北米のペット用おやつ:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Pet Treats - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 228 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693979

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

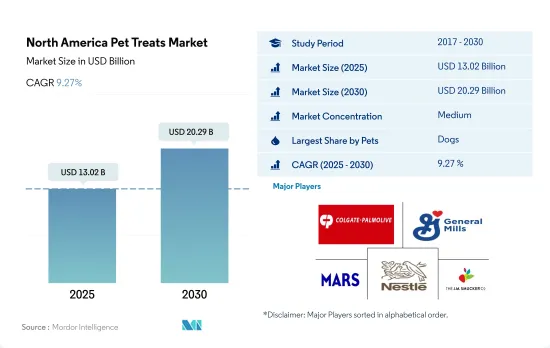

北米のペット用おやつ市場規模は2025年に130億2,000万米ドルと推定され、2030年には202億9,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは9.27%で成長する見込みです。

高級ペット用おやつの需要増加が市場を牽引

- 北米のペット用おやつ市場を独占しているのは犬であり、2022年の市場金額の約54.7%を犬が占めています。これは、2022年の同地域のペット数全体に占める犬の割合が約41.7%と大きいことに起因しています。さらに、同地域ではプレミアム犬用おやつ製品に対する傾向が高まっており、犬用ペットおやつ市場は予測期間中にCAGR 10.6%を記録すると予測されています。

- 2022年には、猫は北米のペット用おやつ市場で2番目に大きな市場シェアを占め、市場金額の約25.0%を占めます。しかし、これは犬よりも比較的低く、その主要理由は猫の飼育数が少ないためです。北米における猫のペット数は、2022年には犬のペット数より49.3%少なかりました。

- 同地域のペット総飼育数の約30.4%を占めているにもかかわらず、鳥、魚、げっ歯類などのその他のペット動物は、2022年の市場総額の20.3%を占めるに過ぎなかりました。これは、これらのペットが一般的にサイズが小さく、比較的少量の餌しか必要としないことが主要理由です。

- 歯科用おやつは犬が最も消費するおやつであり、2022年の犬によるペット用おやつ消費額の約25.6%を占めています。このように歯科用おやつが圧倒的に多いのは、他のペット動物に比べて犬の歯の問題が多いことが主要理由です。これらのデンタルおやつは、予測期間中にCAGR 11.2%を記録すると予測されています。フリーズドライとジャーキーのおやつは、猫が消費する最も人気のあるおやつであり、2022年の猫のペット用おやつ市場額の約24.9%を占めています。

- ペットの人間化傾向の高まりが予測期間中の市場を牽引すると予想されます。

米国は、ペットの人間化とプレミアム化が進んでいるため、この地域で最大のペット用おやつ市場です。

- 北米のペット用おやつ市場は、ペットフード市場の重要かつ拡大中のサブ市場です。2022年、ペット用おやつ市場は北米のペットフード市場の14%を占め、2017年と比較して64%成長しました。このような成長が観察されたのは、主に同地域でペットの飼い主が増加したためです。例えば、2022年、同地域のペット数は3億4,560万人と記録され、これは2017年に比べて12%増加しました。この地域では犬が最も人気のあるペットであり、2022年のペット用おやつ市場で42%と最大の市場シェアを占め、次いで猫が28%でした。

- 2022年の米国市場規模は87億4,000万米ドル、次いでカナダが8億1,020万米ドル、メキシコが5億1,780万米ドルでした。米国の市場シェアが高いのは、ペット数が多く、ペット用おやつ市場が確立しているためです。また、この地域で最も急成長している国でもあり、2023~2029年のCAGRは9.4%を記録すると予想されています。この地域では、カリカリおやつ、デンタルおやつ、フリーズドライおやつやジャーキーおやつが人気です。グレインフリーや新規タンパク質を使用したペット用おやつ、歯と口腔の健康のために特別に配合されたおやつ、その他のサプリメントが人気で、市場での需要が高いです。ペットの飼い主の多くは、環境にやさしくサステイナブルプレミアム製品に高いお金を払うことを望んでいます。

- 専門店が最も好まれる流通チャネルであり、この地域のペット用おやつの流通チャネル全体の37.7%を占めています。オンラインはこの地域で最も急成長しているチャネルであり、2023~2029年のCAGRは10.5%を記録すると推定されます。高品質のおやつに対する需要の増加、ペット用おやつのプレミアム化、eコマースの利用可能性により、この地域の市場は2023~2029年の間にCAGR 9.1%を記録すると推定されます。

北米のペット用おやつ市場動向

若年層やミレニアル世代による猫飼育の増加が成長を牽引

- 北米では、交友関係の需要が高く、他のペットに比べて猫のペットフードへの支出が少ないことから、猫がペットとして採用されています。さらに同地域では、ペットの人間化が進み、猫が生活するのに必要な面積が少ないことから、ペットとしての猫は2017~2022年の間に13.6%増加しました。例えば、米国では2020年に26%の世帯が猫をペットとして飼っていたが、カナダでは29.3%でした。

- 米国、カナダ、メキシコでは、パンデミック後にペットとしての猫の飼育率が上昇しました。リモートワークが刺激となってペットの飼育率が上昇し、ミレニアル世代に属する飼い主が増えたからです。例えば、2022年には、ミレニアル世代が米国におけるペットの親の33%を占め、2020年には、猫のペット数の40%が米国の動物保護施設から引き取られました。さらに、ペットの親は高収入のためペットショップから猫を購入し、2020年には米国の猫の親の43%がペットショップから猫を購入しています。したがって、北米におけるペットとしての猫は2020~2022年の間に5.34%増加しました。

- 米国では、ペットの親による成猫に比べ、幼猫の採用率が高いです。例えば、2021年の米国の猫の飼育数は約68万4,144頭で、若い猫が53.5%を占めています。若い猫の飼育数が増え、ミレニアル世代がペットの親になることで、予測期間中のペット用おやつの成長に貢献すると予想されます。

- 猫の養子縁組や購入の増加、ペットの人間化の進展といった要因がペット数の増加に寄与し、ペット数の増加が同地域のペットフード市場の成長に貢献すると予想されます。

自然でオーガニックなおやつへの需要が同地域のペット支出を増加させています。

- 北米では、ペットの支出が増加する傾向が見られます。ペットフードの支出が増加しているのは、さまざまな種類のペットフードが入手可能になり、米国とカナダでペットフード製品のプレミアム化が進んでいるためです。さらに、ペットの親はこの地域で、カスタマイズ型ペットフードや天然&オーガニックペットフードなどのプレミアムセグメントに出費しています。

- ペットの親たちの最も高い支出はペットフードであり、これは予測期間中に増加すると予測されます。例えば、米国では2022年にペットフードがペット費用の42.4%(1億3,680万米ドル)を占めました。最も高いシェアを占めており、ペットを家族の一員として扱う両親や、特殊なペットフードに対する意識の高まりから、今後も増加すると予測されています。犬のフード支出シェアは猫よりも高いが、これは犬の飼育数が多く、猫よりもフードの消費量が多いためです。ペットペアレントはペットを家族の一員と考え、高級ペットフードを与え、ペットグルーミングやペットデイケアなどのサービスを利用します。米国では、ペットの親の約40%がプレミアムペットフードを購入し、2022年にはペットのグルーミングや散歩などのサービスに114億米ドルが費やされました。

- ペットの親は、オンライン小売店、スーパーマーケット、ペットショップを通じてペットフードを購入します。ペットの親がeコマースサイトで膨大な数のペットフード製品を入手でき、パンデミックによってオンライン注文が増加したため、ペットフードの売上はオンライン小売業者経由の方が高いです。例えば米国では、フードを含むペットケア製品のオンライン販売は、2020年の32%から2022年には40%に増加しました。

- プレミアム化と高品質フードの利点に関する意識の高まりは、この地域におけるペット支出を増加させるのに役立っていると予測される要因です。

北米のペット用おやつ産業概要

北米のペット用おやつ市場は適度に統合されており、上位5社で59.58%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、The J. M. Smucker Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- カリカリおやつ

- デンタルトリーツ

- フリーズドライとジャーキートリーツ

- ソフト&チューイートリーツ

- その他のおやつ

- ペット

- 猫

- 犬

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Affinity Petcare SA

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Sunshine Mills Inc.

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The North America Pet Treats Market size is estimated at 13.02 billion USD in 2025, and is expected to reach 20.29 billion USD by 2030, growing at a CAGR of 9.27% during the forecast period (2025-2030).

Increased demand for premium pet treats is driving the market

- Dogs dominated the North American pet treats market, and dogs accounted for about 54.7% of the market value in 2022. This can be attributed to the fact that dogs comprise a significant proportion, around 41.7% of the overall pet population in the region in 2022. Furthermore, there is a growing trend toward premium dog treat products in the region, and the dog pet treats market is anticipated to register a CAGR of 10.6% during the forecast period.

- In 2022, cats represented the second-largest market share in the North American pet treats market, accounting for about 25.0% of the market value. However, this is comparatively lower than dogs, primarily due to their lower population. The number of pet cats in North America was 49.3% less than the number of pet dogs in 2022.

- Despite accounting for around 30.4% of the total pet population in the region, other pet animals, such as birds, fish, and rodents, only represented 20.3% of the total market value in 2022. This was largely because these pets are generally small in size and require relatively small amounts of food.

- Dental treats are the most consumed treats by dogs, and they accounted for about 25.6% of the pet treats consumption value by dogs in 2022. This domination of dental treats is mainly because dental issues are more common in dogs compared to other pet animals. These dental treats are anticipated to register a CAGR of 11.2% during the forecast period. Freeze-dried and jerky treats are the most popular treats consumed by cats, and they accounted for about 24.9% of the pet treats market value in cats in 2022.

- The increasing trend of pet humanization is anticipated to drive the market during the forecast period.

The United States is the largest pet treats market in the region due to the growing pet humanization and premiumization in the country

- The North American pet treats market is a significant and expanding sub-market of the pet food market. In 2022, the pet treats market accounted for 14% of the pet food market in North America, growing by 64% compared to 2017. This observed growth was primarily due to the increasing number of pet owners in the region. For instance, in 2022, the pet population in the region was recorded at 345.6 million, which was 12% more than in 2017. Dogs are the most popular pets in the region, accounting for the largest market share in the pet treats market at 42% in 2022, followed by cats at 28%.

- In 2022, the US market was valued at USD 8.74 billion, followed by Canada at USD 810.2 million and Mexico at 517.8 million. The United States' high market share is due to its large pet population and well-established pet treats market. It is also the fastest-growing country in the region, and it is expected to register a CAGR of 9.4% during 2023-2029. Crunchy treats, dental treats, and freeze-dried and jerky treats are popular in the region. Pet treats made with grain-free and novel proteins, specifically formulated for dental and oral health, and other supplements are popular and have a high demand in the market. Many pet owners are willing to pay more for premium products that are eco-friendly and sustainable.

- Specialty stores are the most preferred distribution channel, accounting for 37.7% of the total distribution channels for pet treats in the region. Online is the fastest-growing channel in the region, and it is estimated to record a CAGR of 10.5% during 2023-2029. With the increasing demand for high-quality treats, premiumization of pet treats, and e-commerce availability, the regional market is estimated to record a CAGR of 9.1% during 2023-2029.

North America Pet Treats Market Trends

Increased adoption of cats by younger adults and millennials in the region is driving the growth

- Cats have been adopted as pets in North America due to the high demand for companionship and less expenditure on pet food for cats compared to other pets. Moreover, in the region, cats as pets increased by 13.6% between 2017 and 2022 due to a rise in pet humanization, and cats require less area to live. For instance, in the United States, in 2020, 26% of households owned a cat as a pet, whereas, in Canada, it was 29.3%.

- The United States, Canada, and Mexico have witnessed higher adoption of cats as pets after the pandemic because there is an increase in pet ownership stimulated by remote work, and more pet owners belong to the millennial generation. For instance, in 2022, millennials accounted for 33% of pet parents in the United States, and in 2020, 40% of the cat pet population was adopted from animal shelters in the United States. Additionally, pet parents purchased cats from pet stores due to high income, and in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in North America increased by 5.34% between 2020 and 2022.

- There is a higher adoption of young cats in the United States as compared to adult cats by pet parents. For instance, in 2021, the adopted cat population in the United States was about 684,144, and young cats accounted for 53.5% of the cats adopted in the country. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet treats during the forecast period.

- Factors such as an increase in the adoption and purchase of cats and an increase in pet humanization are expected to help the growth of the pet population, and the rise of the pet population will help in the growth of the pet food market in the region.

Demand for natural and organic treats is increasing the pet expenditure in the region

- A trend of increase in pet expenditure is witnessed in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. Moreover, pet parents are spending on premium segments, such as customized pet food and natural and organic pet food, in the region.

- Pet parents' highest expenses are on pet food, which is estimated to increase during the forecast period. For instance, pet food accounted for 42.4% of pet expenses in the United States (USD 136.8 million) in 2022. They have the highest share and are projected to increase due to pet parents treating their pets as family members and increased awareness about specialized pet food. The dog's food expenditure share is higher than that of cats because the dog population is higher, and they consume a larger quantity of food than cats. Pet Parents provide premium pet food to their pets and use services, such as pet grooming and pet daycare, in the region as they consider them as family members. In the United States, about 40% of pet parents purchased premium pet food, and USD 11.4 billion was spent on services, such as pet grooming and pet walking, in 2022.

- Pet parents purchase pet food through online retailers, supermarkets, and pet stores. Higher Pet food sales are through online retailers as pet parents have a vast number of pet food products available on e-commerce sites, and the pandemic increased online orders. For instance, in the United States, online sales of pet care products, including food, increased from 32% in 2020 to 40% in 2022.

- Premiumization and rising awareness about the benefits of quality food are factors anticipated to have helped in increasing pet expenditure in the region.

North America Pet Treats Industry Overview

The North America Pet Treats Market is moderately consolidated, with the top five companies occupying 59.58%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Crunchy Treats

- 5.1.2 Dental Treats

- 5.1.3 Freeze-dried and Jerky Treats

- 5.1.4 Soft & Chewy Treats

- 5.1.5 Other Treats

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 Sunshine Mills Inc.

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 228 Pages

- 納期

- 2~3営業日