|

市場調査レポート

商品コード

1694000

英国のペット用おやつ市場:市場シェア分析、産業動向、成長予測(2025~2030年)UK Pet Treats - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のペット用おやつ市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 197 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

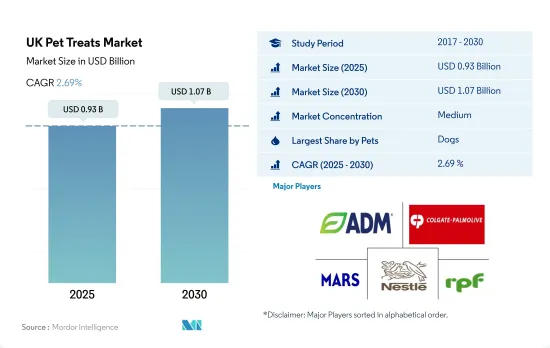

英国のペット用おやつ市場規模は2025年に9億3,000万米ドルと予測され、2030年には10億7,000万米ドルに達し、予測期間(2025~2030年)のCAGRは2.69%で成長すると予測されます。

犬がペット用おやつ市場を独占、猫が主要ペットとして台頭

- 英国のペット用おやつ市場は大きな成長を遂げており、その主要因は同国におけるペット数の増加であり、2017年の2,270万人から2022年には3,840万人に増加します。ペットの人間化の動向も市場成長に寄与しています。

- 英国のペット用おやつ市場は主に犬が占めており、2022年には犬用おやつ市場がペット市場の53.0%を占めます。これは、ペット数全体に占める犬の割合が大きく、同国では同年に約33.8%を占め、他のペット動物に比べて消費量が多いことに起因しています。犬のペット用おやつの市場規模は、予測期間中にCAGR 2.0%を記録すると予測されています。

- 英国のペット用おやつ市場では、猫が第2位のシェアを占め、2022年には金額ベースでペット用おやつ市場の約31.2%を占めました。同年、猫は同地域のペット総飼育数の約33.1%を占めたが、市場シェアは犬に比べ相対的に限定的でした。この格差は、猫が犬に比べおやつの消費量が少ない傾向にあり、ペット用おやつセグメントでの市場プレゼンスに影響を与えていることに起因しています。

- 国内のペット総飼育数の約33.1%を占めているにもかかわらず、鳥類、魚類、げっ歯類などのその他のペット動物は、2022年の市場総額の15.8%を占めるに過ぎなかりました。これは、これらのペットが一般的にサイズが小さく、必要な餌の量が比較的少ないことが主要理由です。

- 同国ではペット数が多く、おやつがペットにさまざまな健康上のメリットを提供できることから、予測期間中、市場の牽引役となることが予想されます。

英国のペット用おやつ市場動向

都市部では猫を飼う傾向が高まっています。

- 英国では過去5年間、ペットの猫の飼育が増加しており、同国におけるペットとしての猫の飼育数の増加は、COVID-19の大流行時の交友関係の必要性の増加、都市化の進展、猫が閉所感を感じることなく室内で飼育できることなどに起因すると考えられます。これらの利点により、猫の飼育数は2019~2022年の間に69.3%増加しました。

- 英国では、ペットとしての猫の飼育数が犬よりも多い地域は1つしかないです。2022年、ロンドンではペットを飼う人の61%を猫が占め、猫の所有率が国内で最も高いことが目の当たりにされました。ロンドンが猫を飼う割合が全国で最も高いのは、手頃な価格でメンテナンスの必要性が低いからです。狭いアパートや一軒家に住む人が増えており、犬よりも猫に適しています。国内で飼われている猫の大半は、都市部で暮らしていることがわかる。都市部で猫を飼う人が多いのは、犬よりも飼育スペースが少なくて済み、散歩の必要がないためで、ロンドンなどの賑やかな都市部では難しいです。猫は比較的おとなしい生き物なので、アパート暮らしには欠かせないです。

- 国内では猫の飼育数が増加する可能性が高く、国内の都市部では今後数年間で25万匹の野良猫がペットの親に飼われると予想されています。都市化の進展による猫の飼育数の増加、維持費の低減、将来的に猫の養子縁組が増加する可能性などが、同国のペットフード市場の成長に寄与すると予想されます。

ペットフード製品のプレミアム化の進展と高品質の天然ペットフードへの需要の高まりが、英国での支出を促進しています。

- 英国では、ペットの飼い主が様々なペット用品に支出する額が一貫して増加傾向にあります。2019~2022年の間に、ペット支出は約13.3%の大幅な増加がありました。この成長は、ペットの人間化の動向の高まりにより、自然食やグレインフリーのペットフードを含むプレミアム製品の需要が高まったことに起因すると考えられます。

- ペット用おやつ支出は、2022年の英国におけるペット1匹当たりの支出総額の約10.3%を占めました。2019~2022年にかけて、同国におけるペット用おやつの支出は増加しました。猫用おやつへの支出は約37.8%の大幅な増加を示し、犬用おやつへの支出は約11.7%、その他のペット動物用おやつへの支出は同期間に4.3%増加しました。英国の主要ペット用おやつメーカーには、マースインコーポレイテッド、ネスレ・ピュリナペットケア、ヒルズペット・ニュートリションなどがあります。同国ではプレミアム化が進んでおり、様々な新規タンパク質のペット用おやつとペットの健康増進が求められており、同国のペット用おやつ支出を牽引しています。

- ペットショップ、動物病院、スーパーマーケットといったオフラインの小売チャネルは、国内でペットフード製品を購入するための好ましい流通チャネルです。しかし、eコマースは、特にパンデミックのため、近年人気を博しています。ペッツ・アット・ホームは国内有数のペットフード小売業者で、452店舗以上を展開しています。高品質のペット用おやつの利点に対する意識の高まりと、ペット用おやつのプレミアム化の進行は、今後も同国のペット支出を促進すると予測されます。

英国のペット用おやつ産業概要

英国のペット用おやつ市場は適度に統合されており、上位5社で43.98%を占めています。この市場の主要企業は、ADM、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、Mars Incorporated、Nestle(Purina)、Real Pet Food Co.です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- カリカリおやつ

- デンタルトリーツ

- フリーズドライとジャーキートリーツ

- ソフト&チューイートリーツ

- その他のおやつ

- ペット

- 猫

- 犬

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Dechra Pharmaceuticals PLC

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Real Pet Food Co.

- Vafo Praha, s.r.o.

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001483

The UK Pet Treats Market size is estimated at 0.93 billion USD in 2025, and is expected to reach 1.07 billion USD by 2030, growing at a CAGR of 2.69% during the forecast period (2025-2030).

Dogs dominate the pet treats market, with cats emerging as major pets in the country

- The United Kingdom pet treats market is experiencing significant growth, which is mainly attributed to the growing pet population in the country, which increased from 22.7 million in 2017 to 38.4 million in 2022. The increasing trend of pet humanization also contributed to market growth.

- The UK pet treats market is primarily dominated by dogs, with the dog treats market accounting for 53.0% of the pet market in 2022. This can be attributed to the significant share of dogs in the overall pet population, accounting for around 33.8% in the country during the same year, and their ability to consume more quantities compared to other pet animals. The dog pet treats market value is projected to register a CAGR of 2.0% during the forecast period.

- In the UK pet treats market, cats held the second-largest share, accounting for about 31.2% of the pet treats market by value in 2022. Although cats made up around 33.1% of the total pet population in the region during the same year, their market share was relatively limited compared to dogs. This disparity is attributed to the fact that cats tend to consume fewer quantities of treats compared to dogs, influencing their market presence in the pet treats segment.

- Despite accounting for around 33.1% of the total pet population in the country, other pet animals, such as birds, fish, and rodents, only represented 15.8% of the total market value in 2022. This is largely because these pets are generally smaller in size and require relatively lesser amounts of food.

- The large population of pets in the country and the treats' ability to offer various health benefits to pets are anticipated to drive the market during the forecast period.

UK Pet Treats Market Trends

There is an increased preference of adopting cats in urban areas as they require less space and are easily affordable

- The adoption of pet cats has been increasing in the United Kingdom for the past five years, and the increase in the number of cats as pets in the country can be attributed to an increase in the need for companionship during the COVID-19 pandemic, increasing urbanization, and because cats can be kept indoors without feeling cooped up. These benefits helped the cat population increase by 69.3% between 2019 and 2022.

- In the United Kingdom, only one region has a higher population of cats as pets than dogs. In 2022, London witnessed that cat ownership was the highest in the country as it accounted for 61% of the pet parents in London. London has the highest national share of cats adopted because of their affordability and lower maintenance requirements. Increasingly, people are living in small apartments and houses, which are better suited for cats than for dogs. The majority of the cats adopted in the country are found to be living in urban areas. The preference of people adopting cats in urban areas is because they require less space than dogs and do not need to be taken on walks, which is difficult in busy cities such as London. Cats are relatively quiet creatures, which is essential while living in flats, making them a preferred choice for pet parents.

- There is a high potential for the growth of the cat population in the country, with 250,000 stray cats in the urban areas of the country expected to be adopted by pet parents in the coming years. The rising cat population due to increasing urbanization, lower maintenance, and the potential of adoption of cats increasing in the future are anticipated to help in the growth of the pet food market in the country.

The growing pet food product premiumization and increasing demand for high-quality natural pet foods are driving expenditure in the United Kingdom

- In the United Kingdom, there has been a consistent upward trend in pet owners' spending on various pet products. Between 2019 and 2022, there was a substantial increase of about 13.3% in pet expenditure. This growth can be attributed to the growing trend of pet humanization, which has resulted in a higher demand for premium products, including natural and grain-free pet foods.

- The pet treats expenditure accounted for about 10.3% of the total pet expenditure in the United Kingdom per pet in 2022. Between 2019 and 2022, there was an increase in pet treats expenditure in the country. The expenditure on cat treats showed a significant increase of about 37.8%, while spending on dog treats increased by about 11.7%, and spending on other pet animal treats increased by 4.3% during the same period. Some of the major pet treat manufacturers in the United Kingdom are Mars Incorporated, Nestle Purina Petcare, and Hill's Pet Nutrition. The increasing premiumization in the country demands various novel protein pet treats and increased pet health, driving the pet treat expenditure in the country.

- Offline retail channels such as pet shops, vet clinics, and supermarkets are the preferred distribution channels for purchasing pet food products in the country. However, e-commerce has gained popularity in recent years, particularly due to the pandemic. Pets at Home is one of the leading pet food retailers in the country and operates more than 452 stores. Growing awareness of the benefits of high-quality pet treats and the increasing premiumization of pet treats are projected to continue driving pet expenditure in the country.

UK Pet Treats Industry Overview

The UK Pet Treats Market is moderately consolidated, with the top five companies occupying 43.98%. The major players in this market are ADM, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle (Purina) and Real Pet Food Co. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Crunchy Treats

- 5.1.2 Dental Treats

- 5.1.3 Freeze-dried and Jerky Treats

- 5.1.4 Soft & Chewy Treats

- 5.1.5 Other Treats

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 Dechra Pharmaceuticals PLC

- 6.4.5 General Mills Inc.

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 Real Pet Food Co.

- 6.4.9 Vafo Praha, s.r.o.

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms