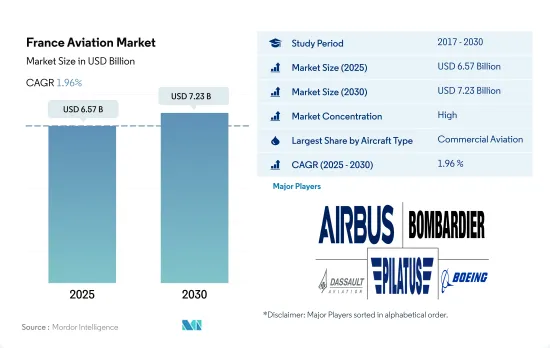

フランスの航空市場規模は2025年に65億7,000万米ドルと推定・予測され、2030年には72億3,000万米ドルに達し、予測期間(2025~2030年)のCAGRは1.96%で成長すると予測されます。

大手OEMの存在と民間機、一般機、軍用機の調達増が市場成長を牽引

- フランスは、その規模と地理的位置、エールフランスやAirbusといった産業のフラッグシップ企業の存在により、トラフィックの点で欧州最大かつ最も重要な航空市場のひとつです。納入機数では、2021年に民間航空部門で22機、一般航空部門で7機のビジネスジェット機と45機のヘリコプターが調達され、2020年比で民間航空部門が23%増、一般航空部門が13%増となりました。

- フランスの航空宇宙産業は、現在の市場の不確実性とフランス政府の航空宇宙支援計画により、技術の大幅な転換を経験しており、これがフランスにおけるこのセグメントの成長を牽引しています。軍事航空部門は、研究開発への政府投資の増加や、地元企業による先進的な戦闘機、ヘリコプター、輸送機・訓練機の調達によって恩恵を受けています。

- 納入は生産停止やロックダウンの影響を受けているが、このセグメントはプラスを維持しています。フランスの一般航空市場は、民間空港のインフラ整備に重点が置かれるようになり、国内の富裕層が増加していることから、予測期間中に拡大する可能性があります。

- 2020年のCOVID-19発生時には、ビジネスジェットの納入が減少しました。しかし、ピストン固定翼、ターボプロップ、ヘリコプターの各セグメントの納入機数は引き続き好調を維持しました。2021年には、これらすべてのセグメントでパンデミック発生前の納入数を上回ります。

フランスの航空市場の動向

国内旅行者の需要増加が航空旅客輸送を牽引

- フランス発着の旅客数では欧州が最大の市場であり、アフリカ、北米がこれに続きます。欧州からの旅客数は約5,830万人(全体の71.3%)、アフリカからの旅客数は970万人(同11.8%)、北米からの旅客数は490万人(同5.9%)でした。フランスのGDPに対する航空輸送と航空会社などの関連産業全体の貢献は約870億米ドルです。

- フランスの航空旅客数は2022年に0.02%増加しました。フライト時間が長くなると燃料消費量が増加し、特定の路線では運航コストが急上昇する可能性があります。燃料費の増加は特に航空会社に影響を及ぼし、その結果、航空券価格の上昇を通じて旅客のコストが増加します。また、経路変更とフライト時間の延長は、航空旅客に不便をもたらし、フライトが完全にキャンセルされるリスクが高まるため、旅客の信頼を低下させる可能性があります。ウクライナ情勢の予測不可能性は、フランスの航空会社にとって大きな課題となり、航空旅客数の回復をさらに遅らせる可能性が高いです。

- 同様に、フランスのによる主要空港では、2020年中の旅客数が68%以上減少しました。旅行規制の緩和による旅客数の回復は、フランスの大手航空会社によって確認されました。2021年には、約3,580万人の旅客がエールフランス-KLMによって運ばれました。全体的な航空旅客輸送量は予測期間中に急増すると予想されます。

地政学的脅威が国防費増加の原動力

- 同国の国防費は2021~2022年にかけて0.6%急増し、2022年には536億米ドルとなりました。同国の国防費はGDPの1.9%でした。2022年、フランスはドイツに次いで欧州第3位の国防支出国でした。2017~2022年にかけて、同国の国防費は約9%急増しました。

- フランス経済はパンデミックの影響を受け、施錠や渡航制限により経済活動が縮小したにもかかわらず、フランス政府は安全保障能力を確保するため、2021年に国防費を急増させました。フランスではLPMとして知られる軍事計画法(Military Programming Law 2019~2025)は、防衛施策のガイドラインと国の資源を定義しています。これには、2022年までに約14億7,000万米ドル、次いで2023年までに33億9,000万米ドルのフランス国防予算の増額が盛り込まれています。LPMは、2019~2025年の間に総額3,340億米ドルを国防費に割り当てています。

- フランスの国防費は、他の欧州諸国や主要軍事大国の国防費と比較して、2,000年以降14.5%も急増しています。例えば、ドイツの国防費は2,000年以降21.6%も急増しています。英国の国防費は20%増、中国は495%増、ロシアは183%増、米国は61%増です。フランスの国防費は、新しい兵器や装備の調達と既存の装備のアップグレードによる軍事の近代化を重視しています。フランス政府は、2つの主要プログラム、すなわち、独仏とスペインの未来型戦闘航空システム(FCAS)(約3億2,522万米ドル)と、次世代戦車プログラムである主力地上戦闘システム(MGCS)(6,567万米ドル)に資金を割り当てています。

フランスの航空産業概要

フランスの航空市場はかなり統合されており、上位5社で103.51%を占めています。この市場の主要企業は、Airbus SE、Bombardier Inc.、Dassault Aviation、Pilatus Aircraft Ltd、The Boeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 航空貨物輸送量

- 国内総生産

- 収入旅客キロ(rpk)

- インフレ率

- アクティブフリートデータ

- 国防支出

- 個人富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 航空機タイプ

- 民間航空機

- サブ航空機タイプ別

- 貨物機

- 旅客機

- ボディタイプ別

- ナローボディ機

- ワイドボディ機

- 一般旅客機

- サブ航空機タイプ別

- ビジネスジェット

- ボディタイプ別

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- ピストン固定翼機

- その他

- 軍用機

- サブ航空機タイプ別

- 固定翼機

- ボディタイプ別

- 多用途航空機

- 訓練用航空機

- 輸送機

- その他

- 回転翼機

- ボディタイプ別

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 民間航空機

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Bombardier Inc.

- Dassault Aviation

- Embraer

- Leonardo S.p.A

- Pilatus Aircraft Ltd

- Robinson Helicopter Company Inc.

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92610

The France Aviation Market size is estimated at 6.57 billion USD in 2025, and is expected to reach 7.23 billion USD by 2030, growing at a CAGR of 1.96% during the forecast period (2025-2030).

Presence of Major OEMs and the Rising Procurement of Commercial, General, and Military Aircraft Drive the Market Growth

- France is one of the largest and most important aviation markets in Europe in terms of traffic due to its size and geographic location and the presence of some of the industry's flagships, such as Air France and Airbus. In terms of deliveries, 22 aircraft were procured in the commercial aviation segment, while seven business jets and 45 helicopters were procured in the general aviation segment in 2021, a 23% rise for commercial aviation and a 13% rise for general aviation from 2020.

- The French aerospace industry is experiencing a significant shift in technology due to the current market uncertainty and the French government's aerospace assistance plan, which is driving the growth of this sector in France. The military aviation sector has benefitted due to the increasing government investment in R&D and the procurement of advanced fighter jets, helicopters, and transport and training aircraft from the local players.

- Though the deliveries have been affected by a halt in production and lockdowns, this segment remained positive. The general aviation market in France could expand over the forecast period due to an increasing emphasis on improving the infrastructure of private airports and the increasing number of HNWIs in the country.

- During the COVID-19 outbreak in 2020, there was a decline in business jet deliveries. However, the piston fixed-wing, turboprop, and helicopter segments remained strong in terms of aircraft deliveries. In 2021, all these segments exceeded the pre-pandemic deliveries.

France Aviation Market Trends

Increased demand from domestic travelers is driving the air passenger traffic

- Europe is the biggest market for passenger flows to and from France, followed by Africa and North America. About 58.3 million passengers traveled from Europe (71.3% of the total), 9.7 million passengers reached France from Africa (11.8%), and 4.9 million passengers arrived from North America (5.9%). The contribution of the overall air transportation and its allied industries, such as airlines, to the French GDP, is around USD 87 billion.

- Air passenger numbers in France increased by 0.02% in 2022. Longer flights will cause an increase in fuel consumption and can result in a sharp increase in operating costs for certain routes. The increasing fuel costs will particularly impact airlines, therefore resulting in increased costs to passengers through higher ticket prices. Re-routing and longer flights may also cause inconvenience for air passengers, with an increased risk of flights being canceled completely and may decrease passenger confidence. The unpredictability of the situation in Ukraine is likely to be a major challenge for airlines in France and further delay the recovery in air passenger numbers.

- In 2021, the airport had a passenger movement of around 482,676 p.a. Similarly, another major airport in France had a drop of over 68% in passenger traffic during 2020. The recovery in passenger traffic with ease in travel restrictions was witnessed by the major French airlines. In 2021, around 35.8 million passengers were carried by Air France-KLM. The overall air passenger traffic is anticipated to surge during the forecast period.

Geopolitical threats are the driving factor for rising defense expenditure

- The country's defense expenditure surged by 0.6% from 2021 to 2022, with USD 53.6 billion in 2022. The defense expenditure of the country was 1.9% of the GDP. In 2022, France was the third-largest country in terms of defense expenditure in Europe after Germany. During 2017-2022, the country's defense expenditure surged by around 9%.

- Despite the French economy being impacted by the pandemic, which led to reduced economic activities due to imposed lockdowns and travel restrictions, the French government surged its defense expenditure in 2021 to ensure its security capabilities. The Military Programming Law 2019-2025, known as LPM in France, defines the defense policy guidelines and the resources for the country. It includes an increase in France's defense budget by around USD 1.47 billion by 2022, followed by an increase of USD 3.39 billion by 2023. The LPM has allotted a total of USD 334 billion to defense expenditures between 2019 and 2025.

- France's defense spending has surged by 14.5% since 2000 compared to the defense expenditures of other European nations and major military powers. For instance, Germany's defense expenditure has surged by 21.6% since then. The United Kingdom's defense expenditure surged by 20%, China's by 495%, Russia's by 183%, and the United States' by 61%. The French defense expenditure emphasizes the modernization of the armed forces by procurement of newer arms and equipment and the upgradation of the existing ones. The French government is allocating funds for two major programs, namely, the Franco-German-Spanish Future Combat Air System or FCAS (around USD 325.22 million) and the Main Ground Combat System, or MGCS, a next-generation tank program (USD 65.67 million).

France Aviation Industry Overview

The France Aviation Market is fairly consolidated, with the top five companies occupying 103.51%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, Pilatus Aircraft Ltd and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Training Aircraft

- 5.1.3.1.1.1.3 Transport Aircraft

- 5.1.3.1.1.1.4 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Dassault Aviation

- 6.4.4 Embraer

- 6.4.5 Leonardo S.p.A

- 6.4.6 Pilatus Aircraft Ltd

- 6.4.7 Robinson Helicopter Company Inc.

- 6.4.8 Textron Inc.

- 6.4.9 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms