|

市場調査レポート

商品コード

1684082

タイの建設用化学品-市場シェア分析、産業動向、成長予測(2025年~2030年)Thailand Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの建設用化学品-市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 346 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

タイの建設用化学品市場規模は2024年に6億9,033万米ドルと推定・予測され、2030年には9億7,896万米ドルに達し、予測期間中(2024年~2030年)のCAGRは5.99%で成長すると予測されます。

タイの住宅建設セクターにおける建設用化学品のニーズの高まりが市場成長を後押しする見込み

- 2022年、タイの建設用化学品市場は、建設活動と材料価格の上昇に牽引され、11.45%の需要急増を示しました。この上昇は、2021年と比較して需要と利益の増加につながりました。建築プロジェクトの増加により、建設用化学製品の特徴や用途に対する認識が高まっており、2023年の需要は前年比4.5%増と予測されます。

- 主に非住宅建築物が多いことから、工業・施設セクターが市場を独占しています。また、タイ経済の重要な柱である製造業セクターは、これまでも外国からの投資を受け入れており、今後も継続的な投資が期待されています。こうした要因が、このセクターにおける建築用化学品の需要を押し上げています。

- 第2位の需要シェアを誇る住宅部門は、タイの都市人口集中の恩恵を受けています。この都市密度の高さは、旺盛な住宅需要につながり、建設用化学薬品の重要な市場を形成しています。特筆すべきは、水害の軽減に欠かせない防水ソリューションで、2022年の同部門の総需要の35%近くを占めています。

- 今後を展望すると、住宅部門が建設用化学品製品需要の最速成長を示すことになり、予測期間中(2023年~2030年)のCAGRは6.5%と予測されます。この急増は、同国で進行中の都市化傾向と、政府の住宅政策に後押しされた手頃な価格の住宅需要の増加が予想されることに支えられています。

タイの建設用化学品市場の動向

外国直接投資(FDI)と観光の増加が同分野の成長を後押し

- 2022年、タイの商業建設セクターは2021年比で20%の数量急増を経験し、COVID-19の大流行からの回復を示しました。この回復がGDPの2.6%増にも貢献しました。この拡大は主に外国直接投資(FDI)の急増によるもので、全国的なオフィススペース、倉庫、小売店の追加需要の高まりにつながっています。

- 2018年から2021年にかけて、タイの商業建設部門の新規床面積は2.82%減少しました。この落ち込みはパンデミックの直接的な結果であり、オフィスや小売店などの商業スペースに対する需要の減少につながりました。2020年と2021年は特に課題となっており、新規床面積は2019年と比較してそれぞれ31.33%と15.17%と大幅に減少しました。パンデミックによる渡航制限やサプライチェーンの途絶といった制約がさらに状況を悪化させ、労働力不足や資材不足につながりました。

- タイの商業スペースの需要は、観光客の急増と2022年の外国直接投資(FDI)の前年比36%増に後押しされ、増加傾向にあります。このFDIの増加は、タイでの事業設立に対する海外企業の関心の高まりを示唆しています。これがオフィススペースの需要をさらに高めています。予測期間中、商業建築セクターの新設床面積は堅調な伸びを示し、CAGRは4.52%と予測されます。

国家住宅局(NHA)やクルンタイ銀行(KTB)などの住宅計画がタイの住宅セクターを後押しする

- 東南アジアで高度に都市化されたタイは、堅調な住宅建設部門を誇っています。2022年には、新設床面積が前年比14.24%増となり、顕著な上昇を見せた。2023年も住宅セクターの成長は続き、2022年の数字を100万平方メートル近く上回りました。この好調な軌道は、同国の安定した経済と一人当たり所得の緩やかな上昇に支えられています。

- 住宅建設部門は、2020年にCOVID-19パンデミックの影響を受け、大幅な後退に直面しました。それに続く景気後退は、旅行制限や雇用喪失と相まって、住宅建設量を2019年から11%減少させました。しかし、2021年には、このセクターは見事に回復し、13%の数量急増を示しました。この復活は、パンデミックの影響が薄れたことと、タイ中央銀行が年間を通じて0.5%という記録的な低政策金利を維持するなど、政府の戦略的施策に起因しています。こうした施策が購買意欲を刺激し、新築住宅需要を後押ししました。

- 予測期間中、タイの住宅建設新規床面積は成長し、CAGRは4.25%と予測されます。この成長は、1人当たりGDPの上昇(2023年に2.8%、2024年に3.2%の成長が見込まれる)、急速な都市化、外国投資の増加、積極的な住宅計画など、いくつかの要因によるものと考えられます。特に、国家住宅局(NHA)とクルンタイ銀行(KTB)は不動産開発業者にインセンティブを提供し、低所得者向けの手頃な住宅建設を奨励しています。

タイの建設用化学品産業の概要

タイの建設用化学品市場は適度に統合されており、上位5社で50.28%を占めています。この市場の主要企業は以下の通り。 Fosroc, Inc., MBCC Group, Saint-Gobain, Sika AG and TOA Paint(Thailand)Public Company Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途分野の動向

- 商業

- 産業・施設

- インフラ

- 住宅

- 主要インフラプロジェクト(現在および発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途セクター

- 商業

- 産業・施設

- インフラ

- 住宅

- 製品

- 接着剤

- サブプロダクト別

- ホットメルト

- 反応性

- 溶剤系

- 水系

- アンカーとグラウト

- サブプロダクト別

- セメント系固定材

- 樹脂固定

- その他のタイプ

- コンクリート混和剤

- サブプロダクト別

- 促進剤

- 空気混入混和剤

- 高範囲減水剤(超可塑剤)

- 遅延剤

- 収縮低減混和剤

- 粘度調整剤

- 減水剤(可塑剤)

- その他のタイプ

- コンクリート保護塗料

- サブプロダクト別

- アクリル系

- アルキド

- エポキシ

- ポリウレタン

- その他の樹脂

- フローリング用樹脂

- サブプロダクト別

- アクリル

- エポキシ

- ポリアスパラギン

- ポリウレタン

- その他の樹脂タイプ

- 補修・再生ケミカル

- サブプロダクト別

- ファイバーラッピングシステム

- 注入グラウト材

- マイクロコンクリートモルタル

- 改質モルタル

- 鉄筋保護材

- シーリング材

- サブプロダクト別

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

- 表面処理薬品

- サブプロダクト別

- 硬化コンパウンド

- 離型剤

- その他の製品タイプ

- 防水ソリューション

- サブプロダクト別

- ケミカル

- メンブレン

- 接着剤

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Act(Thailand)Co., Ltd.

- Ardex Group

- Cemkrete Inter Co., Ltd

- CORMIX INTERNATIONAL LIMITED

- Fosroc, Inc.

- MAPEI S.p.A.

- MBCC Group

- Saint-Gobain

- Sika AG

- TOA Paint(Thailand)Public Company Limited

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50002035

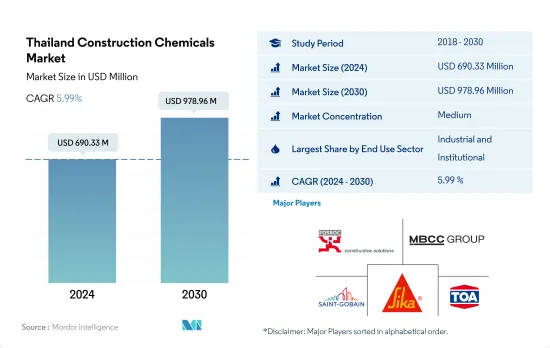

The Thailand Construction Chemicals Market size is estimated at 690.33 million USD in 2024, and is expected to reach 978.96 million USD by 2030, growing at a CAGR of 5.99% during the forecast period (2024-2030).

The growing need for construction chemicals in Thailand's housing construction sector is expected to boost the market growth

- In 2022, Thailand's construction chemicals market witnessed an 11.45% surge in demand, driven by a rise in construction activities and material prices. This uptick translated into higher demand and profits compared to 2021. With a growing awareness of the features and applications of construction chemicals bolstered by an uptick in building projects, the demand is projected to grow by 4.5% in 2023 compared to the previous year.

- The industrial and institutional sectors dominate the market, primarily due to their abundance of non-residential buildings. Additionally, Thailand's manufacturing sector, a key pillar of the economy, has been a recipient of foreign investments in the past, with expectations of continued inflows. These factors have propelled the demand for construction chemicals in this sector.

- The residential sector, with the second-highest demand share, benefits from Thailand's urban population concentration. This urban density translates into a robust demand for residential buildings, creating a significant market for construction chemicals. Notably, waterproofing solutions, crucial for mitigating water damage, accounted for nearly 35% of the sector's total demand in 2022.

- Looking ahead, the residential sector is poised to witness the fastest growth in construction chemical demand, with a projected CAGR of 6.5% during the forecast period (2023-2030). This surge is underpinned by the country's ongoing urbanization trend and the anticipated rise in demand for affordable housing, buoyed by government housing initiatives.

Thailand Construction Chemicals Market Trends

Rising foreign direct investments (FDI) and tourism will boost the sector's growth

- In 2022, Thailand's commercial construction sector experienced a 20% surge in volume compared to 2021, marking a recovery from the COVID-19 pandemic. This rebound also contributed to a 2.6% rise in the country's GDP. In 2023, the commercial construction sector experienced further growth, with a volume increase of 3 million sq. f. This expansion is primarily driven by a surge in foreign direct investments (FDI), which is leading to higher demand for additional office spaces, warehouses, and retail outlets nationwide.

- From 2018 to 2021, the new floor area in Thailand's commercial construction sector witnessed a 2.82% decline. This dip was a direct consequence of the pandemic, which led to a reduced demand for commercial spaces like offices and retail outlets. The years 2020 and 2021 were particularly challenging, with a significant drop of 31.33% and 15.17%, respectively, in the new floor area compared to 2019. The pandemic-induced restrictions, such as travel limitations and supply chain disruptions, further exacerbated the situation, leading to labor shortages and material scarcities.

- The demand for commercial spaces in Thailand is on the rise, bolstered by a surge in tourism and a 36% growth in foreign direct investments (FDI) in 2022 compared to the previous year. This uptick in FDI signals a growing interest from companies overseas in establishing their operations in Thailand. This is further fueling the demand for office spaces. During the forecast period, the commercial construction sector is projected to witness a steady growth in the new floor area, with a compound annual growth rate (CAGR) of 4.52%.

Housing schemes such as the National Housing Authority (NHA) and Krung Thai Bank (KTB) will boost Thailand's residential sector

- Thailand, a highly urbanized nation in Southeast Asia, boasts a robust residential construction sector. In 2022, the sector witnessed a notable upswing, with a 14.24% increase in new floor area compared to the prior year. In 2023, the residential sector growth continued and surpassed the 2022 figures by nearly 1 million sq. f. This positive trajectory is underpinned by the country's stable economy and a gradual uptick in per capita income.

- The residential construction sector faced a significant setback in 2020, grappling with the repercussions of the COVID-19 pandemic. The ensuing economic downturn, coupled with travel restrictions and job losses, led to an 11% dip in residential construction volume from 2019. However, in 2021, the sector rebounded impressively, witnessing a 13% surge in volume. This resurgence can be attributed to the waning impact of the pandemic and strategic government measures, such as maintaining a record-low policy interest rate of 0.5% throughout the year by the Bank of Thailand. These initiatives bolstered buyer confidence, fueling demand for new residential properties.

- During the forecast period, Thailand's residential construction new floor area is projected to grow, registering a CAGR of 4.25%. This growth can be attributed to several factors, including a rising GDP per capita (expected to grow by 2.8% in 2023 and 3.2% in 2024), rapid urbanization, increased foreign investments, and proactive housing schemes. Notably, the National Housing Authority (NHA) and Krung Thai Bank (KTB) offer incentives to property developers, encouraging the construction of affordable homes for low-income earners.

Thailand Construction Chemicals Industry Overview

The Thailand Construction Chemicals Market is moderately consolidated, with the top five companies occupying 50.28%. The major players in this market are Fosroc, Inc., MBCC Group, Saint-Gobain, Sika AG and TOA Paint (Thailand) Public Company Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Act (Thailand) Co., Ltd.

- 6.4.2 Ardex Group

- 6.4.3 Cemkrete Inter Co., Ltd

- 6.4.4 CORMIX INTERNATIONAL LIMITED

- 6.4.5 Fosroc, Inc.

- 6.4.6 MAPEI S.p.A.

- 6.4.7 MBCC Group

- 6.4.8 Saint-Gobain

- 6.4.9 Sika AG

- 6.4.10 TOA Paint (Thailand) Public Company Limited

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms