|

市場調査レポート

商品コード

1690980

欧州動物性タンパク質:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州動物性タンパク質:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 258 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

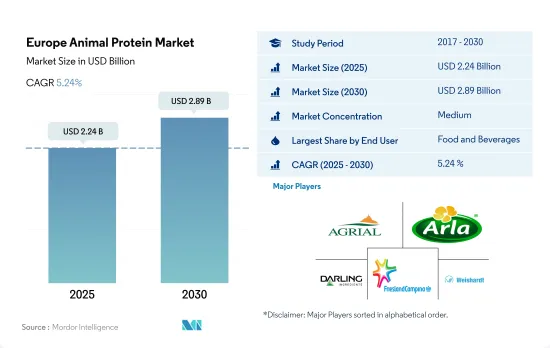

欧州の動物性タンパク質市場規模は2025年に22億4,000万米ドルと推定・予測され、2030年には28億9,000万米ドルに達し、予測期間(2025~2030年)のCAGRは5.24%で成長すると予測されています。

フィットネス愛好家の増加と地域全体でのタンパク質ベースの食品需要の増加により、2022年にはF&Bとサプリメントが合わせてシェアの50%以上を占めます。

- 市場は多くのエンドユーザーセグメントで動物性タンパク質の用途があり、主にF&Bとサプリメントのセグメントが牽引しています。2022年には、この2つのセグメントを合わせて、欧州で消費される動物性タンパク質量の40%のシェアを占めました。タンパク質ベースの製品における乳化剤としてのゼラチンの消費の増加が、市場を牽引する主要因です。2021年には、ミレニアル世代とZ世代の消費者の60%が、欧州で機能性ベーカリーを提供するキュレーションベーカリーを求めていました。

- サプリメントは、この地域で増加するフィットネス愛好家の間で受け入れられています。実際、サプリメントセグメントでは、スポーツ/パフォーマンス栄養が最も優勢で、しかも最も急成長しているサブセグメントであり続け、予測期間中の予測CAGRは数量ベースで5.40%でした。予測期間中、欧州のヘルス&フィットネスクラブの会員数は約1,200万人増加しました。この増加は、プロテイン粉末のような製品にとって大きな可能性を示しています。トップアスリートは、世界中のミレニアル世代にますます影響を与えています。このため、精力増強製品や体重管理用スポーツ栄養剤の需要が急増しています。

- 昆虫タンパク質は動物飼料市場を独占しており、予測期間を通じて金額ベースで2.39%のCAGRで推移すると予想されています。欧州では、このセグメントの設立以来10億米ドル以上が投資されており、この数字は予測期間終了時には29億5,000万米ドルに達すると予想されます。家禽や豚の飼料における昆虫加工動物性タンパク質(PAP)の使用は2021年に欧州連合によって承認されており、こうした動物用飼料へのこうした成分の導入を皮切りに、新たな機会が創出されることが期待されます。

ロシアのベーカリーからの動物性タンパク質の旺盛な需要により、ロシアが2022年に大きなシェアを占める

- 国別では、ロシアが2022年もトップの座を維持しました。飲食品が動物性タンパク質の最大の消費者であり続け、ベーカリー部門が基準年の54%の主要量を占めました。ゼラチンやコラーゲンなどの動物性タンパク質は、ケーキやペストリーの製造に広く使用されています。ケーキとペストリーは第2位の産業で、この地域の市場シェアの11%を占めています。ロシア国民の平均年間消費量は約260ポンドです。2020年には、690を超える大規模ベーカリー、4,800の中堅企業、7,000を超える小規模・零細ベーカリーが存在します。

- 英国のホエイプロテイン市場は、欧州で26.27%のシェアを占めています。欧州で最も強力な市場の一つです。ホエイプロテインは、英国ではサプリメントや飲食品産業での用途が拡大しています。2020年には約350万人の英国人が3型糖尿病に罹患していると記録されています。糖尿病に対処するために、ホエイプロテインはインスリンレベルを即座に上昇させるので効果的です。ホエイプロテインサプリメントの摂取は、3型糖尿病患者の血糖値コントロールに役立ちます。その結果、サプリメントセグメントにおける乳清タンパク質の需要は着実に増加しています。

- 動物性タンパク質市場ではドイツが大きなシェアを占めています。ゼラチン・プロテイン(26.85%)とホエイ・プロテイン(20.14%)が大きなシェアを占めています。ゼラチン・プロテインは飲食品セクタが支配的で、飲料サブセグメントが市場で最も急成長しています。2021年、ドイツ人は一人当たり平均9.9リットルのフルーツジュースを消費します。ゼラチンは、ヘイズの原因となる果汁の沈殿物を除去するのに効果的です。ゼラチンは1%~5%の濃度で使用される場合、天然液の保持を助け、食感と風味を改善します。

欧州動物性タンパク質市場の動向

動物性タンパク質の消費拡大が原料カテゴリーの主要企業のビジネス機会を促進

- 英国では、2016~2019年にかけて、19~64歳の個人の1日平均タンパク質摂取量は1人当たり76gで、成人の1日平均必要摂取量の64g/日を上回りました。この数値は、1日あたり体重0.83g/kgの摂取基準値を用いて算出されました。1人当たりの1日平均動物性タンパク質消費量は39.6gと予測され、25.9gが肉と肉製品から、9.9gが牛乳と牛乳製品から摂取されています。それに伴い、国内の牛乳生産量は増加しています。国内生産量の7%以下が輸出され、メーカーが容易に入手できるようになっています。

- ホエイプロテイン市場は、主にフィットネスセンターやヘルスクラブの人気の高まりによって、ホエイ消費量の増加に繋がっています。ホエイ・プロテインの年間輸入量は、2019~2021年にかけて15.09%飛躍的に増加しました。しかし、健康全般に大きな注目が集まり、消費者のクリーンラベル製品への関心が高まる中、スポーツ栄養産業では天然材料への需要が高まっています。オーガニックや牧草飼育のホエイなどの原料は、健康と倫理的な懸念から注目されています。

- 女性は、引き締まった体、筋力、パフォーマンスのためにスポーツ栄養サプリメントを求めています。栄養士やその他のフィットネス専門家からの奨励も、この地域におけるスポーツ栄養の市場センチメントを後押ししています。菜食主義の高まり、植物性製品に対する需要、消費者の食生活の嗜好の変化は、世界的に確認されています。消費者の間では、肉ベースの製品への志向の低さが目立ち、これが動物性タンパク質市場の主要抑制要因となっています。欧州の菜食主義者は130万人から260万人に倍増し、2021年には人口の3.2%を占めます。

肉と牛乳の生産は、植物性タンパク質メーカーの原料として大きく貢献しています。

- グラフは、牛、豚、鶏の肉(骨付き、生、チルド)、牛とヤギの生乳、牛のスキムミルク、乾燥ホエイ粉末の生産データです。ドイツはEUにおける生乳の主要生産国であり、2020年にはEUにおける生乳出荷量の21%以上を占めます。ドイツでは畜産農業従事者数が減少しているが、平均的な畜産規模は増加しています。生乳生産量の増加は、牛1頭当たりの生乳生産量の増加に起因しています。長年にわたり、生乳生産はドイツ北西部と南部の草原地帯に集中しています。

- 英国では、乳牛の数が減少し続けているにもかかわらず、生乳生産量は絶えず増加しています。2022年12月現在、英国の12ヵ月齢以上の乳牛の総頭数は266万頭です。同年、牛1頭当たりの年間乳量は8,169リットルとなり、2017年の7,893リットルと比べて3.5%増加しました。

- 2020年、欧州連合(EU)の牛の頭数は7,600万頭を超え、牛肉生産量は680万トンに達し、EUは米国、ブラジルに次ぐ世界第3位の生産国となりました。この部門は、牛群の規模、農場の構造、EU内の農場の地理的分布の点で多様です。3つのEU加盟国だけでEUの牛肉の半分を生産しています。フランス(21.2%)、ドイツ(17.8%)、イタリア(11.1%)です。

欧州動物性タンパク質産業概要

欧州動物性タンパク質市場は、上位5社で40.63%を占め、適度に統合されています。この市場の主要企業は、Agrial Enterprise、Arla Foods amba、Darling Ingredients Inc.、Koninklijke FrieslandCampina NV、SAS Gelatines Weishardtなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タンパク質タイプ

- カゼインとカゼイネート

- コラーゲン

- 卵タンパク質

- ゼラチン

- 昆虫プロテイン

- ミルクプロテイン

- ホエイプロテイン

- その他動物性タンパク質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Agrial Enterprise

- Arla Foods amba

- Darling Ingredients Inc.

- Groupe LACTALIS

- Koninklijke FrieslandCampina NV

- Lactoprot Deutschland GmbH

- LAITA

- SAS Gelatines Weishardt

- Ynsect

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Europe Animal Protein Market size is estimated at 2.24 billion USD in 2025, and is expected to reach 2.89 billion USD by 2030, growing at a CAGR of 5.24% during the forecast period (2025-2030).

F&B and supplements together accounted for more than 50% of share in 2022 due to rising number of fitness enthusiasts coupled with increasing demand for protein-based food products across the region

- The market has animal protein applications in many end-user segments, primarily driven by the F&B and supplements segments. In 2022, the two segments together held a share of 40% of animal protein volume consumed in Europe. Increased consumption of gelatin as an emulsifier in protein-based products is the major factor driving the market. In 2021, 60% of millennials and Gen Z consumers sought curated baked bakeries that offered functional bakery goods in Europe.

- The supplements have been gaining acceptance among the rising number of fitness enthusiasts in the region. In fact, under the supplements segment, sports/performance nutrition remained the most dominant and yet the fastest-growing sub-segment, with a projected CAGR of 5.40%, by volume, during the forecast period. Over the review period, the number of members in health and fitness clubs in Europe rose by about 12 million. This increase portrays a vast potential for products like protein powders. Top athletes are increasingly influencing millennials worldwide. Due to this, the demand for energizing products and weight management sports nutrition is surging.

- Insect protein dominates the animal feed market and is anticipated to register a CAGR of 2.39%, by value, throughout the forecast period. In Europe, more than USD 1 billion has been invested in this sector since its establishment, and this figure is expected to reach USD 2.95 billion at the end of the forecast period. The use of insect-processed animal proteins (PAPs) in poultry and pig feed was approved by the European Union in 2021, which is expected to create new opportunities, beginning with the introduction of such components into such animals' diets.

Russia holds significant share in 2022 due to strong demand of animal protein from Russian bakeries

- By country, Russia retained its top position in 2022. Food and beverages remained the largest consumer of animal proteins, with the bakery segment accounting for a major volume of 54% during the base year. Animal proteins, such as gelatin and collagen, are widely used in making cakes and pastries. Cakes and pastries make up the second-largest industry, holding 11% of the market shares in the region. An average Russian citizen consumes about 260 pounds of baked goods per year. In 2020, the country had over 690 large bakeries, 4,800 mid-sized enterprises, and more than 7,000 small and micro-bakeries.

- The UK whey protein market holds a share of 26.27% in Europe. It is one of the strongest markets in Europe. Whey protein has increased applications in the supplements and food and beverage industries in the United Kingdom. Almost 3.5 million Britons were recorded to have had type-3 diabetes in 2020. To cope with diabetes, whey protein is effective as it instantly increases the insulin level. The intake of whey protein supplements helps people with type-3 diabetes control their blood sugar levels. As a result, there is a steady increase in the demand for whey protein in the supplements segment.

- Germany holds a significant share of the animal protein market. Gelatin protein (26.85%) and whey protein (20.14%) hold the major market shares in the country. Gelatin protein is dominated by the food and beverage sector, and the beverage sub-segment is the fastest-growing in the market. In 2021, an average German consumed 9.9 liters per capita of fruit juice. Gelatin is effective in removing fruit juice precipitates that might cause haze. Gelatin, when used in doses of 1%-5% concentrations, aids the retention of natural fluids and improves texture and flavor.

Europe Animal Protein Market Trends

The growing consumption of animal protein fuels opportunities for key players in the ingredients category

- In the United Kingdom, from 2016 to 2019, the average daily protein intake of individuals aged 19-64 years was 76 g per person, which was more than the 64 g/day average adult daily requirement. This number was calculated using a reference intake value of 0.83 g/kg of body weight per day. The average daily consumption of animal protein per person is projected to be 39.6 g, with 25.9 g coming from meat and meat products and 9.9 g from milk and milk products. Accordingly, the total domestic milk production has risen. Less than 7% of the domestic production is exported, thereby providing easy access to manufacturers.

- The market for whey protein is mainly driven by the growing popularity of fitness centers and health clubs, leading to a rise in whey consumption. The annual whey protein import increased exponentially by 15.09% in 2021 from 2019. However, with a great focus on overall health and consumers' interest in clean-label products, the sports nutrition industry's demand for natural ingredients has been growing. Ingredients, such as organic and grass-fed whey, have gained prominence due to health and ethical concerns.

- Women seek sports nutrition supplements for lean body, strength, and performance. Encouragement from nutritionists and other fitness experts is also boosting the market sentiment for sports nutrition in the region. Growing veganism, demand for plant-based products, and changing dietary preferences among consumers are being witnessed globally. The low inclination toward meat-based products is visible among consumers, which is a major restraining factor for the animal protein market. The number of vegans in Europe doubled from 1.3 million to 2.6 million, representing 3.2% of the population in 2021.

Meat and milk production contributes majorly in terms of raw material for plant protein manufacturers

- The graph given depicts the production data for raw materials such as meat of cattle, pigs, and chicken (with bone, fresh or chilled), raw milk from cattle and goats, skim milk from cows, and dry whey powder. Germany is the leading producer of milk in the European Union, accounting for more than 21% of milk deliveries in the European Union in 2020. Although the country has been observing a decline in the count of cattle farms, the average size of the farms is witnessing an upsurge. The rise in milk production is attributed to the escalated volume of milk production per cow. Over the years, milk production has been concentrated in the grassland regions of northwestern and southern Germany.

- Milk production is constantly rising in the United Kingdom despite the continuous decline in the number of dairy cows. As of December 2022, the total number of dairy cows in the United Kingdom that were greater than 12 months old stood at 2.66 million heads. In the same year, milk production per cow amounted to 8,169 liters per annum, an increase of 3.5% compared to 7,893 liters in 2017.

- In 2020, there were over 76 million cattle in the European Union (EU), and beef production reached 6.8 million tonnes, making the European Union the world's third-largest producer after the United States and Brazil. The sector is diverse in terms of herd size, farm structure, and geographical distribution of farms in the European Union. Three EU member states alone produce half of the EU's beef: France (21.2%), Germany (17.8%), and Italy (11.1%).

Europe Animal Protein Industry Overview

The Europe Animal Protein Market is moderately consolidated, with the top five companies occupying 40.63%. The major players in this market are Agrial Enterprise, Arla Foods amba, Darling Ingredients Inc., Koninklijke FrieslandCampina NV and SAS Gelatines Weishardt (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 France

- 3.4.2 Germany

- 3.4.3 Italy

- 3.4.4 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Belgium

- 4.3.2 France

- 4.3.3 Germany

- 4.3.4 Italy

- 4.3.5 Netherlands

- 4.3.6 Russia

- 4.3.7 Spain

- 4.3.8 Turkey

- 4.3.9 United Kingdom

- 4.3.10 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Arla Foods amba

- 5.4.3 Darling Ingredients Inc.

- 5.4.4 Groupe LACTALIS

- 5.4.5 Koninklijke FrieslandCampina NV

- 5.4.6 Lactoprot Deutschland GmbH

- 5.4.7 LAITA

- 5.4.8 SAS Gelatines Weishardt

- 5.4.9 Ynsect

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms