|

市場調査レポート

商品コード

1693572

ASEANの貨物・物流:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEANの貨物・物流:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 382 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

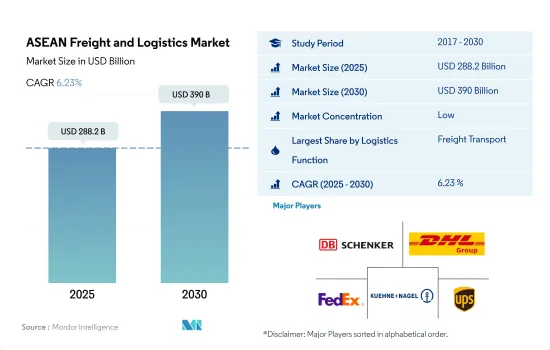

ASEANの貨物・物流市場規模は2025年に2,882億米ドルと推定され、2030年には3,900億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは6.23%で成長する見込みです。

物流セクタの発展につながるASEAN諸国のGDP貢献の増加

- マレーシアはクリーンエネルギーへの移行に注力しており、地元企業と政府系事業体の両方が技術進歩の先頭に立ってインフラ開発を推進しています。こうした取り組みは、屋上や浮体式太陽光発電、蓄電池、水素など、さまざまなセグメントに及んでいます。注目すべき例としては、2022年5月にマサマ社(Masama Sdn Bhd)がサラワク統合産業社(Sarawak Consolidated Industries Bhd、SCIB)に発注した3,800万リンギット(861万米ドル)の契約が挙げられます。エンジニアリング、調達、建設、試運転を含むこの契約は、マレーシアのサラワク州の複数の場所を結ぶ道路プロジェクトで、2023年3月に無事完了しました。

- 3,260kmの広大な海岸線と河川網を持つベトナムは、海上貨物輸送に大きな機会をもたらしています。ベトナム政府は野心的な目標を設定し、2030年までに同国を海洋先進国にすることを目指しています。この目標には、海事部門のGDP貢献度を10%に引き上げ、沿岸28都市・省の経済的重要性を高め、ベトナム全体のGDPに占める割合を65%から70%にすることが含まれています。

eコマース動向の高まりと政府による取り組みが市場成長を牽引

- ベトナム交通運輸省は、2025年までに南北高速道路の主要部分を含む14のインフラプロジェクトを着工し、さらに50のプロジェクトを完成させる計画です。これは、2025年までにベトナムの高速道路を現在の2,021kmから3,000kmに拡大するという目標の一環です。さらに、ドンナイ省の141億2,000万米ドルのプロジェクトであるロンタイン国際空港は、2025年の完成を目指しています。完成すれば国内最大の空港となり、ホーチミン市のタンソンニャットの混雑が緩和されます。

- 2023年11月、BBNインドネシア航空は3機目の貨物機を追加し、機体を拡大しました。アビアソリューションズ・グループの子会社であるACMIの航空会社は、Boeing737-400SFの購入を発表し、現在2機の737-800Fを増強しました。同機は2024年に商業運航を開始します。17,000の島々、5,150kmに及ぶインドネシアの広大な群島を考えると、航空輸送は極めて重要です。国際航空運送協会(IATA)は、2034年までにインドネシアは世界第6位の航空輸送市場になると予測しています。

ASEANの貨物・物流市場の動向

各国政府によるインフラ建設プロジェクトに支えられたASEAN諸国への直接投資の増加が経済成長を牽引

- 2024年5月、日本政府はインドネシアのジャカルタに高速鉄道を建設するため、約1,407億円(9億米ドル)の融資を発表しました。この東西鉄道プロジェクトは、総延長84.1kmで、2026~2031年までの2期に分けて完成します。この新しい鉄道路線には、列車や信号システムに日本の技術が採用されます。このような取り組みにより、運輸・倉庫部門からのGDP貢献が期待されます。

- 2024年2月、運輸省はタイのインフラを強化するため、2025年末までに約150の運輸プロジェクトに188億3,000万米ドルを投資する計画を発表しました。2024年には64のプロジェクトが開始され、さらに31のプロジェクト(112億3,000万米ドル相当)が進行中です。2025年には57の新規プロジェクトが計画されており、その総額は75億9,000万米ドルにのぼります。これらの構想には、18の高速道路プロジェクト、9の鉄道プロジェクト、地域港湾開発計画が含まれ、これらはすべて、将来の輸送・貯蔵部門のGDPへの貢献を強化することを目的としています。

イラン・イスラエル紛争とウクライナ・ロシア戦争のASEAN諸国への影響は、燃料価格の上昇とサプライチェーンの混乱につながりました。

- インドネシアは、シェルとシェブロンが最近撤退した後、掘削と探査を促進するため、2024年に石油・ガス部門への投資が29%増加すると予想しています。化石燃料プロジェクトに対する資金調達の課題が高まる中、インドネシアが長期的な生産量減少に対抗するためには、この推進が不可欠です。エニ、ExxonMobil、BPといった外資系企業は、2024年に予定されている投資の40%を拠出する予定です。また2024年初頭、石油・ガス省は、イラン・イスラエル紛争によって原油価格が1バレルあたり100米ドルまで上昇する可能性があるにもかかわらず、ガソリンスタンドの燃料価格は少なくとも2024年6月まで安定すると発表しました。

- マレーシアのディーゼル価格は、アンワル・イブラヒム首相が長年にわたる燃料補助金制度の改革に取り組みました一環として、2024年6月に50%以上急騰しました。この改革は、普遍的なエネルギー補助金を廃止し、援助を最も必要としている人々に集中させることで、国家財政の圧迫を緩和することを目的としていました。この動きはまた、補助金を受けた軽油が近隣諸国に密輸され、高値で取引されるといった問題に対処する狙いもあります。

ASEANの貨物・物流産業概要

ASEANの貨物・物流市場はセグメント化されており、この市場の主要企業はドイツ鉄道AG(DBシェンカーを含む)、DHLグループ、フェデックス、クーネ・ナゲル、ユナイテッド・パーセルサービスオブ・アメリカ(UPS)の5社です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- トラック輸送コスト

- タイプ別トラック保有台数

- 物流実績

- 主要トラックサプライヤー

- モーダルシェア

- 海上貨物輸送能力

- 定期船の接続性

- 寄港地とパフォーマンス

- 運賃動向

- 貨物トン数の動向

- インフラ

- 規制の枠組み(道路と鉄道)

- インドネシア

- マレーシア

- タイ

- ベトナム

- 規制の枠組み(海上・航空)

- インドネシア

- マレーシア

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 物流機能

- クーリエ、エクスプレス、小包(CEP)

- 仕向地別

- 国内

- 国際

- 貨物輸送

- 輸送モード別

- 航空

- 海上・内水道

- その他

- 貨物輸送

- 輸送手段別

- 航空

- パイプライン

- 鉄道

- 道路

- 海上・内陸水路

- 倉庫保管

- 温度管理

- 温度管理なし

- 温度管理

- その他

- クーリエ、エクスプレス、小包(CEP)

- 国名

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他のASEAN諸国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Alps Logistics

- Deutsche Bahn AG(DB Schenkerを含む)

- DHL Group

- DP World

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- FedEx

- JWD Group

- Kuehne+Nagel

- NYK(Nippon Yusen Kaisha)Line

- Tiong Nam Logistics Holdings Bhd

- United Parcel Service of America, Inc.(UPS)

- YCH Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(市場の促進要因、抑制要因、機会)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

- 為替レート

目次

Product Code: 92671

The ASEAN Freight and Logistics Market size is estimated at 288.2 billion USD in 2025, and is expected to reach 390 billion USD by 2030, growing at a CAGR of 6.23% during the forecast period (2025-2030).

Rising GDP contributions from ASEAN countries in the logistics sector leading to sector development

- Malaysia's focus on clean energy transition is driving its infrastructure development, with both local companies and government-owned entities spearheading technological advancements. These initiatives span various sectors, including rooftop and floating solar, battery storage, and hydrogen. A notable example is the RM 38 million (USD 8.61 million) contract awarded by Masama Sdn Bhd to Sarawak Consolidated Industries Bhd (SCIB) in May 2022. The contract, encompassing engineering, procurement, construction, and commissioning, was for a road project connecting multiple locations in Sarawak, Malaysia, and was successfully completed in March 2023.

- Vietnam, with its extensive coastline of 3,260 km and a network of rivers, presents significant opportunities in maritime freight transportation. The Vietnamese government has set ambitious targets, aiming to position the nation as a leading maritime power by 2030. These goals include elevating the maritime sector's GDP contribution to 10% and amplifying the economic significance of its 28 coastal cities and provinces, targeting a 65% to 70% share of the overall Vietnamese GDP.

Rising e-commerce trends and initiatives imposed by the government are driving the market's growth

- Vietnam's Ministry of Transport plans to break ground on 14 infrastructure projects and complete 50 more by 2025, including key parts of the North-South Expressway. This is part of the goal to expand the country's expressways to 3,000 km by 2025, up from the current 2,021 km. Additionally, the Long Thanh International Airport, a USD 14.12 billion project in Dong Nai province, is on track to finish in 2025. Once completed, it will be the country's largest airport, easing congestion at Tan Son Nhat in Ho Chi Minh City.

- In November 2023, BBN Airlines Indonesia expanded its fleet by adding a third freighter, underscoring the robust growth of the nation's all-cargo market. The ACMI carrier, a subsidiary of Avia Solutions Group, announced the acquisition of a Boeing 737-400SF, enhancing its current fleet of two 737-800Fs. The aircraft, began commercial operations in 2024. Given Indonesia's vast archipelago, which spans 17,000 islands over 5,150 km, air transportation is crucial. The International Air Transport Association (IATA) forecasts that by 2034, Indonesia will rank as the world's sixth-largest air transport market.

ASEAN Freight and Logistics Market Trends

Rising FDI in ASEAN countries supported by infrastructure construction projects by country governments driving economic growth

- In May 2024, the Japanese government announced a loan of about JPY140.7 billion (USD 900 million) to build a high-speed rail line in Jakarta, Indonesia. The East-West rail project will cover 84.1 km and be completed in two phases, starting in 2026 and finishing by 2031. The new rail line will feature Japanese technology for trains and signaling systems. Such initiatives are expected to boost GDP contribution from transport and storage sector.

- In February 2024, the Transport Ministry announced plans to invest USD 18.83 billion in around 150 transport projects by the end of 2025 to enhance Thailand's infrastructure. In 2024, 64 projects will commence, with an additional 31 projects valued at USD 11.23 billion in the pipeline. For 2025, there are 57 new projects planned, totaling USD 7.59 billion. These initiatives include 18 motorway projects, 9 railway projects, and plans for regional port development, all aimed at bolstering the transport and storage sector's contribution to GDP in the future.

Impact of the Iran-Israel conflict and Ukraine-Russia war on ASEAN countries led to increased fuel prices and supply chain disruptions

- Indonesia expects a 29% increase in oil and gas sector investments in 2024 to boost drilling and exploration after Shell and Chevron's recent exits. This push is vital for Indonesia to counter a long-term decline in output amid rising financing challenges for fossil fuel projects. Foreign companies like Eni, Exxon Mobil, and BP will contribute 40% of 2024's planned investments. Also, in early 2024, the Ministry of Oil and Gas announced that fuel prices at gas stations will stay stable until at least June 2024, despite the Iran-Israel conflict potentially raising oil prices to USD 100 per barrel.

- Diesel prices in Malaysia surged by over 50% in June 2024 as part of Prime Minister Anwar Ibrahim's efforts to reform the country's long-standing fuel subsidy system. The restructuring aimed to alleviate pressure on national finances by eliminating universal energy subsidies and focusing assistance on those most in need. This move also aims to address issues like the smuggling of subsidized diesel to neighboring countries, where it fetches higher prices.

ASEAN Freight and Logistics Industry Overview

The ASEAN Freight and Logistics Market is fragmented, with the major five players in this market being Deutsche Bahn AG (including DB Schenker), DHL Group, FedEx, Kuehne+Nagel and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Indonesia

- 4.21.2 Malaysia

- 4.21.3 Thailand

- 4.21.4 Vietnam

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Indonesia

- 4.22.2 Malaysia

- 4.22.3 Thailand

- 4.22.4 Vietnam

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Thailand

- 5.3.4 Vietnam

- 5.3.5 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alps Logistics

- 6.4.2 Deutsche Bahn AG (including DB Schenker)

- 6.4.3 DHL Group

- 6.4.4 DP World

- 6.4.5 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.6 FedEx

- 6.4.7 JWD Group

- 6.4.8 Kuehne+Nagel

- 6.4.9 NYK (Nippon Yusen Kaisha) Line

- 6.4.10 Tiong Nam Logistics Holdings Bhd

- 6.4.11 United Parcel Service of America, Inc. (UPS)

- 6.4.12 YCH Group

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate