|

市場調査レポート

商品コード

1938998

米国の建設化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United States Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の建設化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

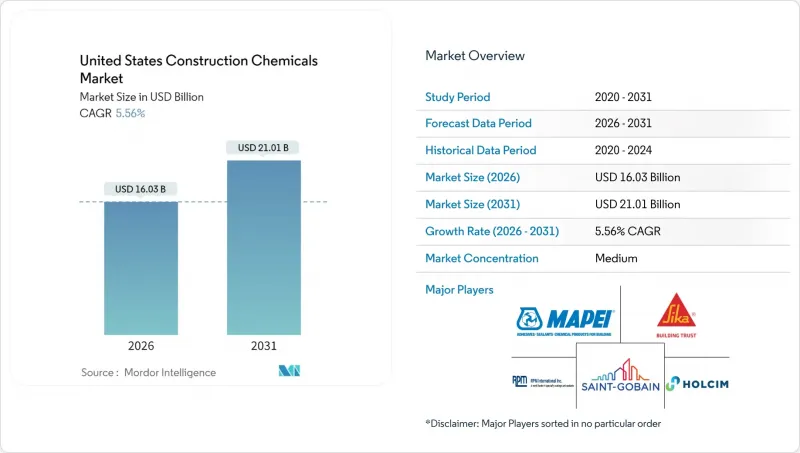

米国建設用化学品市場は、2025年の151億9,000万米ドルから2026年には160億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.56%で推移し、2031年までに210億1,000万米ドルに達すると予測されています。

複数の連邦インフラ計画、建築基準の厳格化、現場作業フローの急速なデジタル化が需要を支えております。一方で、変動する石油原料価格や労働力不足が利益率を圧迫しております。連邦政府による低炭素材料の調達優先政策が、バイオベース混和剤や低VOC塗料への移行を加速させております。また、データセンターや半導体への投資が、高性能床材システムの潜在市場を拡大しております。特にハリケーン多発州における気候変動対策法は、風雨や水圧に耐える防水膜の仕様基準引き上げを促進しています。同時に、大手メーカーによる垂直統合の動きは流通業者の利益率を圧迫する一方、物流環境が逼迫する中で下流の建設業者に対し、より予測可能な供給体制を提供しています。

米国建設用化学品市場の動向と洞察

インフラ法案による大型プロジェクト

インフラ投資・雇用創出法を通じて投入される連邦資金により、橋梁やトンネルの耐用年数を60年以上延長する高耐久性混和剤、耐食性コーティング、結晶系防水システムの需要が加速しています。鉄道路線変更や港湾拡張工事を請け負う建設業者は、混雑した現場でのポンプ送水性を向上させる低収縮性高性能減水剤を指定するケースが増加しています。移動式配合試験所を保有するサプライヤーは、継続的な配合検証が多くの公共契約に明記されるようになったため、複数年にわたる供給契約を獲得しています。州間高速道路回廊周辺の地域クラスターにより、製造業者はリードタイムの短縮、輸送コストの削減、施工ミスを軽減する現場技術トレーニングの提供が可能となっています。

住宅着工件数の回復と修繕需要の蓄積

住宅ローン金利の低下に伴い、一戸建て住宅の建築許可件数は増加傾向にあります。一方、5,743億米ドル規模の住宅改修市場では、2025年まで積み上がった修繕需要が押し寄せています。新築と改修の両方の需要が重なる状況は、多目的防水シート、低VOCシーラント、ひび割れ補修モルタルに有利に働いています。これらは、長期間の操業停止を伴わずに、居住中の建物の改修を可能にします。米国建設用化学品市場は、小型パッケージや色調調整済みシーラントによる消費者のリピート購入を生むDIYチャネルから継続的な恩恵を受けています。防湿材と表面処理材をセット販売する流通業者は、住宅所有者が断熱材・床材・外壁改修を単一プロジェクトで同時施工する傾向から、高単価販売を実現しています。

変動する石油由来原料価格

物流のボトルネックや床材請負業者の入札価格差拡大を背景に、2025年にはエポキシ樹脂価格が上昇し、固定金額契約へのエスカレーター条項導入を余儀なくされました。ヘッジング手段を持たない小規模な地域混合業者は、支払いサイクルの長期化に伴い運転資金の逼迫に直面し、米国建設化学品市場における統合を促しています。一部のメーカーは、マージンの変動を緩和するため、バイオベースの希釈剤や再生PETポリオールへの配合変更を進めていますが、供給量は依然として限られています。原材料価格の変動は公共事業の予算編成も複雑化させています。多くの州では入札開始よりかなり前に年間予算を確定させるため、資金調達と調達コストの間に不一致が生じるからです。

セグメント分析

防水ソリューションは2025年に米国建設化学品市場で34.42%と最大のシェアを占め、2031年までCAGR6.05%で拡大が見込まれます。この優位性は、商業・住宅建築双方における建築基準法で義務付けられた連続気密層と、保険需要に後押しされた防湿性能向上のニーズを反映しています。液体塗布型防水シートはシート材を上回る成長を見せています。スプレー施工により複雑な貫通部をシームレスに覆い、故障点となり得る継ぎ目を排除できるためです。ハリケーン発生頻度の増加に伴い、沿岸地域の建設業者は1万回の疲労サイクルに耐える試験済みのエラストマー系防水シートを選択する傾向にあります。この特性は15%の価格プレミアムを伴いますが、生涯修理費用を削減します。

シームレスな防水シートの普及は、湿潤下での施工が可能な一液型湿気硬化ポリウレタン系製品に有利に働いています。工事業者からは、新開発の低臭気配合により負圧テントを必要とせず屋内施工が可能となり、地下駐車場への適用範囲が広がったとの報告が寄せられています。持続可能性指標も重要であり、再生材35%含有の水性アクリル系防水シートは、現在、公共住宅プロジェクトにおける連邦税制優遇の対象となります。EPAが溶剤規制の強化を検討する中、メーカーは柔軟性と超低VOC排出を両立するシリル末端ポリエーテル骨格への投資を進めています。これらの動向が相まって、防水システムは予測期間を通じて米国建設化学品市場における主導的地位を維持する見込みです。

米国建設用化学品レポートは、製品別(接着剤、アンカー・グラウト、コンクリート混和剤、コンクリート保護塗料、床用樹脂、補修・再生用化学品、シーラント、表面処理化学品など)および用途別(商業施設、産業・公共施設、インフラ、住宅)に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インフラ法案による大型プロジェクト

- 住宅着工件数の回復と修繕需要の積み残し

- 高性能・環境配慮型混和剤への移行

- 建築基準法に基づく防水・保護コーティングの採用拡大

- データセンターの急成長が特殊床材の需要を牽引

- 市場抑制要因

- 石油由来原料価格の変動性

- VOCおよび有害化学物質規制の強化

- 高度なシステム向けの熟練施工者の不足

- バリューチェーン分析

- 規制情勢

- ポーターのファイブフォース

- 競争企業間の敵対関係

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

第5章 市場規模と成長予測

- 製品別

- 接着剤

- ホットメルト

- 反応性

- 溶剤系

- 水性

- アンカー及びグラウト

- セメント系固定剤

- 樹脂固定

- コンクリート混和剤

- 加速剤

- 空気混入剤

- 高性能減水剤

- 遅延剤

- 収縮抑制剤

- 粘度調整剤

- 可塑剤

- その他

- コンクリート保護コーティング

- アクリル

- アルキド樹脂

- エポキシ樹脂

- ポリウレタン

- その他の樹脂

- 床用樹脂

- アクリル

- エポキシ樹脂

- ポリアスパラギン酸樹脂

- ポリウレタン

- その他の樹脂

- 補修・改修用化学製品

- 繊維巻き付けシステム

- 注入グラウティング

- マイクロコンクリートモルタル

- 改質モルタル

- 鉄筋保護材

- シーラント

- アクリル

- エポキシ樹脂

- ポリウレタン

- シリコーン

- その他の樹脂

- 表面処理用化学品

- 養生剤

- 離型剤

- その他

- 防水ソリューション

- 化学品

- 防水シート

- 接着剤

- エンドユーザー分野別

- 商業用

- 産業・公共施設

- インフラストラクチャー

- 住宅用

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア**(%)/順位分析

- 企業プロファイル

- 3M

- Arkema

- Ashland

- Dow

- Kingspan Group

- Henkel AG & Co. KGaA

- HOLCIM

- ARDEX Americas

- MAPEI S.p.A.

- LATICRETE International, Inc

- RPM International Inc.

- Sika AG

- Saint-Gobain

- Xypex USA

第7章 市場機会と将来展望

- ホワイトスペースと未充足ニーズの評価