|

市場調査レポート

商品コード

1684080

中東・アフリカの建設用化学品:市場シェア分析、産業動向、成長予測(2025年~2030年)Middle East and Africa Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの建設用化学品:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 388 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

中東・アフリカの建設用化学品市場規模は2024年に60億6,000万米ドルと推定され、2030年には82億9,000万米ドルに達すると予測され、予測期間中(2024年~2030年)のCAGRは5.38%で成長する見込みです。

商業エンドユーザー部門が成長率で市場をリード

- 2022年には、サウジアラビアとアラブ首長国連邦のインフラ部門が建設用化学品の需要急増に最も立ち会い、2019年から5%の金額増加を占めました。住宅部門は、2023年に需要が6%増加すると予測され、市場をリードすると予測されました。このように、住宅部門はこの地域の他のすべての部門と比較して最も成長を記録しました。

- サウジアラビアとアラブ首長国連邦を除く地域全体では、工業・施設部門が建設用化学品の主要消費者です。特に、床材用樹脂、コンクリート混和剤、表面処理用化学薬品がこの分野を支配しており、2022年の同部門の需要の16%を占めています。

- 住宅エンドユーザー部門は、同地域で2番目に高い建設用化学品製品の消費者です。さらに、サウジアラビアでは最も多く、2022年の全エンドユーザー部門の総消費量の42%を占める。2022年のコンクリート混和剤、表面処理薬品、接着剤は、地域全体とサウジアラビアにおけるこのエンドユーザー部門の需要の大半を占めています。

- サウジアラビアとアラブ首長国連邦は同地域の市場に最も大きな影響力を持っており、建設用化学品の需要において最も急成長しているエンドユーザー部門は商業用であるため、地域レベルでは商業用エンドユーザー部門の需要が最も急成長する可能性が高いです。この需要は、推定・予測期間中(2023年~2030年)にCAGR 5.83%を記録すると見られています。

サウジアラビアの住宅・商業セクターが同地域の市場成長に最も影響を与える

- 同地域の建設用化学品市場は、原油価格の上昇と堅調な経済成長に後押しされ、2022年に顕著な盛り上がりを見せた。この高騰は、2021年と比較して1億5,000万米ドルの市場価値の上昇につながりました。2023年には市場はさらに2億7,700万米ドル拡大し、住宅と商業セクターがこの成長の先頭に立ちました。

- サウジアラビアがこの地域の建設セクターで優位を占めているのは、その安定した政治的・法的枠組みが、ビジネス環境を求める多くの建設会社を引き付けているためと考えられます。サウジアラビアの豊富な熟練労働力は、主要産油国としての地位と相まって、すでに堅調な経済をさらに強化し、建設活動に拍車をかけています。その結果、サウジアラビアは同地域における建設用化学物質の需要を牽引する主要国として浮上しました。

- アラブ首長国連邦(UAE)は、建設部門のリーダーとしてサウジアラビアに僅差で続きます。アラブ首長国連邦(UAE)の魅力は、外国直接投資(FDI)の安定的な流入によって強化されており、2021年には域内の対内直接投資で首位の座を確保しました。

- 中東・アフリカでは、サウジアラビアが建設用化学品市場に大きな影響力を持っています。主要なエンドユーザーである住宅・商業セクターからの需要急増が予想されることから、サウジアラビアは予測期間(2023~2030年)のCAGRが6.18%と予測され、同地域で最も速い市場成長が見込まれます。

中東・アフリカの建設用化学品市場動向

サウジアラビアによる近代的なオフィスビル建設プロジェクトへの高額の投資が中東の商業建築の新規床面積を押し上げる見込み

- 2022年、中東・アフリカの商業施設の新設床面積は3.56%減少したが、これは主に鉄鋼価格の高騰とパンデミック後の輸送コストの5倍増によるものです。アラブ首長国連邦は、新規床面積の42.20%減という大幅な落ち込みで、その矛先がアラブ首長国連邦に向けられました。中東・アフリカの商業施設の新設床面積は、2023年には2022年比で2.83%増加すると予想されました。

- COVID-19の流行が2020年の景気減速につながり、その結果、多くの建設プロジェクトが中止または延期されました。その結果、2020年の新規床面積は2019年に比べ5.32%減少しました。2021年に規制が解除され建設活動が再開されると、新設床面積は2020年比で2.68%増加し、サウジアラビアが2.40%と最も高い伸びを示しました。

- 中東・アフリカの商業施設の新設床面積は予測期間中にCAGR 3.95%を記録すると予想され、中でもサウジアラビアは最も速いCAGR 4.34%を記録すると予想されます。これは、入居者が古いオフィスビルから近代的で整備されたオフィススペースや物流パークに移行する動向を受けたものです。さらに、ドバイのTECOM'S Innovation Hub Phase 2のように、35万5,000平方フィートに及ぶ複数のオフィスビル・プロジェクトが、UAEにおけるグレードAのオフィススペース需要の高まりに対応するために開発されています。さらに、サウジアラビアはJabal Omar、Amaala、Al Widyaaなどのプロジェクトに100億米ドル以上を投資し、地域の商業建設を強化する予定です。

中東・アフリカでは高予算住宅プロジェクトへの投資が増加し、住宅建設の新規床面積を押し上げると思われます。

- 2022年、中東・アフリカの住宅建設セクターは、都市化の進展と手頃な価格の住宅に対する人口需要の急増に牽引され、新設床面積が2.25%増加しました。この成長はさらに加速し、2023年にはサウジアラビアが主導して3.89%の増加が見込まれます。ビジョン2030の一環として、サウジアラビアの自治体・農村問題・住宅省は、2025年までに4万戸の手頃な価格の住宅をサウジアラビア国民に提供し、2030年までに住宅所有率を70%に引き上げるというイニシアチブを展開しました。

- COVID-19の流行は、この地域の住宅建設に顕著な影響を与えました。2020年には、施錠措置、労働力不足、サプライチェーンの混乱、個人消費の減少の結果、新規床面積は2019年比で7.46%減少しました。しかし、閉鎖措置が緩和され、建設活動が再開されたため、2021年には回復し、新設床面積は前年比2.43%増となりました。

- 中東・アフリカの住宅建設セクターは着実な成長を遂げており、予測期間中のCAGRは3.05%を記録すると予想されます。アラブ首長国連邦のCAGRは4.91%と最も速いと予想されます。推定価格56億米ドルのサウジアラビアのメガシティNEOMや、8,000人以上の住民に住宅を提供するために設計されたUAEのAl Quoz Creative Zoneなどの注目すべきプロジェクトが、この地域の住宅建設に拍車をかけると予想されます。2030年までに、新設床面積は46億4,000万平方フィートに達すると予想され、2022年の36億平方フィートから大幅に増加します。

中東・アフリカの建設用化学品産業の概要

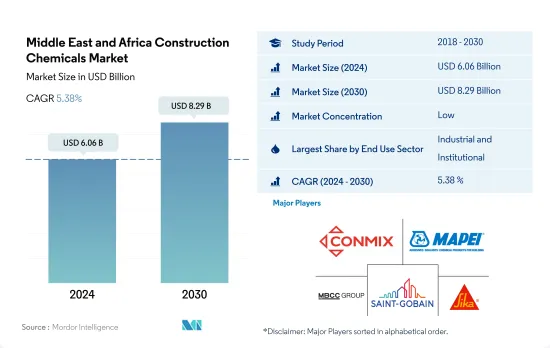

中東・アフリカの建設用化学品市場は細分化されており、上位5社で25.40%を占めています。この市場の主要企業は以下の通り。 Conmix, MAPEI S.p.A., MBCC Group, Saint-Gobain and Sika AG.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途分野の動向

- 商業

- 産業・施設

- インフラ

- 住宅

- 主要インフラプロジェクト(現在および発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途セクター

- 商業

- 産業・施設

- インフラ

- 住宅

- 製品

- 接着剤

- サブプロダクト別

- ホットメルト

- 反応性

- 溶剤系

- 水系

- アンカーとグラウト

- サブプロダクト別

- セメント系固定材

- 樹脂固定

- その他のタイプ

- コンクリート混和剤

- サブプロダクト別

- 促進剤

- 空気混入混和剤

- 高範囲減水剤(超可塑剤)

- 遅延剤

- 収縮低減混和剤

- 粘度調整剤

- 減水剤(可塑剤)

- その他のタイプ

- コンクリート保護塗料

- サブプロダクト別

- アクリル系

- アルキド

- エポキシ

- ポリウレタン

- その他の樹脂

- フローリング用樹脂

- サブプロダクト別

- アクリル

- エポキシ

- ポリアスパラギン

- ポリウレタン

- その他の樹脂タイプ

- 補修・再生ケミカル

- サブプロダクト別

- ファイバーラッピングシステム

- 注入グラウト材

- マイクロコンクリートモルタル

- 改質モルタル

- 鉄筋保護材

- シーリング材

- サブプロダクト別

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

- 表面処理薬品

- サブプロダクト別

- 硬化コンパウンド

- 離型剤

- その他の製品タイプ

- 防水ソリューション

- サブプロダクト別

- 化学製品

- メンブレン

- 接着剤

- 国名

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ahlia Chemicals Company

- Arkema

- CIKO Middle East

- CMB

- CMCI(Construction Material Chemical Industries)

- Conmix

- EAMIC

- Fosroc, Inc.

- Hemts Construction Chemicals

- MAPEI S.p.A.

- MBCC Group

- NCC X-CALIBUR

- Saint-Gobain

- Sika AG

- SOCHEM

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50002033

The Middle East and Africa Construction Chemicals Market size is estimated at 6.06 billion USD in 2024, and is expected to reach 8.29 billion USD by 2030, growing at a CAGR of 5.38% during the forecast period (2024-2030).

Commercial end-user sector to lead the market in terms of growth

- In 2022, the infrastructure sectors of Saudi Arabia and the United Arab Emirates witnessed the highest surge in demand for construction chemicals, accounting for a 5% increase in value from 2019. The residential sector was projected to lead the market, with an estimated 6% increase in demand in 2023. Thus, the residential sector recorded the most growth compared to all other sectors in the region.

- Across the region, except Saudi Arabia and the United Arab Emirates, the industrial and institutional sector is the primary consumer of construction chemicals. Notably, flooring resins, concrete admixtures, and surface treatment chemicals dominate this segment, collectively accounting for 16% of the sector's demand in 2022.

- The residential end-user sector is the region's second-highest consumer of construction chemicals. Additionally, it is the highest in Saudi Arabia, with a share of 42% of the total consumption by all the end-user sectors in 2022. Concrete admixtures, surface treatment chemicals, and adhesives in 2022 made up most of the demand of this end-user sector in the region overall and in Saudi Arabia.

- Since Saudi Arabia and the United Arab Emirates have the most influence over the market in the region, and as their fastest-growing end-user sector in terms of demand for construction chemicals is the commercial, the demand consequently will likely grow the fastest in the commercial end-user sector at a regional level. The demand is estimated to record a CAGR of 5.83% during the forecast period (2023-2030).

Saudi Arabia's residential and commercial sectors to have the most impact on the market's growth in the region

- The construction chemicals market in the region witnessed a notable upswing in 2022, buoyed by rising oil prices and robust economic growth. This surge translated into a USD 150 million uptick in market value compared to 2021. The market further expanded by USD 277 million in 2023, with the residential and commercial sectors spearheading this growth.

- Saudi Arabia's dominance in the regional construction sector can be attributed to its stable political and legal framework, which attracts numerous construction firms seeking a conducive business environment. The country's abundant skilled labor pool, coupled with its status as a major oil producer, bolsters its already robust economy, further fueling construction activities. Consequently, Saudi Arabia emerges as the primary driver of demand for construction chemicals in the region.

- The United Arab Emirates (UAE) follows closely behind Saudi Arabia in terms of construction sector leadership. The UAE's attractiveness is bolstered by its consistent inflow of foreign direct investment (FDI), with 2021 seeing it secure the top spot in the region for inbound FDI.

- Within the Middle East & Africa, Saudi Arabia wields significant influence over the construction chemicals market. Given the anticipated surge in demand from its key end-user sectors, residential and commercial, Saudi Arabia is poised to witness the region's fastest market growth, with a projected CAGR of 6.18% during the forecast period (2023-2030).

Middle East and Africa Construction Chemicals Market Trends

High investments in modern office building projects by Saudi Arabia are expected to propel the new floor area for commercial construction in the Middle East

- In 2022, the Middle East & Africa witnessed a 3.56% decline in the new floor area for commercial construction, primarily due to surging steel prices and a fivefold increase in shipping costs post-pandemic. The United Arab Emirates bore the brunt, with a significant 42.20% drop in new floor area. The new floor area for commercial construction in the Middle East & Africa was expected to grow by 2.83% in 2023 compared to 2022.

- The COVID-19 pandemic led to an economic slowdown in 2020, resulting in the cancellation or postponement of numerous construction projects. Consequently, the new floor area saw a 5.32% dip in 2020 compared to 2019. As the restrictions were lifted in 2021 and construction activities resumed, the new floor area grew by 2.68% compared to 2020, with Saudi Arabia having the highest growth of 2.40%.

- The new floor area for commercial construction in the Middle East & Africa is expected to record a CAGR of 3.95% during the forecast period, with Saudi Arabia expected to record the fastest CAGR of 4.34%, following a trend of occupiers migrating from old office buildings to modern, well-maintained office spaces, and logistic parks. Furthermore, several office building projects like TECOM'S Innovation Hub Phase 2 in Dubai, spread across 355,000 square feet, are being developed to meet the growing demand for Grade A office spaces in the UAE. Additionally, Saudi Arabia will invest more than USD 10 billion in projects like Jabal Omar, Amaala, and Al Widyaa, among others, to bolster regional commercial construction.

Increasing investments in high-budget housing projects in the Middle East & Africa will likely drive the new floor area for residential construction

- In 2022, the residential construction sector in the Middle East & Africa witnessed a 2.25% growth in new floor area, driven by increased urbanization and a surging population's demand for affordable housing. This growth was projected to accelerate, with an expected increase of 3.89% in 2023, led by Saudi Arabia. As part of its Vision 2030, the Ministry of Municipal and Rural Affairs and Housing in Saudi Arabia rolled out initiatives to deliver 40,000 affordable housing units to Saudi nationals by 2025 and raise the homeownership rate to 70% by 2030.

- The COVID-19 pandemic had a notable impact on residential construction in the region. In 2020, as a result of lockdowns, labor shortages, disrupted supply chains, and reduced consumer spending, the new floor area saw a decline of 7.46% compared to 2019. However, as lockdown measures eased and construction activities resumed, the region rebounded in 2021, witnessing a 2.43% growth in new floor area compared to the previous year.

- The residential construction sector in the Middle East & Africa is poised for steady growth, and it is expected to record a CAGR of 3.05% during the forecast period. The United Arab Emirates is expected to register the fastest CAGR of 4.91%. Noteworthy projects, such as Saudi Arabia's NEOM, a mega-city with an estimated value of USD 5.60 billion, and the Al Quoz Creative Zone in the UAE, designed to provide housing for more than 8,000 residents, are expected to fuel the region's residential construction. By 2030, the new floor area is anticipated to reach 4.64 billion square feet, a significant increase from 3.6 billion square feet in 2022.

Middle East and Africa Construction Chemicals Industry Overview

The Middle East and Africa Construction Chemicals Market is fragmented, with the top five companies occupying 25.40%. The major players in this market are Conmix, MAPEI S.p.A., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ahlia Chemicals Company

- 6.4.2 Arkema

- 6.4.3 CIKO Middle East

- 6.4.4 CMB

- 6.4.5 CMCI (Construction Material Chemical Industries)

- 6.4.6 Conmix

- 6.4.7 EAMIC

- 6.4.8 Fosroc, Inc.

- 6.4.9 Hemts Construction Chemicals

- 6.4.10 MAPEI S.p.A.

- 6.4.11 MBCC Group

- 6.4.12 NCC X-CALIBUR

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 SOCHEM

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms