|

市場調査レポート

商品コード

1687076

南米の貨物・物流:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の貨物・物流:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 361 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

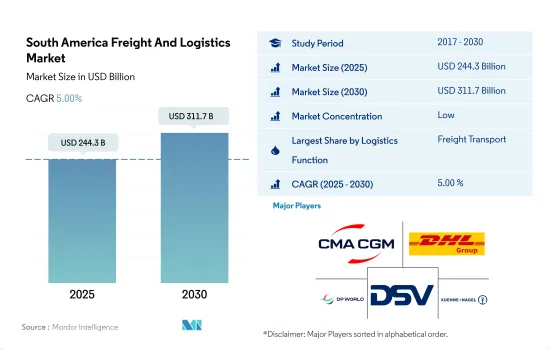

南米の貨物・物流市場規模は2025年に2,443億米ドルと推定され、2030年には3,117億米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.00%で成長します。

eコマース産業とインフラ投資、同地域の貨物輸送市場を開拓

- ブラジルは、2024~2026年にかけて、新規鉄道・高速道路プロジェクトに約1,800億BRL(340億3,000万米ドル)の民間投資を誘致する目標を掲げています。この動きは、ブラジルの道路インフラを近代化・拡大し、長距離トラック輸送能力を強化するための広範な取り組みの一環です。注目すべき動きとして、南北アメリカ開発銀行(IDB)はサンパウロ州高速道路投資プログラムに対し、2023年に4億8,000万米ドルの融資を承認しました。このイニシアチブは、同州の生産チェーンの強化、生産能力の向上、地域統合の促進を目的としています。ブラジルは、2026年までに620億米ドルの高速道路投資を確保することを目標としています。

- 南米におけるeコマースの急成長は、輸送サービスの需要に拍車をかけています。2023年には、この地域のeコマース部門の売上は583億8,000万米ドルに達し、2022年の517億9,000万米ドルから大幅に増加しました。予測によると、2023~2027年のCAGRは13.50%で、2027年までに収益は968億7,000万米ドルに達する見込みです。ユーザーベースも拡大し、2025年には2億4,410万人に達するとの基本推定があります。2022年のユーザー普及率は54.0%で、2025年には58.7%まで上昇すると予測されています。

南米の貨物・物流の成長と変遷

- ブラジルは、アルゼンチン、チリ、コロンビア、ペルーと並ぶこの地域の主要経済国のひとつです。ブラジルはサステイナブル輸送を目指し、トラック車両にクリーン技術を採用しています。例えば、Anheuser-Busch InBevが所有するブラジルの醸造会社Ambevは、電気トラックのサプライヤーであるFNMと協力し、2023年末までに約1,000台の電気トラックを導入しました。ブラジルは、鉱業における電気トラックの採用を示しました。例えば、2022年10月、Valeはミナス・ジェライス州のアグア・リンパで72トンのオフハイウェイ・トラックをテストすると発表しました。こうした重要な技術革新と、複数のセクターにわたる貨物輸送需要の増大。

- アルゼンチンでは、2023年9月にDHL Expressがマイアミとブエノスアイレスを結ぶ新たな貨物便を就航させ、配送効率の向上を図りました。このフライトはパナマのDHL Aero Expresoが管理し、52トンの積載能力を持つB767-300貨物機を使用します。運航は週6便で、マイアミ国際空港(MIA)からチリのサンティアゴ(SCL)を経由してブエノスアイレス(EZE)まで往復します。この取り組みにより、アルゼンチン到着当日の通関を10%スピードアップし、当日配送を50%増やすことを目指しています。

南米の貨物・物流市場の動向

南米諸国は輸送部門を改善するため、インフラ開発に多額の投資を行っています。

- 2024年6月、アルゼンチン連邦政府は914のインフラプロジェクトを州当局に移管し、州にとって厳しい財政上の課題が生じた。公共事業の再開を望んでいるにもかかわらず、州は主要収入源である連邦政府からの交付金の大幅削減に直面しています。州への連邦税移転額(CFI)は2024年6月に前年同月比20%減となり、2024年6ヶ月のうち5ヶ月で2桁減となりました。その他の連邦政府移転(RON)も6月に24.1%減少しました。

- 2023年、ブラジル政府は高速道路、鉄道、港湾、空港を含むインフラ物流に25億9,000万米ドルを割り当てました。その大部分、約24億2,000万米ドルが高速道路に投入され、鉄道は3,025万米ドルと控えめな配分でした。今後、政府は2024年6月までに、公共部門と民間部門の資金を組み合わせて、貨物鉄道プロジェクトへの投資を拡大することを目的とした大規模な国家イニシアチブを開始する予定です。野心的なビジョンに基づき、政府はこれらの鉄道プロジェクトに40億米ドルを投入する予定です。

ロシア・ウクライナ戦争が世界の原油価格に与えた影響により、この地域の原油価格は大幅に上昇しました。

- 2024年3月、季節変動と景気減速の兆候により、ブラジルのディーゼル需要が減少しました。ペトロブラスが軽油価格の引き下げを決定したことに加え、バイオディーゼル混合率を12%から14%に引き上げることが義務化されたことも、従来型の化石軽油の需要減少に拍車をかけた。国内市場は、世界の原油価格の変動と、それを安定させようとする政府の努力にも左右されました。手元に320万バレルのロシア産軽油が過剰にあったにもかかわらず、ブラジルは完全に出荷を停止することなく出荷を維持しました。

- チリは2030年までにサステイナブル航空燃料(SAF)の大規模生産を開始する計画で、2050年までに航空燃料需要の半分を油脂、生物学的と都市廃棄物由来のバイオ燃料で賄うことを目指しています。2040年までに航空交通量が倍増すると予測される中、チリはSAFを脱炭素化戦略における極めて重要な要素と考えています。さらに、SAFは従来のジェット燃料と混合することで、エンジンを改造することなく排出ガスを最大80%削減することができます。SAFはチリが目標とする炭素排出削減量の半分以上に貢献し、同国のネットゼロ目標において重要な役割を果たすと期待されています。

南米の貨物・物流産業概要

南米の貨物・物流市場は細分化されており、CMA CGM Group(CEVA Logisticsを含む)、DHL Group、DP World、DSV A/S(De Sammensluttede Vognmaend af Air and Sea)、Kuehne+Nagel(アルファベット順)が主要5社となっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- トラック輸送コスト

- タイプ別トラック保有台数

- 物流実績

- 主要トラックサプライヤー

- モーダルシェア

- 海上貨物輸送能力

- 定期船の接続性

- 寄港地とパフォーマンス

- 運賃動向

- 貨物トン数の動向

- インフラ

- 規制の枠組み(道路と鉄道)

- アルゼンチン

- ブラジル

- チリ

- 規制の枠組み(海上・航空)

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 物流機能

- クーリエ、エクスプレス、小包(CEP)

- 仕向地別

- 国内

- 国際

- 貨物輸送

- 輸送モード別

- 航空

- 海上・内水道

- その他

- 貨物輸送

- 輸送手段別

- 航空

- パイプライン

- 鉄道

- 道路

- 海上・内陸水路

- 倉庫保管

- 温度管理

- 温度管理なし

- 温度管理

- その他

- クーリエ、エクスプレス、小包(CEP)

- 国名

- アルゼンチン

- ブラジル

- チリ

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Agunsa

- Alonso Group

- Americold

- CMA CGM Group(CEVA Logisticsを含む)

- Deutsche Bahn AG(DB Schenkerを含む)

- DHL Group

- DP World

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Kuehne+Nagel

- Romeu

- SAAM

- TASA Logistica

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

- 為替レート

目次

Product Code: 54644

The South America Freight And Logistics Market size is estimated at 244.3 billion USD in 2025, and is expected to reach 311.7 billion USD by 2030, growing at a CAGR of 5.00% during the forecast period (2025-2030).

E-commerce industry and infrastructure investments, developing the freight transport market in the region

- Brazil has set a target of attracting around BRL 180 billion (USD 34.03 billion) in private investments for new rail and highway projects from 2024 to 2026. This move is part of Brazil's broader efforts to modernize and expand its road infrastructure, which would bolster its long-haul trucking capabilities. In a notable development, the Inter-American Development Bank (IDB) sanctioned a USD 480 million loan in 2023 for the State of Sao Paulo Highway Investment Program. The initiative aims to enhance the state's production chains, improve production capacity, and foster regional integration. Brazil has set its sights on securing USD 62 billion in highway investments by 2026.

- The rapid growth of e-commerce in South America is fueling the demand for transportation services. In 2023, the region's e-commerce sector generated revenues of USD 58.38 billion, marking a significant increase from USD 51.79 billion in 2022. Projections indicate a CAGR of 13.50% from 2023 to 2027, with revenues expected to reach USD 96.87 billion by 2027. The user base is also set to expand, with estimates pegging it at 244.1 million by 2025. In 2022, the user penetration rate stood at 54.0%, and it is projected to rise to 58.7% by 2025.

Growth and transition in South America's freight and logistics

- Brazil is one of the major economies in the region, along with Argentina, Chile, Colombia, and Peru. Brazil is working toward sustainable transport and adopting clean technologies for truck fleets. For instance, Ambev, a Brazilian brewing company owned by Anheuser-Busch InBev, collaborated with electric truck supplier FNM to receive around 1,000 electric trucks by the end of 2023. Brazil witnessed the adoption of electric trucks in mining. For instance, in October 2022, Vale announced testing 72-tonne off-highway trucks at Agua Limpa in Minas Gerais. These significant technological innovations and growing demand for freight transport across several sectors.

- In Argentina, in September 2023, DHL Express launched new freighter flights between Miami and Buenos Aires to improve delivery efficiency. These flights, managed by DHL Aero Expreso in Panama, use a B767-300 freighter with a 52-ton capacity. Operating six times weekly, the service goes from Miami International Airport (MIA) to Buenos Aires (EZE) via Santiago, Chile (SCL), and back. This initiative aims to speed up customs clearance in Argentina by 10% on the same day as arrival and increase same-day deliveries by 50%.

South America Freight And Logistics Market Trends

South American countries are investing heavily in infrastructure development to improve the transportation sector

- In June 2024, Argentina's federal government transferred 914 infrastructure projects to provincial authorities, creating a tough financial challenge for the provinces. Despite wanting to resume public works, provinces have faced deep cuts to federal transfers, their main source of income. Federal tax transfers (CFI) to provinces dropped 20% YoY in June 2024 and have decreased by double digits in five out of the six months of 2024. Other federal transfers (RON) also fell 24.1% in June.

- In 2023, the Brazilian government allocated USD 2.59 billion to infrastructure logistics, encompassing highways, railways, ports, and airports. A significant portion, approximately USD 2.42 billion, was funneled into highways, while railways received a modest allocation of USD 30.25 million. Looking ahead, by June 2024, the government is set to launch a major national initiative aimed at amplifying investments in freight rail projects, leveraging a blend of public and private sector funding. With an ambitious vision, the government plans to inject a substantial USD 4 billion into these rail projects.

Crude oil prices in the region rose significantly owing to the impact of the Russia-Ukraine War on global crude oil

- In March 2024, seasonal fluctuations and signs of an economic slowdown led to a decline in Diesel demand in Brazil. Petrobras' decision to reduce Diesel prices, coupled with the mandated increase in biodiesel blending from 12% to 14%, further fueled this drop in demand for conventional fossil Diesel. The domestic market was also swayed by global fluctuations in crude oil prices and government efforts to stabilize them. Even with an excess of 3.2 million barrels of Russian Diesel on hand, Brazil maintained its shipments without a complete halt.

- By 2030, Chile plans to launch large-scale production of sustainable aviation fuel (SAF) and aims for these biofuel sources derived from oils, fats, and both biological and municipal waste to satisfy half of its aviation fuel needs by 2050. With projections of air traffic doubling by 2040, Chile views SAF as a pivotal element in its decarbonization strategy. Moreover, SAF can be blended with traditional jet fuel to reduce emissions by up to 80% without engine modifications. It is expected to contribute over half of Chile's targeted carbon emissions reductions, playing a key role in the country's net-zero goals.

South America Freight And Logistics Industry Overview

The South America Freight And Logistics Market is fragmented, with the major five players in this market being CMA CGM Group (including CEVA Logistics), DHL Group, DP World, DSV A/S (De Sammensluttede Vognmaend af Air and Sea) and Kuehne+Nagel (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Argentina

- 4.21.2 Brazil

- 4.21.3 Chile

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Argentina

- 4.22.2 Brazil

- 4.22.3 Chile

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agunsa

- 6.4.2 Alonso Group

- 6.4.3 Americold

- 6.4.4 CMA CGM Group (including CEVA Logistics)

- 6.4.5 Deutsche Bahn AG (including DB Schenker)

- 6.4.6 DHL Group

- 6.4.7 DP World

- 6.4.8 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.9 Kuehne+Nagel

- 6.4.10 Romeu

- 6.4.11 SAAM

- 6.4.12 TASA Logistica

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate