マレーシアの建設用化学品市場-シェア分析、業界動向と統計、成長予測(2026年~2031年)

Malaysia Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日

- 商品コード

- 1911820

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

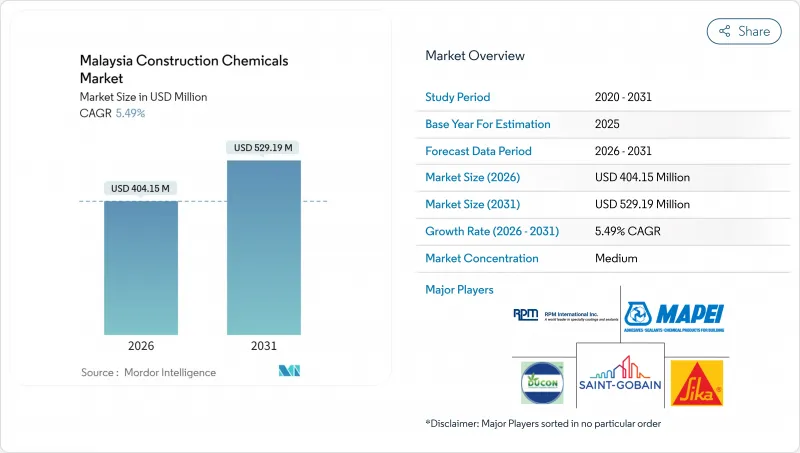

マレーシアの建設用化学品市場は、2025年の3億8,312万米ドルから2026年には4億415万米ドルへ成長し、2026~2031年にかけてCAGR5.49%で推移し、2031年までに5億2,919万米ドルに達すると予測されています。

2024年1月から11月にかけて発注された1,837億人民元規模のプロジェクトを含む持続的なインフラ投資の勢いが、開発業者が高性能な混和剤、防水シート、保護コーティングを指定するにつれて、着実な数量成長を支えています。2025年1月に調印されたジョホール・シンガポール特別経済区などのメガプロジェクトは、海洋環境や高湿度環境に適した耐久性化学製品の需要を加速させると予想されます。マレーシアの建設用化学品市場は、公共事業におけるBIM導入率90%という政府の義務化も追い風となっています。これは自動化された建設ワークフローとシームレスに統合される精密設計製品を有利にします。同時に、グリーンビルディング認証の勢いは、低VOC(揮発性有機化合物)とリサイクル可能な配合の採用を促進し、メーカーが持続可能性を重視した機会を捉えながらプレミアム価格を設定することを可能にしています。

マレーシアの建設用化学品市場の動向と洞察

サステイナブル公共・民間インフラ投資の加速

マレーシアの堅調なインフラ整備計画(2024年契約額:1,837億人民元)は、橋梁・トンネル・都市鉄道システム向け特殊防水シート、ポリマー改質グラウト、防食コーティングの成長を支えます。ジョホール・シンガポール特別経済区だけでも、5年以内に50の越境プロジェクトを目標としており、汽水環境にも耐える海洋用シーラントや炭酸塩防止混和剤の需要を拡大しています。TeslaやIntelなどの製造大手を含む官民連携により、性能基準がさらに高まり、静電気散逸性床用樹脂や耐薬品性壁用塗料の仕様開発が促進されています。改良された道路、港湾、デジタルチャネルは二次的な商業プロジェクトを呼び込み、マレーシアの建設用化学品市場全体で製品需要の好循環を強化しています。

住宅化学品消費を牽引する低所得者向け住宅施策

国家住宅施策による補助付き住宅の加速的な展開は、レディーミクストコンクリートやプレハブ壁パネルの使用を標準化し、混和剤の使用量を拡大すると同時に品質許容差を厳格化しています。低所得者向け住宅開発業者は自主的にグリーンビルディング基準を採用し、グリーンビルディング指数が定める炭素削減目標に沿った水性アクリル系シーラントや低VOCタイル接着剤の需要を喚起しています。イポーやクチンなどの地方都市への施策拡大に伴い流通網が拡大し、サプライヤーは小容量包装製品や移動式技術サービスチームの導入を促進しています。コスト重視のプロジェクトでは、高耐久性でありながら価格競合化学製品が採用され、現地メーカーはバッチ品質の安定化を図るため自動化生産ラインの規模拡大を推進しています。

原料価格の変動が市場拡大を制約

輸入ポリマー、特殊溶剤、高性能添加剤は、高級配合における原料コストの最大60%を占めており、メーカーは為替変動や原油価格急騰の影響を受けやすくなっています。ペトロナス社は2026年までの先物供給契約を締結していますが、中小規模の企業はスポット取引で購入しているため、原料コストが上昇するとEBITDAマージンが圧迫されます。2025年半ばから建設中のペンゲラン拠点35億米ドル規模の石油化学コンプレックスは、現地供給の統合を強化しますが、2028年以前に設計生産能力に達する見込みはありません。それまでは、資本不足の企業が統合型多国籍企業にシェアを譲ることで、変動性が産業再編を加速させる可能性があります。

セグメント分析

防水ソリューションは、クアラルンプールとジョホールバルにおける高層開発プロジェクトの屋上・ポディウムデッキへの義務付け仕様を背景に、2025年のマレーシアの建設用化学品市場シェアの48.42%を占めました。量販面ではアスファルト改質防水シートが首位を維持する一方、ポリマーセメント系ハイブリッド製品は地下工事における速硬化特性から支持を集めています。防水セグメントにおけるマレーシアの建設用化学品市場規模は、湿潤環境下での長寿命が求められる交通指向型開発、港湾、データセンター地下施設と歩調を合わせて拡大が見込まれます。

表面処理化学品は、プレキャスト外壁パネル向けに最適化された高度な硬化剤や離型エマルジョンにより、2031年までにCAGR6.78%という最も高い伸びを示す見込みです。落書き防止シーラーや疎水性シランゲルは、維持管理コスト削減を目指す自治体インフラ事業からの需要増加が見込まれます。イノベーションは、VOCレベルを増加させることなく耐摩耗性を高めるナノエンジニアリング粒子へと移行しており、グリーンビルディング認証基準にも適合しています。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インフラプロジェクトへのサステイナブル官民投資

- 低価格住宅推進による住宅着工件数の拡大

- グリーンビルディング認証が低VOC・高耐久性化学品の需要を促進

- レディーミクストコンクリートの急速な普及とプレハブ用混和剤の浸透率向上

- 特別経済区(SEZ)の税制優遇による特殊化学品生産の現地化

- 市場抑制要因

- 原料価格の変動が生産者の利益率を圧迫

- 環境・健康・安全(EHS)規制対応コストの上昇(揮発性有機化合物(VOC)、有害溶剤の禁止)

- 高度化学技術に対応できる熟練施工者の不足

- バリューチェーン分析

- 規制情勢

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 接着剤

- ホットメルト

- 反応性

- 溶剤系

- 水性

- アンカーとグラウト

- セメント系固定剤

- 樹脂固定

- コンクリート混和剤

- 加速剤

- 空気混入剤

- 高性能減水剤

- 遅延剤

- 収縮抑制剤

- 粘度調整剤

- 可塑剤

- その他

- コンクリート保護コーティング

- アクリル

- アルキド樹脂

- エポキシ樹脂

- ポリウレタン

- その他

- 床用樹脂

- アクリル

- エポキシ樹脂

- ポリアスパラギン酸

- ポリウレタン

- その他

- 補修・再生用化学製品

- 繊維巻き付けシステム

- 注入グラウティング

- マイクロコンクリートモルタル

- 改質モルタル

- 鉄筋保護材

- シーラント

- アクリル

- エポキシ樹脂

- ポリウレタン

- シリコン

- その他

- 表面処理用化学品

- 養生剤

- 離型剤

- その他

- 防水ソリューション

- 化学品

- 防水シート

- 接着剤

- 用途別

- 商用

- 産業・公共施設

- インフラ

- 住宅

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- ARDEX-QUICSEAL SINGAPORE

- Arkema(Bostik)

- Cementaid International

- Dribond Construction Chemicals

- Ducon Construction Chemicals

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- MC-Bauchemie

- PENETRON MALAYSIA SDN BHD.

- RPM International

- Saint-Gobain

- Sika AG

- Terraco Holdings Ltd.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日