|

市場調査レポート

商品コード

1692556

中国の道路貨物輸送:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の道路貨物輸送:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 277 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

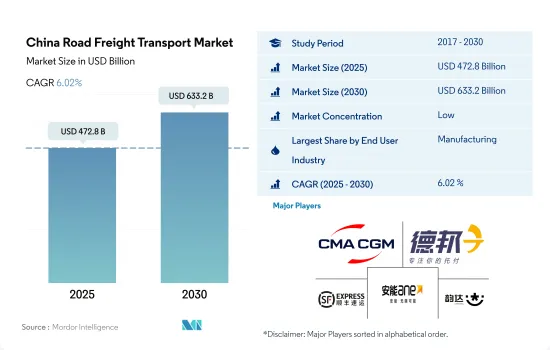

中国の道路貨物輸送市場規模は2025年に4,728億米ドルと推定され、2030年には6,332億米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは6.02%で成長する見込みです。

製造業の生産高増加とeコマースが道路貨物サービスの需要を牽引

- 製造業の生産量の増加は、トラック運送業界が国内での製造品のタイムリーな配達と流通を確保する上で重要な役割を果たしているため、道路サービスの需要を促進しています。中国の製造業は、世界の地政学や他の新興経済国との競合による課題に直面しているにもかかわらず、繁栄しています。2023年には、中国の製造業の付加価値はGDPの31.7%を占める。さらに、中国は新興アジア製造業指数2024のトップに位置しています。2024年4月の中国の工業生産高は前年同月比6.7%増と、製造業の回復に支えられ、2024年3月の同4.5%増を上回りました。

- 道路、橋、空港などの大規模インフラ建設プロジェクトの開発が、建設エンドユーザー・セグメントを牽引しています。建設業界は、第14次5ヵ年計画(FYP)(2021~2025年)の一環としてのインフラ・プロジェクトへの投資に支えられ、2025~2028年の間にCAGR3.9%を記録すると予想されます。2060年までに13兆8,000億米ドルをグリーン電力転換に投資するという政府の計画も成長を支えるものと予想されます。その結果、建設エンドユーザー部門は今後数年間で成長すると予想されます。

中国の道路貨物輸送市場の動向

第14次5ヵ年計画におけるクリーンエネルギーインフラの開発と輸送部門への投資の重点化が成長を牽引

- 2023年、中国のクリーンエネルギー部門は同国の経済拡大に大きく貢献しました。エネルギー・アンド・クリーン・エア(CREA)によると、中国の再生可能エネルギーインフラへの投資額は8,900億米ドルに達し、同年の化石燃料供給への世界の投資額にほぼ匹敵しました。再生可能エネルギー源、原子力、電力網、エネルギー貯蔵、電気自動車(EV)、鉄道を含むクリーンエネルギーは、2023年には中国のGDPの9.0%を占め、前年比7.2%から増加します。EVの生産台数は2023年に前年比36%増加しました。

- 第14次5カ年計画(2021~2025年)において、中国は交通網拡大の目標を明らかにしました。2025年までに、高速鉄道は2020年の38,000kmから50,000kmに拡大し、人口50万人以上の都市の95%を250kmの路線でカバーします。2025年までに、鉄道を165,000km、民間空港を270以上、都市部の地下鉄を10,000km、高速道路を190,000km、高水準内陸水路を18,500kmにすることを目指しています。2025年までに総合的な開発を達成することが第一の目標であり、交通システムの変革とGDPへの貢献の進展を重視しています。

ロシア・ウクライナ戦争の中、中国のディーゼルガソリン小売価格は歴史的な高水準に高騰しました。

- 2023年、中国の原油輸入量は2022年比11%増の5億6,399万トン、1日当たり1,128万バレルとなりました。この急増は、ロシア・ウクライナ戦争の中で世界の原油価格が上昇し、中国の燃料価格が歴史的な高値に達したためです。2024年1-2月期の原油輸入量は前年同期比5.1%増の8,831万トンに達しました。この増加は、先に安い価格で原油を購入したことによる。ブレント先物は2023年9月に97.69米ドルでピークを迎え、12月には72.29米ドルまで下落し、2024年3月には84.05米ドルまで上昇しました。2024年3月にOPEC+グループが減産を6月末まで延長すると決定したことで、原油価格はさらに上昇しました。同グループは世界需要の6%近くを減産するため、この動きは世界の石油需要に対する懸念を高めています。また、最近の原油価格の上昇は、2024年下半期以降の中国の輸入を減退させる可能性があります。

- 中国は、最近の世界の原油価格の変動に合わせて、ガソリンと軽油の小売価格を調整する予定です。今回の値上げは、世界の供給逼迫と需要見通しの好転を反映したものです。NDRCによると、中国のガソリンとディーゼルの価格は2024年にトン当たり28米ドル上昇します。燃料需要の減少が予想されるもの、2035年まで石油ベースの燃料が主要な選択肢であり続けると思われます。

中国の道路貨物輸送産業の概要

中国の道路貨物輸送市場は断片化されており、CMA CGMグループ(CEVAロジスティクスを含む)、Depponロジスティクス、SFエクスプレス(KEX-SF)、Shanghai Aneng Juchuang Supply Chain Management、Yunda Holding(アルファベット順)が主要5社となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 経済活動別GDP分布

- 経済活動別GDP成長率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 物流実績

- 道路の長さ

- 輸出動向

- 輸入動向

- 燃料価格動向

- トラック輸送コスト

- タイプ別トラック保有台数

- 主要トラックサプライヤー

- 道路貨物トン数の動向

- 道路貨物価格動向

- モーダルシェア

- インフレ率

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 輸出先

- 国内貨物

- 国際貨物

- トラック積載量

- 全トラック積載(FTL)

- 小口貨物(LTL)

- コンテナ輸送

- コンテナ輸送

- コンテナなし

- 輸送距離

- 長距離輸送

- 短距離輸送

- 商品構成

- 流体商品

- 固体商品

- 温度制御

- 非温度制御

- 温度制御

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A.P. Moller-Maersk

- Changjiu Logistics

- China Post

- CMA CGM Group(including CEVA Logistics)

- Deppon Logistics Co., Ltd.

- DHL Group

- SF Express(KEX-SF)

- Shanghai Aneng Juchuang Supply Chain Management Co., Ltd.

- Shanghai YTO Express(Logistics)Co., Ltd.

- SINOTRANS

- STO Express Co., Ltd.(Shentong Express)

- Yunda Holding Co. Ltd

- ZTO Express

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の物流市場の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界バリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

- 為替レート

The China Road Freight Transport Market size is estimated at 472.8 billion USD in 2025, and is expected to reach 633.2 billion USD by 2030, growing at a CAGR of 6.02% during the forecast period (2025-2030).

Rise in manufacturing sector's output and e-commerce driving the demand for road freight services

- The rise in manufacturing production is driving the demand for road services as the trucking industry plays a significant role in ensuring the timely delivery and distribution of manufactured goods domestically. China's manufacturing sector thrives despite facing challenges due to global geopolitics and competition from other emerging economies. In 2023, the value-added by China's manufacturing accounted for 31.7% of its GDP. Moreover, China is at the top of the Emerging Asia Manufacturing Index 2024. China's industrial output grew 6.7% YoY in April 2024, up from the 4.5% growth in March 2024, supported by the recovery in the manufacturing sector.

- Developing large-scale infrastructure construction projects such as roads, bridges, and airports is driving the construction end-user segment. The construction industry is expected to record an average annual growth rate of 3.9% between 2025 and 2028, supported by investment in infrastructure projects as part of the 14th Five-Year Plan (FYP) (2021-2025). The government's plan to invest USD 13.8 trillion by 2060 in green power transformation is also expected to support the growth. As a result, the construction end-user segment is expected to grow in the coming years.

China Road Freight Transport Market Trends

Rising focus on developing clean energy infrastructure and transport sector investment under 14th Five-Year Plan driving growth

- In 2023, China's clean energy sector significantly contributed to the country's economic expansion. According to Energy and Clean Air (CREA), China's investment in renewable energy infrastructure amounted to USD 890 billion, almost matching global investments in fossil fuel supply for the same year. Clean energy, including renewable energy sources, nuclear power, electricity grids, energy storage, electric vehicles (EVs), and railways, constituted 9.0% of China's GDP in 2023, up from 7.2% YoY. EV production grew by 36% YoY in 2023.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

China's retail diesel and gasoline prices were soared to historically high levels amid the Russia-Ukraine War

- In 2023, China imported 11% more crude oil than in 2022, totaling 563.99 mn metric tons (MMT), or 11.28 mn barrels per day. This surge was due to increased global crude oil prices amid the Russia-Ukraine War, causing fuel prices in China to reach historic highs. In Jan-Feb 2024, crude oil imports rose by 5.1% YoY, reaching 88.31 MMT. This increase was driven by purchasing crude oil at lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, fell to USD 72.29 in December, and rose to USD 84.05 by March 2024. The decision made by the OPEC+ group in March 2024 to extend output cuts until the end of June has further boosted crude prices. This move has raised concerns about global oil demand, as the group is reducing production by nearly 6% of world demand. The recent increase in crude prices may also dampen China's imports starting from H2 2024.

- China plans to adjust retail prices for gasoline and diesel to align with recent shifts in global crude oil prices. The price hike reflects a tightening of global supply and a positive forecast for demand. According to NDRC, gasoline and diesel prices in China will increase by USD 28 per ton in 2024. Although there's expectation of declining demand for fuels, oil-based fuels will remain the primary choice until 2035.

China Road Freight Transport Industry Overview

The China Road Freight Transport Market is fragmented, with the major five players in this market being CMA CGM Group (including CEVA Logistics), Deppon Logistics Co., Ltd., SF Express (KEX-SF), Shanghai Aneng Juchuang Supply Chain Management Co., Ltd. and Yunda Holding Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 Changjiu Logistics

- 6.4.3 China Post

- 6.4.4 CMA CGM Group (including CEVA Logistics)

- 6.4.5 Deppon Logistics Co., Ltd.

- 6.4.6 DHL Group

- 6.4.7 SF Express (KEX-SF)

- 6.4.8 Shanghai Aneng Juchuang Supply Chain Management Co., Ltd.

- 6.4.9 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.10 SINOTRANS

- 6.4.11 STO Express Co., Ltd. (Shentong Express)

- 6.4.12 Yunda Holding Co. Ltd

- 6.4.13 ZTO Express

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate