|

市場調査レポート

商品コード

1687265

タイの貨物輸送およびロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Thailand Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの貨物輸送およびロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 335 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

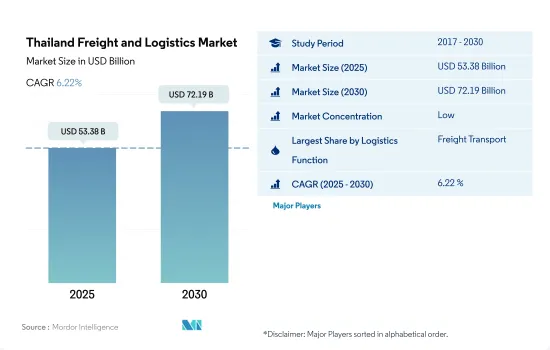

タイの貨物輸送およびロジスティクス市場規模は2025年に533億8,000万米ドルと推定され、2030年には721億9,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは6.22%で成長すると予測されます。

運輸部門のGDP寄与率の上昇で貨物市場への投資機会が増加

- 2023年、タイ政府は2,900億バーツ(88億米ドル)相当の東部航空都市プロジェクトを開始しました。これは、ラヨーンのベトナム戦争にさかのぼる施設であるウタパオ空港を、世界の航空ハブに変貌させるというものです。アップグレードされた空港は、ドンムアン空港やスワンナプーム空港と結ばれます。1,040ヘクタールに及ぶこのプロジェクトには、新ターミナルの建設と貨物自由貿易地域の設立が含まれます。

- タイは2030年までに年間生産台数250万台の約30%をEVに転換することを目指しており、EV製造への投資と転換を促進するためのインセンティブを準備しています。タイは、電気自動車の研究開発センターを設立するメーカーに優遇措置や税制優遇措置を提供する計画で、地域のEVフロントランナーとして初期の成功を築こうとしています。中国のさまざまな自動車メーカーがタイでの新たな生産施設に14億4,000万米ドルの投資を約束しており、BYDは年間15万台のEVを生産するために約5億米ドルを投資しています。

タイの貨物輸送およびロジスティクス市場の動向

タイの輸送・保管部門は2022年に国際貿易とeコマースに牽引され成長を遂げた

- 2023年の経済成長率は低下したもの、政府は景気刺激策としてFDIと観光を後押しし、タイが特に電気トラックの製造拠点となることに貢献しました。さらに、2023年に最終決定された「EV 3.5パッケージ」では、車両1台当たり2,889.23米ドルの購入補助金が減額され、この分野からのGDP貢献をさらに後押しします。

- 2024年2月、運輸省は国のインフラを強化するため、2025年末までに約150の運輸プロジェクトに188億3,000万米ドルを投資する計画を発表しました。2024年には64のプロジェクトが開始され、さらに31のプロジェクト(112億3,000万米ドル相当)が進行中です。2025年には57の新規プロジェクトが計画されており、総額は75億9,000万米ドルにのぼる。これらの構想には、18の高速道路プロジェクト、9の鉄道プロジェクト、地域の港湾開発計画が含まれ、これらはすべて、将来の輸送・貯蔵部門のGDPへの貢献を強化することを目的としています。

燃料費補助のための2023年国家基金として23億5,000万米ドルが閣議決定されました。

- タイ政府は世界の原油価格高騰の影響を緩和するため、2022年2月からディーゼル消費税を免除することを決定したが、これにより政府は45億6,000万米ドルの歳入を失うことになりました。2022年2月から2024年3月までの間、国内ディーゼル価格を1リットルあたり1.01米ドル前後に維持する上で、免税と基金によるディーゼル価格補助が重要な役割を果たしました。世界の原油価格の下落を受けて、ディーゼル価格は2023年2月以降徐々に下がり、1リットル当たり0.92米ドルとなっています。タイ政府は高インフレとの戦いの中、燃料費補助のための国家基金として2023年にも23億5,000万米ドルの新規借り入れを閣議決定しました。

- 経済成長の鈍化が予想されるにもかかわらず、タイの精製油需要、特にジェット燃料の需要は2024年に増加すると予測されています。ジェット燃料の消費量は、2023年の1,350万LDから24.2%増の1日平均1,680万LDになると予測されます。ディーゼル、ガソリン、ガソホールは現在、国の価格補助制度の対象となっています。さらに、2024年にはLNG価格の下落が予想され、発電所経営者は重油への依存度を下げることになります。

タイの貨物輸送およびロジスティクス産業の概要

タイの貨物輸送およびロジスティクス市場は断片化されており、同市場の主要企業はドイツ鉄道AG(DBシェンカーを含む)、DHLグループ、フェデックス、JWDグループ、ユナイテッド・パーセル・サービス・オブ・アメリカ(UPS)の5社である(アルファベット順)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- トラック輸送コスト

- タイプ別トラック保有台数

- 物流実績

- 主要トラックサプライヤー

- モーダルシェア

- 海上貨物輸送能力

- 定期船の接続性

- 寄港地とパフォーマンス

- 運賃動向

- 貨物トン数の動向

- インフラ

- 規制の枠組み(道路と鉄道)

- タイ

- 規制の枠組み(海上・航空)

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 物流機能

- クーリエ、エクスプレス、パーセル(CEP)

- 仕向地別

- 国内

- 国際

- 貨物輸送

- 輸送モード別

- 航空

- 海上・内水道

- その他

- 貨物輸送

- 輸送手段別

- 航空

- パイプライン

- 鉄道

- 道路

- 海上・内陸水路

- 倉庫保管

- 温度管理別

- 温度管理なし

- 温度管理

- その他のサービス

- クーリエ、エクスプレス、パーセル(CEP)

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- FedEx

- JWD Group

- Kuehne+Nagel

- ProFreight Group

- Sub Sri Thai Public Company Ltd.

- Toyota Tsusho Corporation(including Toyota Tsusho Thai Holdings Co., Ltd.)

- Triple I Logistics Public Company Ltd.

- United Parcel Service of America, Inc.(UPS)

- WICE Logistics Public Company Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

- 為替レート

目次

Product Code: 58019

The Thailand Freight and Logistics Market size is estimated at 53.38 billion USD in 2025, and is expected to reach 72.19 billion USD by 2030, growing at a CAGR of 6.22% during the forecast period (2025-2030).

Rising GDP contribution of the transport sector increases investment opportunities in the freight market

- In 2023, the Thai government initiated the Eastern Aviation City project worth THB 290 billion (USD 8.8 billion). This involves the transformation of U-Tapao Airport, a facility dating back to the Vietnam War in Rayong, into a global aviation hub. The upgraded airport will be linked to Don Muang Airport and Suvarnabhumi Airport. Spanning 1,040 hectares, the project encompasses the construction of a new terminal and the establishment of a cargo-free trade zone.

- Thailand aims to convert about 30% of its annual production of 2.5 million vehicles into EVs by 2030 and is preparing incentives to encourage more investment and conversion into EV manufacturing. Thailand plans to provide incentives and tax breaks for manufacturers setting up electric vehicle R&D centers as it seeks to build on early success as a regional EV frontrunner. Various Chinese automobile manufacturers have committed to invest USD 1.44 billion in new production facilities in Thailand, with BYD investing nearly USD 500 million to produce 150,000 EVs a year.

Thailand Freight and Logistics Market Trends

Thailand's transport and storage sector experienced growth in 2022 driven by international trade and e-commerce

- Despite a decline in economic growth in 2023, the government boosted FDI and tourism to act as economic stimulus and contribute towards Thailand becoming a manufacturing hub especially for electric trucks. Furthermore, the recently finalized "EV 3.5 package" in 2023 offers a reduced purchase subsidy of USD 2,889.23 per vehicle, further supporting GDP contribution from the sector.

- In February 2024, the Transport Ministry announced plans to invest USD 18.83 billion in around 150 transport projects by the end of 2025 to enhance the country's infrastructure. In 2024, 64 projects will commence, with an additional 31 projects valued at USD 11.23 billion in the pipeline. For 2025, there are 57 new projects planned, totaling USD 7.59 billion. These initiatives include 18 motorway projects, 9 railway projects, and plans for regional port development, all aimed at bolstering the transport and storage sector's contribution to GDP in the future.

USD 2.35 billion was approved by Thailand's cabinet for the 2023 state fund to subsidize fuel costs

- The Thai government decided to waive the diesel excise tax from February 2022 to relieve the impact of the global oil price surge, but this led the government to lose USD 4.56 billion in revenue. The tax exemption and the diesel price subsidy under the fund played a key role in keeping the domestic diesel price at around USD 1.01 a liter since Feb 2022 till March 2024. The diesel price has gradually fallen since February 2023 to USD 0.92 a liter in response to declining global oil prices. Thailand's cabinet approved another USD 2.35 billion of new borrowing in 2023 for a state fund to subsidize fuel costs as the government battles high inflation.

- Despite an anticipated sluggish economic growth, demand for refined oil in Thailand, particularly jet fuel, is predicted to rise in 2024. Jet fuel consumption is forecasted to grow by 24.2% to an average of 16.8 million litres per day (MLD), up from 13.5 MLD in 2023. Diesel, gasoline, and gasohol are currently part of a state price subsidy program. Additionally, LNG prices are expected to decrease in 2024, leading power plant operators to rely less on fuel oil.

Thailand Freight and Logistics Industry Overview

The Thailand Freight and Logistics Market is fragmented, with the major five players in this market being Deutsche Bahn AG (including DB Schenker), DHL Group, FedEx, JWD Group and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Thailand

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Thailand

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Deutsche Bahn AG (including DB Schenker)

- 6.4.2 DHL Group

- 6.4.3 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.4 FedEx

- 6.4.5 JWD Group

- 6.4.6 Kuehne+Nagel

- 6.4.7 ProFreight Group

- 6.4.8 Sub Sri Thai Public Company Ltd.

- 6.4.9 Toyota Tsusho Corporation (including Toyota Tsusho Thai Holdings Co., Ltd.)

- 6.4.10 Triple I Logistics Public Company Ltd.

- 6.4.11 United Parcel Service of America, Inc. (UPS)

- 6.4.12 WICE Logistics Public Company Ltd.

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate