アジア太平洋地域のペット用おやつ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Pet Treats - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 261 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690764

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

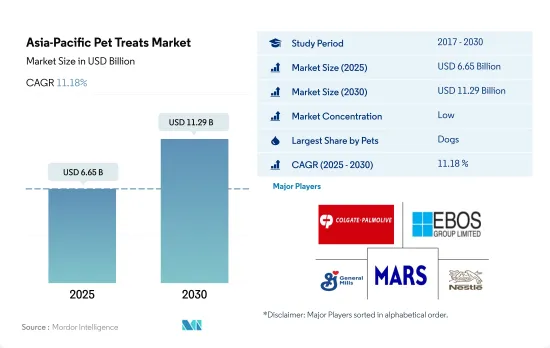

アジア太平洋地域のペット用おやつの市場規模は、2025年に66億5,000万米ドルと推定され、予測期間中(2025-2030年)にCAGR 11.18%で成長し、2030年には112億9,000万米ドルに達すると予測されます。

主なペットは犬であったが、同地域での浸透が進んでいるため、猫が最も急速に成長している

- アジア太平洋地域のペット用おやつ市場は、2017年の4億4,220万人から2022年には5億1,110万人に増加したペット数の増加を主な要因として、著しい成長を遂げています。ペットの人間化の動向の高まりは、高品質のペット用おやつへの需要の増加をもたらし、市場の成長に寄与しました。

- ペットの中では犬がアジア太平洋のペット用おやつ市場を独占し、2022年の市場金額の51.4%を占める。同年の市場規模は27億4,000万米ドルでした。犬のシェアが高いのは、同地域のペット数の34.49%を占める犬の飼育数が、他のペットに比べて多いためです。他のペットに比べ、犬のおやつに対する嗜好性が高いこともシェア上昇に寄与しています。

- 猫市場は、同地域における猫の飼育数が多いことから、2022年には31.8%を占め、第2位の市場セグメントとなっています。同年、猫の飼育数はペット数の26.1%を占めました。同地域では猫の飼育数が増加しており、犬と比較して狭い居住空間への適応性が高いことから、猫用おやつ市場は予測期間中にCAGR 12.4%を記録し、最も急成長するセグメントとして牽引役となることが予想されます。

- その他のペット用おやつ市場は、2022年に8億9,540万米ドルの規模に達しました。犬や猫に比べて比較的メンテナンスが簡単であることから、ペットとしてのその他の動物への関心が高まっており、これが市場を牽引すると予想されます。

- この地域におけるペット数の増加は、予測期間中に市場を牽引すると予想される主な要因です。

アジア太平洋地域のペット用おやつ市場を牽引しているのは、高品質でプレミアムなペット用おやつに対するペットの親たちの購買意欲の高まりです。

- ペット用おやつは、アジア太平洋地域のペットフード市場で最も急成長している市場セグメントです。2022年、ペット用おやつ市場はアジア太平洋地域のペットフード市場の18.2%を占め、53億3,000万米ドルとなりました。ペットの飼育率の増加と高品質で健康的なおやつに対する意識の高まりに伴い、2022年の市場は2017年比で70.2%成長しました。

- 2022年のアジア太平洋ペット用おやつ市場では、中国が25億8,000万米ドルを占め、最大国でした。同国のシェアが高いのは、ペット数が多いことに加え、飼い主のペット用おやつへの支出が多いためです。例えば、中国のペット数は2022年にアジア太平洋のペット数の54%を占めました。さらに、中国のペットオーナーは、ペット1匹当たり平均約509米ドルをペット支出に費やしています。

- 日本とオーストラリアは、この地域で2番目と3番目に大きいペット用おやつ市場で、それぞれ5億3,640万米ドルと4億3,640万米ドルと評価されています。ペットの親がプレミアム製品を購入し、オーダーメイド製品に対する需要が高まっていることが、これらの国々で高い市場需要を生み出しています。

- フィリピンは、ペット数の増加と2017年から2022年の間にペット支出が約20.9%増加し続けることから、2023年から2029年の間にCAGRが20.1%となり、地域市場で最も急成長する国になると予測されています。

- タイ、インド、台湾は、2022年に合わせて5億6,500万米ドルと評価される地域市場の他の重要な国です。ペット用おやつの需要は、ペット支出の増加に伴い、これらの国々で今後数年間増加すると推定されます。

- ペット数の増加、プレミアムフードへの需要の高まり、健康への懸念に対する意識の高まりといった要因が、2023年から2029年にかけてのおやつ市場の成長を後押しすると予想されます。

アジア太平洋のペット用おやつ市場動向

動物の世話を支援し、多種多様なキャットフード製品やサービスを提供するペットカフェやペットショップのエコシステムの発展が、猫の飼育数を増加させています。

- アジア太平洋では、猫は犬よりもシェアが低く、2022年にはペット数の26.1%を占める。中国、インド、オーストラリアなどの国々では、リラックスしてストレスを感じにくくなる、交友関係が広がるなどの健康上の利点から、ペットの飼育が増加しています。そのため、猫の飼育数は2017年から2022年にかけて0.28%増加しました。インドネシアとマレーシアでは、2021年にはそれぞれ47%と34%を占め、犬の親よりも猫の親のシェアが高いです。これらの国の宗教文化や、犬よりも猫をペットとして好む傾向が、猫の飼育数を増加させました。この動向は、企業がこれらの国々でキャットフードにより多く投資するのに役立つと思われます。

- 中国では、都市部において猫を含むペットの数が増加しており、猫を含むペット数は2018年から2020年の間に10.2%増加し、2020年には1億80万人に達しました。猫の飼育数は、パンデミック時の同伴ニーズの高まりにより、2020年の7,440万匹から2022年には8,250万匹に増加しました。猫の寿命は20年以上であるため、この動向は長期的な影響を及ぼす可能性があります。

- この地域では、多種多様なペットフード製品やサービスを通じて動物の購入や世話を支援するペットカフェやペットショップという形で、ペットの採用と購入に関する新たなエコシステムが発展しつつあります。例えばベトナムでは、R HouseのMeow Houseがベジタリアンやビーガン向けの食事を提供する猫カフェであり、猫の家として機能しています。健康上の利点による猫の採用の増加、この地域の文化、ペット生態系の変化などの要因が、この地域での猫の採用を後押ししています。

グレインフリーやナチュラル製品など高級ペット用おやつへの需要の高まりがペットの支出を押し上げる

- アジア太平洋地域では、さまざまな種類のペットフードが入手可能になったことと、ペットの親がプレミアム価格を喜んで支払うような良質なペットフードを好むようになったことから、ペットへの支出が増加しています。従来、ペットの親は犬を飼うことが多かったが、近年は猫の飼育頭数が増加しています。しかし、2022年の支出に占める犬の割合は45.4%と高いです。この高いシェアは、高品質のペットフードの消費量の増加と、犬用にカスタマイズされたおやつの需要の高さによるものです。オーストラリアでは犬の人気が最も高く、2022年には約40%の世帯が犬を飼っており、これがペット用おやつの需要を増加させました。

- 中国、インド、韓国はこの地域の主要なペット市場であり、ペット支出はさらに伸びています。これらの国々では、特にパンデミックの後、ペットの親がペットの栄養要件をより意識するようになったため、ペットの飼育数が多く、良質でプレミアムなペットフードの消費量が多くなりました。例えば、香港のキャットフード市場では、2022年にプレミアム・ペットフード部門がペットフード売上高の75%を占めました。オンライン・ペットフードの売上は、特に中国で高いが、これはウェブサイトに膨大な数の商品が掲載され、注文が簡単なためです。例えば、2022年の中国のオンライン・チャネルによるペットフード売上高は58.9%であるのに対し、オフラインのペットショップの寄与率は27.5%です。

- ペットフードに対する需要の高まりと良質なペットフードに対する意識の高まりにより、予測期間中、同地域のペット支出は増加すると予想されます。

アジア太平洋ペット用おやつ産業概要

アジア太平洋のペット用おやつ市場は断片化されており、上位5社で15.71%を占めています。この市場の主要企業は以下の通り。 Colgate-Palmolive Company(Hill's Pet Nutrition Inc.), EBOS Group Limited, General Mills Inc., Mars Incorporated and Nestle(Purina)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- クランキートリート

- デンタルトリート

- フリーズドライとジャーキートリート

- ソフトおよびチューイートリート

- その他のおやつ

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Affinity Petcare SA

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- EBOS Group Limited

- General Mills Inc.

- IB Group(Drools Pet Food Pvt. Ltd.)

- Mars Incorporated

- Nestle(Purina)

- Vafo Praha, s.r.o.

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Asia-Pacific Pet Treats Market size is estimated at 6.65 billion USD in 2025, and is expected to reach 11.29 billion USD by 2030, growing at a CAGR of 11.18% during the forecast period (2025-2030).

Dogs were the major pets, but cats are the fastest growing due to their growing adoption in the region

- The Asia-Pacific pet treats market is witnessing significant growth, primarily driven by the increasing pet population, which rose from 442.2 million in 2017 to 511.1 million in 2022. The growing trend of pet humanization resulted in increased demand for high-quality pet treats, which contributed to the market's growth.

- Among pets, dogs dominate the Asia-Pacific pet treats market, accounting for 51.4% of the market value in 2022. They were valued at USD 2.74 billion in the same year. The higher share of dogs can be attributed to the larger population of dogs compared to other pets in the region, accounting for 34.49% of the pet population in the same year. The higher preference of dogs for treats compared to other pets contributed to their higher share.

- The cats segment is the second-largest market segment, accounting for 31.8% in 2022, due to their significant population in the region. The cat population accounted for 26.1% of the pet population in the same year. The growing population of cats in the region and their adaptability to small living spaces compared to dogs are expected to drive the cat treats market as the fastest-growing segment, with a CAGR of 12.4% during the forecast period.

- The treats market for other pets reached a value of USD 895.4 million in 2022. There is a growing interest in other animals as pets due to their relatively lower maintenance compared to dogs and cats, which is anticipated to drive their market.

- The increasing pet population in the region is the major factor anticipated to drive the market during the forecast period.

Increased willingness of pet parents to spend on high-quality premium pet treats has driven the Asia-Pacific pet treats market

- Pet treats are the fastest-growing market segment in the Asia-Pacific pet food market. In 2022, the pet treats market accounted for 18.2% of the pet food market in Asia-Pacific, valued at USD 5.33 billion. The market grew by 70.2% in 2022 compared to 2017, in line with increasing pet adoption rates and growing awareness about high-quality healthy treats.

- In 2022, China was the largest country in the Asia-Pacific pet treats market, accounting for USD 2.58 billion in 2022. The higher share of the country was because of its higher pet population, along with the higher expenditure of pet owners on pet treats. For instance, the pet population in China accounted for 54% of the Asia-Pacific pet population in 2022. Additionally, Chinese pet owners spend an average of around USD 509 per pet on pet expenditure.

- Japan and Australia are the second and third-largest pet treat markets in the region, valued at USD 536.4 million and USD 436.4 million, respectively. Pet parents purchasing premium products and increasing demand for custom-made products have created high market demand in these countries.

- The Philippines is projected to be the fastest-growing country in the regional market, with a CAGR of 20.1% during 2023-2029, owing to the growing pet population and the continued rise in pet expenditures by around 20.9% between 2017 and 2022.

- Thailand, India, and Taiwan are the other significant countries in the regional market, together valued at USD 565 million in 2022. The demand for pet treats is estimated to increase in these countries over the coming years, with increasing pet expenditures.

- Factors such as the rising pet population, growing demand for premium foods, and growing awareness about health concerns are anticipated to help the growth of the treats market during 2023-2029.

Asia-Pacific Pet Treats Market Trends

The evolving ecosystem of pet cafes and pet stores that assist in taking care of the animals and offer a wide variety of cat food products and services is driving the population of cats

- In Asia-Pacific, cats have a lower share compared to dogs, accounting for 26.1% of the pet population in 2022. Countries such as China, India, and Australia witnessed an increase in pet ownership due to health benefits such as feeling relaxed and less stressed and companionship. Therefore, the cat population grew by 0.28% between 2017 and 2022. The shares of cat parents are higher than dog parents in Indonesia and Malaysia, accounting for 47% and 34%, respectively, in 2021. The religious cultures of these countries and the preference for cats as pets over dogs drove the cat population. This trend may help the companies invest more in cat food in these countries.

- In China, there has been an increase in the no. of pets, including cats, in urban areas, and the pet population, including cats, grew by 10.2% between 2018-2020, reaching 100.8 million in 2020. The cat population grew from 74.4 million in 2020 to 82.5 million in 2022 due to a rise in the need for companionship during the pandemic. This trend may have long-term effects as the life span of cats is more than 20 years.

- A new pet adoption and purchase ecosystem is evolving in the region in the form of pet cafes and pet stores that assist in purchasing and taking care of animals through a wide variety of pet food products and services. For instance, in Vietnam, the Meow House by R House is a cat cafe that serves vegetarian and vegan food and serves as a home for cats. Factors such as the rising adoption of cats due to health benefits, the region's culture, and changes in the pet ecosystem are helping boost cat adoption in the region.

Increased demand for premium pet treats such as grain-free and natural products is boosting pet expenditure

- In Asia-Pacific, there has been a rise in pet expenditure because of the availability of different types of pet food and pet parents' preference for good quality pet food as they are willing to pay premium prices. Traditionally, pet parents had a higher number of pet dogs, but there has been an increase in the cat population in recent years. However, pet dogs had a higher share of expenditure in 2022, i.e., 45.4%. This high share was due to higher consumption of high-quality pet food and a high demand for customized treats for dogs. Dogs are most popular in Australia, and about 40% of households had a pet dog in 2022, which increased the demand for pet treats.

- China, India, and South Korea are the major pet markets in the region, further registering growth in pet expenditure. These countries witnessed a high number of pet adoptions and high consumption of good quality, premium pet food, especially after the pandemic, as pet parents became more aware of the nutritional requirements of their pets. For instance, in Hong Kong's cat food market, the premium pet food segment accounted for 75% of the pet food sales in 2022. Online pet food sales are high, especially in China, due to the vast number of products on the websites and the ease of placing orders. For instance, in 2022, China's pet food sales from online channels were 58.9% compared to the offline pet stores' contribution of 27.5%.

- The rising demand for pet food and growing awareness about good quality pet food are expected to increase pet expenditure in the region during the forecast period.

Asia-Pacific Pet Treats Industry Overview

The Asia-Pacific Pet Treats Market is fragmented, with the top five companies occupying 15.71%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), EBOS Group Limited, General Mills Inc., Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Crunchy Treats

- 5.1.2 Dental Treats

- 5.1.3 Freeze-dried and Jerky Treats

- 5.1.4 Soft & Chewy Treats

- 5.1.5 Other Treats

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Malaysia

- 5.4.7 Philippines

- 5.4.8 Taiwan

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 EBOS Group Limited

- 6.4.6 General Mills Inc.

- 6.4.7 IB Group (Drools Pet Food Pvt. Ltd.)

- 6.4.8 Mars Incorporated

- 6.4.9 Nestle (Purina)

- 6.4.10 Vafo Praha, s.r.o.

- 6.4.11 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 261 Pages

- 納期

- 2~3営業日