|

市場調査レポート

商品コード

1685800

アジア太平洋の貨物・ロジスティクス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia Pacific Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の貨物・ロジスティクス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 443 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

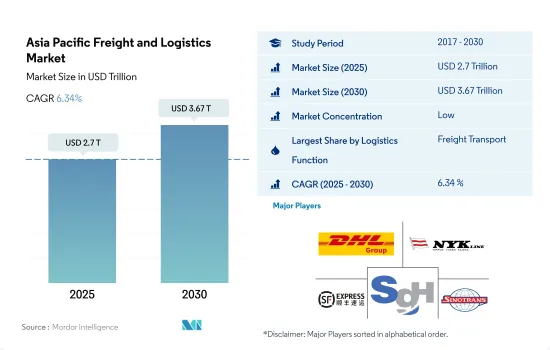

アジア太平洋の貨物・ロジスティクス市場規模は2025年に2兆7,000億米ドルと推定され、2030年には3兆6,700億米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは6.34%で成長します。

アジア開発銀行が同国のインフラ整備を支援、貨物輸送需要を後押し

- 2023年3月以降、中国浙江省の寧波近郊にある2つの主要コンテナ・トラック・ヤードでは、3,000台近い遊休車両の過剰に悩まされています。これらのヤード、横埔と北侖は港の運営と密接に結びついています。しかし、過去2年間、これらの港湾の輸送量は著しく減少しています。コンテナの集積は、中国の低い保管コスト、パンデミックによる輸出ブーム時のコンテナ供給の急増、ブーム沈静後に戻ってきた相当数のコンテナなどの要因によるものと考えられます。

- アジア開発銀行(ADB)は、計画、建設、メンテナンスなど、接続インフラに関連する太平洋DMC(新興諸国)の取り組みを積極的に支援しています。交通プロジェクトだけでも、太平洋地域におけるADBのポートフォリオの59%以上を占めています。ADBによるこのような強力な支援は、太平洋地域におけるより強固で持続可能な成長軌道を促進しています。今後、太平洋地域の運輸セクターに対するADBの投資は16億米ドルを上回ると予測され、2022年から2024年にかけて22のプロジェクトが資金提供を予定しており、その中には注目すべき1億1,500万米ドルの協調融資も含まれています。

アジア太平洋における持続可能で強靭な貨物・ロジスティクスセクターの構築

- インドでは、輸送コストが物流を支配しており、物流コスト全体の62%、GDPの14%を占めています。ディーゼル燃料費が輸送費の大部分を占めていることを考えると、ゼロ・エミッション・トラック(ZET)を採用することで、車両の耐用年数を通じて燃料費を最大46%大幅に削減することができます。これはインド経済にとって広範囲な意味を持っています。特に、すでに石油輸入費用の4分の1以上を占めている道路貨物は、2050年までに4倍に急増すると予測されています。ZETを採用することで、インドは2050年までに8,380億リットルものディーゼルを節約できる可能性があり、これは1,401億7,000万米ドルの石油支出削減につながります。

- 限られた新規供給、老朽化した施設、オンライン小売の急増による消費者の嗜好の変化といった要因が重なり、アジア太平洋の冷蔵倉庫への投資は、2032年までに年間50億米ドルに達すると予測されています。この急増は主に、同地域におけるコールドチェーン倉庫の需要の高まりによるものです。

アジア太平洋の貨物・ロジスティクス市場の動向

アジア太平洋の貨物需要は世界の海上貿易に牽引され、これが輸送セクターへの投資の引き金となっています。

- 2024年5月17日、日本の東京駅で開催された見本市では、高速旅客列車の軽貨物への利用が拡大していることが強調されました。このシフトは、商業運転手の不足と新しい時間外労働法に後押しされ、道路配送コストを最大20%増加させました。JR東日本は2023年8月から、12両編成のE系専用車両を使った新潟発東京行きの当日配送サービスを実施しています。輸送品目は生鮮食品、菓子類、飲料、花、精密部品、医療品など。2023年9月、JR東日本は東北新幹線で貨物専用サービスを開始し、現在は高速および特急ネットワークで「はこBYUN」ブランドの貨物サービスを提供しています。

- 第14次5ヵ年計画(2021~2025年)において、中国は交通網拡大の目標を明らかにしました。2025年までに、高速鉄道は2020年の38,000kmから50,000kmに延長され、人口50万人以上の都市の95%が250kmの路線でカバーされます。2025年までに、鉄道を165,000km、民間空港を270以上、都市部の地下鉄を10,000km、高速道路を190,000km、高水準内陸水路を18,500kmに増やすことを目標としています。主な目標は、2025年までに総合開発を達成することであり、交通システムの変革とGDPへの貢献の進展を重視しています。

世界の不確実性に起因して、アジア諸国のほとんどが石油の純輸入国であるため、原油価格が高騰しています。

- 2023年、中国の原油輸入量は11%増の5億6,399万MTとなったが、これはロシア・ウクライナ戦争による世界の原油価格の上昇が原因でした。2024年初頭には、中国が先の価格下落を利用したため、輸入量は前年比5.1%増の8,831万トンに達しました。ブレント先物は2023年9月に97.69米ドルでピークを迎え、12月には72.29米ドルまで下落し、2024年3月には84.05米ドルまで上昇しました。OPEC+が2024年3月に減産延長を決定したことで、価格はさらに上昇し、世界の需要に対する懸念が高まり、2024年下半期の中国の輸入が鈍化する可能性があります。

- オーストラリア連邦政府は、2025年1月1日から乗用車と小型商用車の新燃費基準を導入します。これは、新法の起草に先立つ1ヶ月間の協議期間を経たものです。2023年予算の一部として発表され、2023年4月に発表されたEV戦略と連動するこの基準は、自動車メーカーに平均CO2目標を設定します。これらの目標は徐々に減少し、より燃費の良い低排出ガス車やゼロエミッション車の生産が求められます。

アジア太平洋の貨物・ロジスティクス業界の概要

アジア太平洋の貨物・ロジスティクス市場は細分化されており、DHLグループ、日本郵船、SFエクスプレス(KEX-SF)、SGホールディングス、SINOTRANS(アルファベット順)が主要5社となっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- トラック輸送コスト

- タイプ別トラック保有台数

- 物流実績

- 主要トラックサプライヤー

- モーダルシェア

- 海上貨物輸送能力

- 定期船の接続性

- 寄港地とパフォーマンス

- 運賃動向

- 貨物トン数の動向

- インフラ

- 規制の枠組み(道路と鉄道)

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- タイ

- ベトナム

- 規制の枠組み(海上および航空)

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 物流機能

- クーリエ、エクスプレス、小包(CEP)

- 仕向地別

- 国内

- 国際

- 貨物輸送

- 輸送モード別

- 航空

- 海上・内水道

- その他

- 貨物輸送

- 輸送手段別

- 航空

- パイプライン

- 鉄道

- 道路

- 海上・内陸水路

- 倉庫保管

- 温度管理

- 温度管理なし

- 温度管理

- その他のサービス

- クーリエ、エクスプレス、小包(CEP)

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Alps Logistics

- C.H. Robinson

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DP World

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- FedEx

- Kuehne+Nagel

- NYK(Nippon Yusen Kaisha)Line

- SF Express(KEX-SF)

- SG Holdings Co., Ltd.

- SINOTRANS

- United Parcel Service of America, Inc.(UPS)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

- 為替レート

目次

Product Code: 47682

The Asia Pacific Freight and Logistics Market size is estimated at 2.7 trillion USD in 2025, and is expected to reach 3.67 trillion USD by 2030, growing at a CAGR of 6.34% during the forecast period (2025-2030).

Asian Development Bank assists the infrastructure development in the country, boosting freight transport demand

- Since March 2023, two major container truck yards in Zhejiang province, China, near Ningbo, have grappled with an excess of nearly 3,000 idle vehicles. These yards, Hengpu and Beilun, are closely tied to the port's operations. However, they have experienced a notable decline in traffic over the past two years. The accumulation of containers can be attributed to factors such as China's low storage costs, a surge in container supply during the pandemic's export boom, and a significant number of containers returning after the boom subsided.

- The Asian Development Bank (ADB) is actively supporting Pacific DMCs (Developing Member Countries) in their endeavors related to connectivity infrastructure, including planning, construction, and maintenance. Transport projects alone account for over 59% of the ADB's portfolio in the Pacific. This robust support from the ADB is fostering a more robust and sustainable growth trajectory in the Pacific region. Looking ahead, ADB's investments in the Pacific's transportation sector are projected to surpass USD 1.6 billion, with 22 projects slated for funding during 2022-2024, including a notable USD 115 million in co-financing.

Building a sustainable and resilient freight and logistics sector in the Asia Pacific region

- In India, transportation costs dominate the logistics landscape, accounting for 62% of overall logistics costs and 14% of the country's GDP. Given that diesel fuel costs make up the lion's share of transportation expenses, the adoption of zero-emission trucks (ZETs) can significantly slash fuel costs by up to 46% over the vehicle's lifespan. This has far-reaching implications for India's economy. Notably, road freight, which already accounts for over a quarter of oil import expenses, is projected to surge fourfold by 2050. By embracing ZETs, India could potentially save a staggering 838 billion liters of diesel by 2050, translating to a reduction of USD 140.17 billion in oil expenditures.

- With a confluence of factors such as limited new supply, outdated facilities, and evolving consumer preferences driven by the surge in online retail, investments in cold storage properties in the Asia-Pacific were projected to hit USD 5 billion annually by 2032. This surge is primarily driven by the escalating demand for cold chain warehousing in the region.

Asia Pacific Freight and Logistics Market Trends

Asia Pacific freight demands driven by global seaborne trade, which is triggering transport sector investments

- On May 17, 2024, a fair at Tokyo Station in Japan highlighted the growing use of high-speed passenger trains for light freight. This shift, driven by a shortage of commercial drivers and new overtime laws, has increased road delivery costs by up to 20%. Since August 2023, JR East has been running a same-day delivery service from Niigata to Tokyo using a dedicated 12-car Series E trainset. Items transported include fresh food, confectionery, drinks, flowers, precision components, and medical supplies. In September 2023, JR East launched a freight-only service on the Tohoku Shinkansen and now offers Hakobyun-branded freight services across its high-speed and Limited Express networks.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

Owing to global uncertainties, crude oil prices are soaring in the Asian economies as most of them are net oil importers

- In 2023, China's crude oil imports rose by 11% to 563.99 MMT, driven by higher global oil prices due to the Russia-Ukraine War. In early 2024, imports increased by 5.1% YoY, reaching 88.31 MMT, as China capitalized on lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, dropped to USD 72.29 in December, and rose to USD 84.05 by March 2024. OPEC+'s decision in March 2024 to extend output cuts has further boosted prices, raising concerns about global demand and potentially slowing China's imports in H2 2024.

- Australia's federal government will introduce a new fuel efficiency standard for passenger and light commercial vehicles starting January 1, 2025. This follows a one-month consultation period before drafting the new laws. Announced as part of the 2023 budget and linked to the EV strategy released in April 2023, the standard sets average CO2 targets for vehicle manufacturers. These targets will gradually decrease, requiring the production of more fuel-efficient and low or zero-emissions vehicles.

Asia Pacific Freight and Logistics Industry Overview

The Asia Pacific Freight and Logistics Market is fragmented, with the major five players in this market being DHL Group, NYK (Nippon Yusen Kaisha) Line, SF Express (KEX-SF), SG Holdings Co., Ltd. and SINOTRANS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Australia

- 4.21.2 China

- 4.21.3 India

- 4.21.4 Indonesia

- 4.21.5 Japan

- 4.21.6 Malaysia

- 4.21.7 Thailand

- 4.21.8 Vietnam

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Australia

- 4.22.2 China

- 4.22.3 India

- 4.22.4 Indonesia

- 4.22.5 Japan

- 4.22.6 Malaysia

- 4.22.7 Thailand

- 4.22.8 Vietnam

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alps Logistics

- 6.4.2 C.H. Robinson

- 6.4.3 Deutsche Bahn AG (including DB Schenker)

- 6.4.4 DHL Group

- 6.4.5 DP World

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 FedEx

- 6.4.9 Kuehne+Nagel

- 6.4.10 NYK (Nippon Yusen Kaisha) Line

- 6.4.11 SF Express (KEX-SF)

- 6.4.12 SG Holdings Co., Ltd.

- 6.4.13 SINOTRANS

- 6.4.14 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate